Global Private Cloud Market, By Service Model (Infrastructure as a Service, Platform as a Service, Software as a Service), Organization Size (Large Enterprises, Small and Medium-sized Enterprises), Industry Vertical, and Region – Industry Analysis and Forecast to 2030

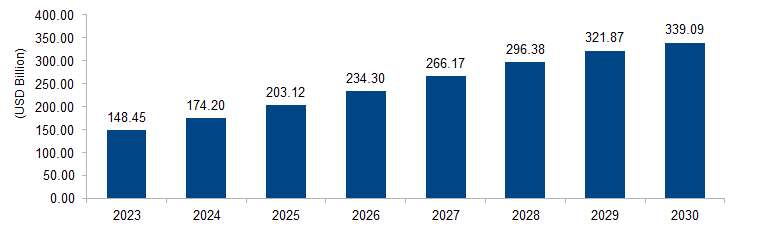

The global private cloud market is expected to grow from USD 148.45 billion in 2023 to USD 339.09 billion by 2030 at a CAGR of 12.5%. The private cloud market is driven by the increasing demand for secure and customizable cloud solutions. Organizations opt for private clouds to retain control over their data, comply with industry-specific regulations, and address privacy concerns. The flexibility to tailor infrastructure and services to specific needs fosters private cloud adoption, catering to enterprises’ diverse requirements for scalability and data governance.

Figure 1: Global Private Cloud Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

A private cloud refers to a cloud computing environment exclusively dedicated to a single organization. Unlike public clouds, private clouds are designed to meet the specific needs of an individual business, offering a secure and isolated infrastructure. Hosted either on-premises or by a third-party provider, private clouds provide greater control over data, security, and compliance, making them ideal for industries with stringent regulatory requirements. This model allows organizations to leverage the benefits of cloud computing, such as scalability and resource optimization, while maintaining a higher level of customization and privacy, making it well-suited for enterprises with unique operational and security considerations.

Private Cloud Market Drivers

Enhanced Data Security and Privacy Concerns

One significant driver of the private cloud market is the heightened focus on enhanced data security and privacy concerns. Government agencies, such as the European Union with its General Data Protection Regulation (GDPR), emphasize the need for robust data protection measures. Private clouds address these concerns by offering dedicated and isolated infrastructure, allowing organizations to have greater control over their data and maintain compliance with strict regulations. The increasing instances of high-profile data breaches underscore the importance of secure cloud solutions. For example, reports from the U.S. Federal Trade Commission (FTC) indicate a rising number of data breach incidents, prompting organizations to prioritize private cloud adoption to safeguard sensitive information. The commitment to data privacy, coupled with regulatory imperatives, serves as a driving force propelling the demand for private cloud solutions across various industries.

Customization and Tailored Infrastructure Solutions

Another key driver in the private cloud market is the demand for customization and tailored infrastructure solutions to meet specific organizational requirements. Different sectors have unique operational needs, and private clouds offer a level of flexibility that enables organizations to customize their cloud environment accordingly. This is particularly crucial for industries with specific regulatory constraints, such as healthcare or finance. Government reports, like those from the U.S. National Institute of Standards and Technology (NIST), acknowledge the importance of tailored cloud solutions in aligning with diverse business needs. As organizations increasingly recognize the value of a cloud infrastructure designed to fit their specific workflows and applications, the private cloud market experiences growth. The ability to adapt and scale resources based on individual requirements positions private clouds as a strategic choice for enterprises seeking a customized and efficient cloud computing environment.

Private Cloud Market Restraints

High Initial Implementation Costs and Resource Investments

A significant restraint in the private cloud market is the high initial implementation costs and resource investments required for setting up dedicated infrastructure. Government organizations, such as the U.S. Small Business Administration (SBA), recognize that the upfront expenses associated with deploying a private cloud, including hardware procurement, software licenses, and skilled personnel, can be substantial. Small and medium-sized enterprises (SMEs) particularly feel the financial strain, hindering their ability to adopt private cloud solutions. The SBA reports indicate that budget constraints often limit the adoption of private clouds, as the initial capital outlay can divert resources from other critical business needs. Overcoming this restraint involves initiatives to streamline implementation costs, promote cost-effective solutions, and provide support mechanisms to make private cloud adoption more accessible, especially for smaller enterprises.

Limited Scalability Compared to Public Cloud Alternatives

Another notable challenge facing the private cloud market is the limited scalability compared to public cloud alternatives. Government reports from bodies like the National Institute of Standards and Technology (NIST) acknowledge that private clouds may face constraints in quickly scaling resources to meet fluctuating demands. Unlike public clouds that offer virtually unlimited scalability, the finite nature of privately-owned infrastructure can become a limiting factor, particularly during periods of rapid growth or sudden resource spikes. This scalability limitation can impact the ability of organizations to adapt swiftly to changing business requirements. While private clouds offer customization and control, organizations need to carefully assess their scalability needs and balance them against the inherent limitations of a dedicated infrastructure model. Addressing this restraint may involve strategic planning, hybrid cloud approaches, or considering a mix of private and public cloud solutions to achieve optimal scalability without compromising control and security.

Private Cloud Market Opportunities

Edge Computing Integration for Low Latency Applications

A significant opportunity in the private cloud market is the integration of edge computing capabilities to support low-latency applications. As the Internet of Things (IoT) continues to grow, government agencies such as the National Institute of Standards and Technology (NIST) emphasize the need for edge computing solutions to process data closer to the source. Private clouds, with their dedicated infrastructure, offer an opportunity to establish edge computing nodes strategically. This facilitates the processing of time-sensitive data locally, reducing latency and enhancing the performance of applications such as real-time analytics, autonomous vehicles, and smart cities. The integration of edge computing into private cloud environments aligns with the evolving technological landscape, presenting a lucrative opportunity for organizations to provide efficient, low-latency solutions tailored to specific industry needs.

Disaster Recovery and Business Continuity Solutions

Another significant opportunity in the private cloud market is the provision of robust disaster recovery and business continuity solutions. Government reports, including those from the Federal Emergency Management Agency (FEMA), emphasize the importance of preparedness for unforeseen disruptions. Private clouds, with their dedicated infrastructure, offer organizations the ability to establish comprehensive disaster recovery plans. This involves replicating critical data and applications across geographically dispersed private cloud instances, ensuring business operations can swiftly resume in the event of a disaster. The demand for reliable disaster recovery solutions is increasing, driven by the rising frequency of natural disasters and cyber threats. Private cloud providers can capitalize on this opportunity by offering tailored disaster recovery services, providing organizations with the resilience needed to safeguard against data loss and downtime, and meeting regulatory requirements for business continuity planning.

Private Cloud Market Challenges

Interoperability and Standardization Concerns

A significant challenge in the private cloud market is the complexity surrounding interoperability and standardization. Government bodies, such as the National Institute of Standards and Technology (NIST), emphasize the importance of interoperability to ensure seamless communication and data exchange between different cloud environments. However, private clouds may face challenges in integrating with other cloud platforms or hybrid cloud architectures due to varying standards and technologies. This lack of interoperability can hinder organizations seeking a cohesive and flexible cloud ecosystem. The absence of standardized interfaces and protocols poses a significant challenge, complicating efforts to create a unified cloud environment. Addressing this challenge requires collaborative efforts within the industry to establish common standards and interoperability frameworks. The adoption of standardized interfaces would facilitate smoother interactions between private clouds, public clouds, and other IT infrastructure components, enhancing the overall effectiveness and flexibility of cloud deployments.

Talent Shortage and Skilled Workforce

Another notable challenge in the private cloud market is the shortage of skilled professionals with expertise in cloud technologies. Government reports from agencies like the U.S. Department of Labor highlight the growing demand for cloud-related skills, including proficiency in private cloud solutions. The rapid evolution of cloud technologies requires a skilled workforce capable of designing, implementing, and managing private cloud environments effectively. However, there is a shortage of qualified personnel with the necessary expertise in areas such as virtualization, network management, and security within private cloud contexts. This talent shortage can impede the successful deployment and management of private clouds, particularly for small and medium-sized enterprises (SMEs) with limited resources. Addressing this challenge involves investing in educational programs, certifications, and training initiatives to build a skilled workforce capable of navigating the complexities of private cloud technologies, fostering innovation and overcoming the talent gap.

Key Players

Key players operating in the global private cloud market are Cisco, AWS, Microsoft, Dell, Oracle, SAP, Alibaba, IBM, HPE, NTT Data, Rackspace, VMware, and CenturyLink.

PRICE

ASK FOR FREE SAMPLE REPORT