Global RF Signal Chain Component Market, By Product (RF Amplifiers, Voltage-Controlled Oscillators (VCOS), Power Dividers, Filters, Mixers, Switches, Attenuators, Duplexers, Diplexers, Couplers, Phase Shifters), Frequency Band (VHF/UHF Band (30-100 MHz), L Band (1-2 GHz), S Band (2-4 GHz), C Band (4-8 GHz), X Band (8-12 GHz), Ku Band (12-18 GHz), K Band (18-27 GHz), Ka Band (26.5-40 GHz), V Band (40-75 GHz), W Band (75-110 GHz)), Material Type (Gallium Arsenide (GaAs), Gallium Nitride (GaN), Silicon, Silicon-Germanium), Application (Telecommunication Infrastructure, Consumer Electronics, Satcom, Automotive, Aerospace & Defense, Medical), and Region — Industry Analysis and Forecast to 2030

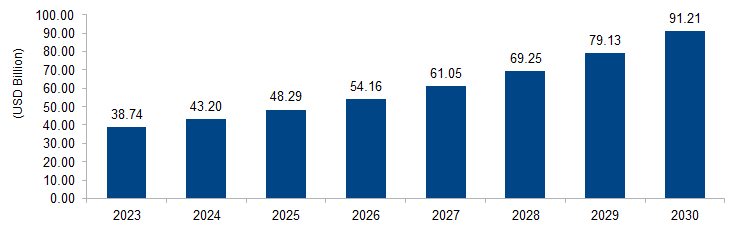

The global RF signal chain component market is expected to grow from USD 38.74 billion in 2023 to USD 91.21 billion by 2030 at a CAGR of 13.0%. The market is driven by the growing demand for high-performance wireless communication systems. As industries adopt advanced technologies like 5G, IoT, and satellite communications, there is an increasing need for efficient and reliable RF signal chain components to ensure seamless connectivity, driving the market’s growth.

Figure 1: Global RF Signal Chain Component Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

RF (Radio Frequency) signal chain components refer to a series of interconnected electronic elements crucial in processing and transmitting radio frequency signals within communication systems. Comprising components like amplifiers, filters, mixers, and modulators, the signal chain ensures the efficient conversion, amplification, and modulation of RF signals. It plays a pivotal role in diverse applications, including wireless communication, radar systems, and satellite communication. Optimizing the RF signal chain enhances signal quality, minimizes interference, and enables the seamless transmission of information across various wireless technologies, such as 5G networks, IoT devices, and other wireless communication systems.

RF Signal Chain Component Market Drivers

Proliferation of 5G Technology

A significant driver propelling the RF signal chain component market is the widespread deployment of 5G technology. The International Telecommunication Union (ITU) emphasizes the transformative impact of 5G on wireless communication, offering higher data speeds, low latency, and increased network capacity. As governments and telecom operators globally invest in 5G infrastructure, the demand for advanced RF signal chain components intensifies. The Federal Communications Commission (FCC) in the United States, for example, has allocated substantial spectrum for 5G, driving the need for components like high-frequency amplifiers and filters to support the expanded frequency bands. The accelerating adoption of 5G is reflected in the growing number of 5G subscriptions worldwide, which surpassed 1 billion in 2022, reinforcing the crucial role of RF signal chain components in enabling the capabilities of next-generation wireless networks.

Rise of Internet of Things (IoT)

Another key driver is the rapid expansion of the Internet of Things (IoT) ecosystem, where interconnected devices demand efficient RF signal chain components for seamless communication. The IoT market is witnessing substantial growth, with the number of connected devices projected to reach tens of billions globally. Government initiatives, such as the European Commission’s focus on IoT standardization and interoperability, underscore the strategic importance of IoT in various sectors. RF components like transceivers, filters, and low-power amplifiers are integral to IoT devices, facilitating reliable and energy-efficient wireless communication. As industries adopt IoT for applications like smart cities, healthcare, and industrial automation, the demand for specialized RF signal chain components is propelled. The surge in IoT deployments indicates a robust market outlook, positioning RF signal chain components as essential enablers for the seamless connectivity and communication infrastructure required by the expanding IoT landscape.

RF Signal Chain Component Market Restraints

Spectrum Allocation Challenges

A notable restraint in the RF signal chain component market is the challenge associated with spectrum allocation and the scarcity of available frequencies for wireless communication. Government regulatory bodies, such as the Federal Communications Commission (FCC) in the United States and similar entities worldwide, play a pivotal role in assigning and regulating the use of radio frequency spectrum. The increasing demand for wireless communication services, especially with the proliferation of 5G and IoT, has led to a spectrum crunch. For instance, the FCC’s efforts to auction additional spectrum for 5G applications highlight the complexities in balancing the growing demand with the finite availability of suitable frequency bands. The spectrum shortage can limit the expansion of RF signal chain components, particularly in applications that require higher frequency bands. As a result, industries may face challenges in optimizing their wireless communication systems, potentially impacting the development and adoption of advanced RF technologies.

Interference and Coexistence Issues

Another significant restraint is the issue of interference and coexistence in the crowded RF spectrum. As more devices and communication systems utilize the available frequency bands, the potential for interference between different wireless technologies increases. The International Telecommunication Union (ITU) recognizes the importance of addressing interference concerns, particularly in the context of IoT and smart city deployments. Coexistence challenges arise when multiple wireless devices operate in proximity, leading to degraded signal quality and performance. Governments and industry associations are working towards defining standards and regulations to mitigate interference, but the complexity of the RF environment remains a challenge. As the number of connected devices continues to rise, the potential for interference-related issues poses a restraint on the seamless operation of RF signal chain components. This challenge underscores the need for innovative solutions and collaborative efforts to manage the coexistence of diverse wireless technologies within the limited spectrum resources available.

RF Signal Chain Component Market Opportunities

Satellite Communication Advancements

An intriguing opportunity for the RF signal chain component market lies in the advancements and expansion of satellite communication technologies. Governments and private entities worldwide are investing in satellite constellations for applications such as broadband internet coverage and Earth observation. The International Telecommunication Union (ITU) emphasizes the significance of satellite communication in bridging the digital divide, especially in remote and underserved areas. RF signal chain components, including frequency converters and transceivers, play a crucial role in satellite communication systems. As the satellite industry experiences growth, the demand for high-performance RF components is expected to rise. For instance, the global satellite transponder market is projected to witness substantial growth, reflecting the opportunities presented by increased satellite deployments. This trend aligns with the broader push for global connectivity, making RF signal chain components key enablers in shaping the future of satellite communication technologies.

Emergence of Millimeter Wave Technology

An emerging opportunity in the RF signal chain component market is the increasing utilization of millimeter wave (mmWave) technology for high-frequency communication. As the demand for higher data rates and enhanced wireless capabilities escalates, mmWave frequencies (30 GHz to 300 GHz) are gaining prominence. Government bodies such as the Federal Communications Commission (FCC) have allocated spectrum in the mmWave range to support applications like 5G and wireless backhaul. RF signal chain components designed for mmWave frequencies, including amplifiers and mixers, are crucial for realizing the potential of these high-bandwidth applications. The mmWave technology market is anticipated to witness significant growth, reflecting the opportunities for RF signal chain components in this domain. Leveraging mmWave frequencies offers advantages such as increased data capacity and faster communication speeds, presenting a promising opportunity for manufacturers and innovators in the RF signal chain component market to cater to the evolving needs of high-frequency communication systems.

RF Signal Chain Component Market Challenges

Security Concerns in Wireless Communication

A substantial challenge facing the RF signal chain component market is the increasing complexity of addressing security concerns in wireless communication systems. As wireless technologies, particularly 5G and IoT, become pervasive, the vulnerability to cybersecurity threats escalates. Government agencies, including the U.S. Department of Homeland Security (DHS) and international organizations, highlight the critical importance of securing communication networks against potential cyber-attacks. RF signal chain components, being integral to communication systems, are exposed to risks such as eavesdropping, signal interception, and unauthorized access. The challenge is not only to ensure the robustness of individual components but also to establish secure end-to-end communication channels. The global cost of cybersecurity breaches is staggering, underscoring the urgency of addressing these challenges. The evolving threat landscape necessitates continuous innovation in security measures, encryption technologies, and authentication protocols within RF signal chain components to safeguard wireless communication systems. Balancing the need for seamless connectivity with robust security measures poses a complex challenge for manufacturers and stakeholders in the RF signal chain component market.

Environmental Impact and Sustainability

Another significant challenge in the RF signal chain component market pertains to the environmental impact and sustainability considerations associated with manufacturing and disposal of electronic components. Governments and environmental agencies worldwide, such as the Environmental Protection Agency (EPA) in the United States, are increasingly focusing on reducing electronic waste (e-waste) and promoting sustainable practices in the electronics industry. RF signal chain components, which often contain materials with environmental implications, contribute to the broader e-waste challenge. The production processes, use of rare-earth materials, and end-of-life disposal present environmental concerns. As the demand for wireless communication technologies rises, so does the volume of electronic components, amplifying the ecological footprint. Sustainable practices, including recycling and eco-friendly manufacturing, are gaining importance. Industry associations are working towards establishing guidelines for sustainable electronic design and production. Navigating this challenge requires a concerted effort from the RF signal chain component market to adopt green manufacturing practices, minimize waste, and explore environmentally friendly materials, aligning with global initiatives for a more sustainable and environmentally responsible electronics industry.

Regional Trends

North America: In North America, particularly in the United States, there is a trend towards increased research and development (R&D) investments in advanced communication technologies. Government initiatives, including spectrum auctions by the Federal Communications Commission (FCC) to support 5G deployment, indicate a thriving environment for RF Signal Chain Component innovation. The region is likely to witness a surge in demand for components supporting high-frequency communication, driven by the growing adoption of 5G and advancements in satellite communication.

Europe: Europe is experiencing a trend towards regulatory alignment and standardization to facilitate the deployment of advanced wireless communication technologies. Organizations such as the European Telecommunications Standards Institute (ETSI) play a key role in defining standards for RF technologies. With the European Commission’s focus on achieving digital connectivity targets, the RF signal chain component market in Europe is expected to see increased collaboration between industry stakeholders and regulatory bodies.

Asia Pacific: In the Asia Pacific region, particularly in countries like China, Japan, and South Korea, there is a trend towards dominance in the global semiconductor and electronics manufacturing landscape. The region is a key player in the production of RF Signal Chain Components, benefiting from the presence of major electronics manufacturers. With the increasing demand for 5G infrastructure and IoT devices, the Asia Pacific market is likely to witness significant growth in the RF Signal Chain Component sector.

Middle East and Africa: The Middle East and Africa are experiencing a trend towards the deployment of advanced communication technologies to support smart city initiatives and improve connectivity. Governments in the region are investing in 5G infrastructure, and the adoption of RF Signal Chain Components is expected to rise to meet the demands of these technological advancements.

Latin America: Latin America is witnessing a trend towards increasing connectivity and digital transformation. As countries in the region work towards expanding access to high-speed internet and enhancing communication networks, there is a growing demand for RF Signal Chain Components. Initiatives to bridge the digital divide and improve communication infrastructure are likely to drive the market in Latin America.

Key Players

Key players operating in the global RF signal chain component market are Analog Devices, Inc., Qorvo, Inc, Skyworks Solutions, Inc., Broadcom, MACOM, Murata Manufacturing Co., Ltd., National Instruments Corp., CPI INTERNATIONAL, NXP Semiconductors, STMicroelectronics, Infineon Technologies AG, Texas Instruments, Mitsubishi Electric, Cobham Limited, Microchip Technology Inc., Astra Microwave Products Limited, Panasonic Holdings Corporation, and Microwave Technology, Inc.

PRICE

ASK FOR FREE SAMPLE REPORT