Global Usage Based Insurance Market, By Device Offering (Bring Your Own Device (BYOD), Company Provided), Electric Vehicle Type (Battery Electric Vehicle (BEV), Fuel-Cell Electric Vehicle (FCEV), Plug-In Hybrid Vehicle (PHEV)), Package Type (Pay-as-you-Drive (PAYD), Pay-how-you-Drive (PHYD), Manage-how-you-Drive (MHYD)), Technology (OBD-II, Smartphone, Embedded Telematics Box), Vehicle Age (New Vehicle, Old Vehicle), Vehicle Type (Light-Duty Vehicle (LDV), Heavy-Duty Vehicle (HDV)), and Region — Industry Analysis and Forecast to 2030

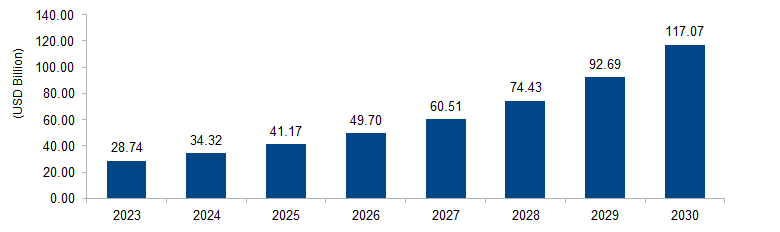

The global usage based insurance market is expected to grow from USD 28.74 billion in 2023 to USD 117.07 billion by 2030 at a CAGR of 22.2%. The usage-based insurance (UBI) market is driven by the growing demand for personalized and data-driven insurance solutions. UBI leverages telematics and real-time data from connected devices to assess individual driving behavior. Consumers are increasingly attracted to UBI for its potential cost savings, tailored premiums based on actual driving habits, and the incentive for safer driving practices. This market responds to the evolving preferences of tech-savvy and risk-conscious policyholders seeking more transparent and flexible insurance options.

Figure 1: Global Usage Based Insurance Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Usage-based insurance (UBI) is a personalized insurance model that utilizes telematics technology to assess an individual’s driving behavior in real-time. Instead of relying solely on traditional risk factors, UBI captures data through connected devices installed in vehicles, monitoring factors such as driving speed, distance, braking patterns, and time of day. Insurers use this data to calculate premiums, offering policyholders the opportunity for more customized rates based on their actual driving habits. UBI incentivizes safer driving practices, promotes transparency, and allows policyholders to potentially lower their insurance costs by demonstrating responsible behavior on the road through continuous monitoring and data analysis.

Usage Based Insurance Market Drivers

Advancements in Telematics Technology

A significant driver for the usage-based insurance (UBI) market is the continual advancements in telematics technology. The increasing sophistication of connected devices and in-vehicle sensors allows insurers to gather detailed and accurate data on driving behavior. According to the National Association of Insurance Commissioners (NAIC), the adoption of telematics in the auto insurance sector has witnessed substantial growth. The evolving capabilities of telematics devices enable the tracking of various parameters such as speed, acceleration, braking, and location in real-time. This wealth of data empowers insurers to create more nuanced risk profiles, fostering a fairer and personalized pricing model for policyholders. As telematics technology becomes more affordable and accessible, it drives the expansion of UBI programs. The Insurance Information Institute (III) notes that the increased adoption of telematics is enhancing insurers’ ability to assess risk accurately and incentivizing safer driving practices, thereby propelling the growth of the UBI market globally.

Changing Consumer Behavior and Preferences

Changing consumer behavior and preferences act as another significant driver for the UBI Market. The desire for personalized and flexible insurance solutions has grown among policyholders. According to the Pew Research Center, the increasing use of digital technologies and the desire for tailored services have become prominent aspects of modern consumer behavior. UBI aligns with this shift by offering policyholders customized premiums based on their actual driving habits. The willingness of consumers to share data in exchange for potential cost savings and personalized insurance plans is driving the adoption of UBI. The National Association of Insurance Commissioners (NAIC) highlights the growing interest in UBI among younger demographics who are more accustomed to digital technologies. As consumers seek transparency and fair pricing in insurance, UBI presents an attractive option, allowing individuals to have a direct impact on their insurance costs through responsible driving, reflecting the changing landscape of consumer expectations and preferences in the insurance market.

Usage Based Insurance Market Restraints

Privacy Concerns and Data Security Challenges

One significant restraint for the usage-based insurance (UBI) market revolves around privacy concerns and the associated challenges of data security. As insurers collect and analyze real-time driving data through telematics devices, policyholders express apprehensions about the potential invasion of privacy. According to surveys conducted by the National Association of Insurance Commissioners (NAIC), a considerable percentage of consumers hesitate to adopt UBI due to worries about how their personal driving information is handled and shared. Striking a balance between leveraging data for risk assessment and addressing privacy concerns becomes crucial for market growth. Furthermore, the Insurance Information Institute (III) underscores the importance of safeguarding the sensitive information collected by telematics devices against cybersecurity threats. Instances of data breaches or misuse of personal information can erode trust and hinder the broader acceptance of UBI. Overcoming these challenges requires stringent data protection measures, transparent communication about data usage policies, and compliance with privacy regulations, such as the General Data Protection Regulation (GDPR) in Europe, to assure policyholders of the secure and responsible handling of their information.

Limited Adoption Among Older Demographics and Non-Tech Savvy Consumers

Another restraint in the UBI market is the limited adoption among older demographics and non-tech-savvy consumers. According to studies by the Pew Research Center, there exists a digital divide among different age groups, with older individuals being less likely to embrace digital technologies. Similarly, the National Association of Insurance Commissioners (NAIC) notes that the preference for traditional insurance models remains prominent among certain demographics that may not be as comfortable with or reliant on digital devices. This limited adoption poses a challenge for insurers looking to expand UBI programs across a diverse customer base. Additionally, the Insurance Information Institute (III) emphasizes the need for user-friendly interfaces and educational initiatives to bridge the gap and enhance awareness among older and less tech-savvy consumers. Overcoming the hurdle of technology adoption requires targeted strategies, clear communication about the benefits of UBI, and the development of solutions that cater to a broader demographic spectrum, ensuring that the advantages of personalized insurance are accessible to all consumer segments.

Usage Based Insurance Market Opportunities

Innovative Partnership Models

An opportunity for the usage-based insurance (UBI) market lies in the exploration of innovative partnership models. Insurers can collaborate with various stakeholders, including automakers, telecommunications companies, and technology providers, to enhance the value proposition of UBI. According to the National Association of Insurance Commissioners (NAIC), partnerships with automakers are gaining traction, allowing insurers to integrate telematics solutions directly into vehicles. This not only streamlines the data collection process but also creates a seamless and user-friendly experience for policyholders. The Insurance Information Institute (III) highlights the potential for partnerships with smart city initiatives, leveraging data from connected infrastructure to enhance risk assessment and pricing accuracy. Such collaborations can lead to the development of holistic mobility solutions, combining insurance offerings with intelligent transportation systems. Exploring diverse partnership models opens avenues for insurers to expand their UBI portfolios, enhance customer engagement, and stay at the forefront of evolving mobility ecosystems.

Expansion of UBI Beyond Auto Insurance

An emerging opportunity for the UBI market is the expansion of usage-based insurance beyond traditional auto insurance products. The National Association of Insurance Commissioners (NAIC) notes that UBI principles can be applied to other insurance segments, such as home insurance and health insurance. In the context of home insurance, IoT devices and smart home technologies can provide valuable data for risk assessment, allowing insurers to tailor premiums based on real-time information about home security, maintenance, and occupancy. Similarly, in health insurance, wearable devices and health monitoring tools can contribute to personalized insurance plans based on individuals’ lifestyle and health choices. The Insurance Information Institute (III) emphasizes the potential for insurers to leverage UBI concepts across a spectrum of insurance products, offering consumers more customized coverage options. This expansion aligns with the broader trend of insurtech innovation and presents opportunities for insurers to diversify their UBI offerings, catering to evolving consumer needs and preferences across different insurance segments.

Usage Based Insurance Market Challenges

Regulatory Hurdles and Standardization Challenges

A significant challenge for the usage-based insurance (UBI) market is navigating regulatory hurdles and standardization challenges. The National Association of Insurance Commissioners (NAIC) highlights the complexities arising from varying regulations across different regions and countries. Inconsistent regulatory frameworks pose obstacles to the seamless implementation of UBI programs, making it challenging for insurers to offer standardized solutions globally. The lack of uniformity in data privacy and usage regulations adds a layer of complexity, requiring insurers to navigate a patchwork of legal requirements. Additionally, the Insurance Information Institute (III) underscores the need for standardization in data collection and analysis methodologies. The absence of industry-wide standards makes it challenging to compare and assess UBI offerings consistently. The development of standardized practices and collaboration with regulatory bodies becomes essential to create a conducive environment for UBI growth. Overcoming these challenges requires proactive engagement with regulators, industry associations, and policymakers to establish clear guidelines and standards that foster innovation while addressing privacy and regulatory concerns.

Customer Trust and Perception

Building and maintaining customer trust represent a significant challenge for the usage-based insurance (UBI) market. The National Association of Insurance Commissioners (NAIC) notes that concerns about how driving data is used and potential privacy breaches can create hesitancy among consumers to adopt UBI. Issues related to data accuracy, security, and the fear of increased premiums based on collected data can contribute to a lack of trust. The Insurance Information Institute (III) emphasizes the importance of transparent communication about the benefits and potential risks of UBI to alleviate consumer concerns. Building trust requires insurers to be clear about data usage policies, ensure robust cybersecurity measures, and provide tangible benefits, such as cost savings and personalized coverage. Overcoming these challenges involves ongoing education, effective communication strategies, and the establishment of industry best practices to create a positive perception of UBI among consumers. As UBI continues to evolve, addressing these trust-related challenges is crucial for widespread adoption and the long-term success of usage-based insurance programs.

Regional Trends

North America: In North America, the UBI market trends were characterized by a growing acceptance of telematics-based insurance solutions. The National Association of Insurance Commissioners (NAIC) noted a rise in the adoption of UBI programs by insurers, particularly in the auto insurance sector. The trend included increased collaboration between insurers and automakers to integrate telematics devices directly into vehicles. Additionally, there was a focus on enhancing user experiences and addressing privacy concerns through transparent communication. Consumer interest in personalized insurance premiums based on driving behavior contributed to the overall growth of UBI programs in North America.

Europe: Europe witnessed a surge in UBI adoption, driven by regulatory support and advancements in telematics technology. The European Insurance and Occupational Pensions Authority (EIOPA) highlighted the role of regulatory initiatives, such as the General Data Protection Regulation (GDPR), in shaping UBI practices. Insurers in Europe explored innovative partnerships with automakers and technology providers to expand UBI offerings. The trend included a shift toward more sophisticated risk assessment models, leveraging a broader range of telematics data. European insurers also explored opportunities to extend UBI principles beyond auto insurance into other segments like home and health insurance.

Asia Pacific: The UBI Market in the Asia Pacific region exhibited trends associated with the region’s rapid technological advancements and the increasing adoption of connected devices. Insurers in countries like China and Japan explored telematics solutions to provide more personalized insurance offerings. The Asia Insurance Review noted a growing interest in leveraging UBI for commercial fleets and expanding usage-based insurance beyond personal auto policies. Insurers in the region aimed to enhance customer engagement through user-friendly interfaces and incentives for safe driving behaviors.

Middle East and Africa: In the Middle East and Africa, UBI trends were influenced by efforts to modernize insurance practices and improve road safety. Insurers in the region explored partnerships with technology providers to deploy telematics solutions. The Middle East Insurance Review highlighted pilot programs aimed at incentivizing safer driving behaviors and reducing accident rates through UBI initiatives. The trends included considerations for adapting UBI models to the unique characteristics of the regional insurance landscape.

Latin America: Latin America experienced a gradual adoption of UBI, with insurers exploring telematics solutions to address specific challenges in the insurance market. The Latin American Insurance Review noted a focus on using UBI to mitigate fraud and improve risk assessment accuracy. Insurers sought to educate consumers about the benefits of UBI and address privacy concerns. The trends included efforts to align UBI offerings with local regulatory frameworks and adapt telematics solutions to the diverse driving conditions in the region.

Key Players

Key players operating in the global usage based insurance market are Progressive Casualty Insurance Company, Unipolsai Assicurazioni S.P.A, State Farm Mutual Automobile Insurance Company, AXA, Allstate Insurance Company, Liberty Mutual Insurance Company, Assicurazioni Generali S.P.A, Allianz, Webfleet Solutions, Verizon, Zubie, Inc., Nationwide Mutual Insurance Company, Cambridge Mobile Telematics, Modus Group, LLC, Metromile, Inc., Sierra Wireless, Octo Group S.P.A, and Amica.

PRICE

ASK FOR FREE SAMPLE REPORT