Global Orthopedic Software Market, By Product (Orthopedic Picture Archiving and Communication Systems (PACS), Orthopedic Digital Templating/Preoperative Planning Software, Orthopedic Electronic Health Records, Orthopedic Revenue Cycle Management (RCM), Orthopedic Practice Management), Mode of Delivery (On-Premise, Cloud), Application (Fracture Management, Joint Replacement, Pediatric Assessment), End User (Hospitals, Ambulatory Care Centers), and Region — Industry Analysis and Forecast to 2030

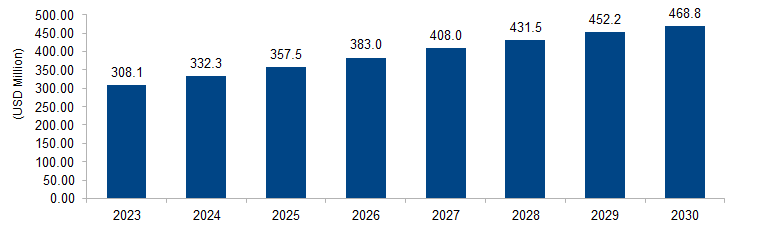

The global orthopedic software market is expected to grow from USD 308.1 million in 2023 to USD 468.8 million by 2030 at a CAGR of 6.2%. The market is driven by the increasing demand for streamlined orthopedic practice management, enhanced patient care, and efficient workflows. The adoption of electronic health records (EHRs) and the integration of orthopedic-specific software solutions aim to optimize clinical operations, improve decision-making, and ultimately enhance the overall quality of orthopedic care.

Figure 1: Global Orthopedic Software Market Size, 2023-2030 (USD Million)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Orthopedic software refers to specialized digital tools designed for the management and optimization of orthopedic healthcare practices. These software solutions cater to the unique needs of orthopedic clinics, hospitals, and healthcare providers by offering features such as electronic health records (EHRs), appointment scheduling, imaging and diagnostic support, billing and coding functionalities, and treatment planning. Orthopedic software aims to streamline administrative tasks, enhance clinical workflows, and improve patient care coordination. By digitizing and centralizing orthopedic-specific information, these software solutions contribute to more efficient practice management, accurate diagnosis, and better overall outcomes in the field of orthopedic healthcare.

Orthopedic Software Market Drivers

Increasing Orthopedic Procedure Volumes and Patient Demands

A key driver fueling the orthopedic software market is the steady increase in orthopedic procedure volumes and growing patient demands for specialized care. As the global population ages, orthopedic conditions such as osteoarthritis and fractures become more prevalent, leading to a surge in the number of orthopedic surgeries and interventions. According to the World Health Organization (WHO), the aging population is a significant contributor to the rise in musculoskeletal disorders. The demand for efficient and specialized orthopedic solutions is further intensified by the increasing expectations of patients for personalized care and improved treatment outcomes. Orthopedic software, equipped with features like digital imaging and treatment planning, addresses the complex requirements of orthopedic procedures, contributing to enhanced diagnostic accuracy and better patient satisfaction.

Regulatory Emphasis on Electronic Health Records (EHRs) and Interoperability

Another driving force in the orthopedic software market is the regulatory emphasis on adopting electronic health records (EHRs) and achieving interoperability in healthcare systems. Government bodies, including the Centers for Medicare & Medicaid Services (CMS) in the United States, are advocating for the implementation of EHRs to improve data accessibility, reduce errors, and enhance overall healthcare quality. The orthopedic software market aligns with these initiatives by offering solutions that not only digitize orthopedic patient records but also facilitate seamless interoperability with broader healthcare ecosystems. The push for standardization and interoperability, as seen in initiatives like the Health Level Seven International (HL7) standards, encourages the integration of orthopedic software into larger health information networks, promoting coordinated care and comprehensive patient information exchange. This regulatory momentum drives the adoption of orthopedic software solutions, ensuring compliance and fostering improved communication and data sharing across the orthopedic care continuum.

Orthopedic Software Market Restraints

Implementation Costs and Resource Constraints

A significant restraint in the orthopedic software market is the high implementation costs associated with adopting and integrating comprehensive orthopedic software solutions. Healthcare providers, particularly smaller orthopedic practices or facilities in resource-constrained settings, may face challenges in allocating financial resources for the upfront costs of acquiring and implementing sophisticated software. The American Hospital Association (AHA) recognizes the financial strain on healthcare organizations, and this is particularly relevant in the orthopedic sector. The need for specialized training, infrastructure upgrades, and ongoing maintenance further adds to the financial burden. As a result, some orthopedic practices may hesitate to invest in advanced software solutions, leading to a slower adoption rate and limiting the overall market growth.

Data Security and Privacy Concerns

Data security and privacy concerns pose a significant restraint to the orthopedic software market. The digitization of patient health records and the transmission of sensitive medical information across networks raise apprehensions about the security of patient data. Regulatory bodies, such as the Health Information Portability and Accountability Act (HIPAA) in the United States, mandate stringent data protection measures. The fear of data breaches, unauthorized access, or cyber-attacks can hinder the willingness of orthopedic practices to fully embrace software solutions. According to the European Data Protection Supervisor (EDPS), healthcare data is particularly vulnerable to privacy risks. Addressing these concerns requires robust security measures, compliance with regulatory standards, and continuous efforts to build trust in the security features of orthopedic software solutions among healthcare providers and patients.

Orthopedic Software Market Opportunities

Remote Patient Monitoring and Telehealth Integration

An emerging opportunity in the orthopedic software market is the integration of remote patient monitoring (RPM) and telehealth capabilities. The global shift towards telehealth, accelerated by the COVID-19 pandemic, has opened avenues for orthopedic software to incorporate features that facilitate remote monitoring of orthopedic patients. Organizations such as the World Health Organization (WHO) recognize telehealth as a valuable tool for expanding access to healthcare services. Orthopedic software can seize this opportunity by enabling virtual consultations, monitoring post-operative recovery remotely, and offering patients real-time guidance on rehabilitation exercises. The integration of telehealth features enhances patient engagement, reduces the need for in-person visits, and contributes to more efficient orthopedic care delivery.

Artificial Intelligence and Predictive Analytics for Treatment Planning

Artificial Intelligence (AI) and predictive analytics present a substantial opportunity for the orthopedic software market in the realm of treatment planning and personalized care. With advancements in AI algorithms and machine learning, orthopedic software can analyze vast datasets, including patient history, imaging studies, and treatment outcomes. The American Academy of Orthopaedic Surgeons (AAOS) recognizes the potential of AI in improving clinical decision-making. Orthopedic software integrated with AI capabilities can provide predictive insights into patient responses to specific treatments, optimize surgical planning, and contribute to more personalized orthopedic care strategies. This opportunity aligns with the broader trend in healthcare towards precision medicine, offering orthopedic practitioners innovative tools for tailoring interventions based on individual patient characteristics and predicting treatment outcomes more accurately.

Orthopedic Software Market Challenges

Interoperability Issues with Diverse Imaging Systems

A significant challenge facing the orthopedic software market is the interoperability issues arising from the diversity of imaging systems used in orthopedic diagnostics. Orthopedic practices utilize various imaging modalities, such as X-rays, MRIs, and CT scans, each with its own proprietary formats and standards. The lack of standardized interoperability can hinder the seamless integration of orthopedic software with diverse imaging systems, leading to difficulties in accessing and exchanging comprehensive patient data. The American College of Radiology (ACR) acknowledges the challenges of achieving interoperability in medical imaging. Overcoming this challenge requires concerted efforts to establish and adhere to standardized imaging protocols, ensuring that orthopedic software can effectively interface with different imaging technologies and facilitate a cohesive approach to patient diagnosis and treatment planning.

Resistance to Workflow Disruptions and Change Management

A notable challenge in the orthopedic software market is the resistance to workflow disruptions and the need for effective change management strategies during software implementation. Orthopedic practices, especially those accustomed to traditional paper-based or legacy systems, may face resistance among clinicians and staff when transitioning to digital solutions. The American Academy of Orthopaedic Surgeons (AAOS) recognizes the importance of minimizing disruptions to clinical workflows during technology adoption. Resistance to change can stem from concerns about disruptions in patient care, the time required for training, and uncertainties about the new system’s efficiency. Overcoming this challenge necessitates thorough change management planning, including comprehensive training programs, communication strategies, and close collaboration with orthopedic practitioners to address their specific workflow needs. Successful change management practices will be crucial in ensuring a smooth transition to orthopedic software solutions without compromising the efficiency and effectiveness of orthopedic care delivery.

Regional Trends

North America: In North America, there is a trend toward increased adoption of orthopedic software solutions, driven by advanced healthcare infrastructure, regulatory support for health information technology, and a focus on improving patient outcomes. The Centers for Medicare & Medicaid Services (CMS) in the United States promotes the use of electronic health records (EHRs) and incentivizes healthcare providers to adopt technology for better care coordination. The region experiences a surge in demand for orthopedic software that integrates with existing systems, enhances diagnostic accuracy, and supports value-based care initiatives.

Europe: Europe sees a trend toward the digital transformation of healthcare, with an emphasis on interoperability and standardized electronic health records. Initiatives like the European Union’s Digital Health and Care Strategy aim to promote the use of digital tools in healthcare. The region experiences a growing interest in orthopedic software solutions that streamline workflows, improve collaboration among healthcare providers, and contribute to better orthopedic patient outcomes.

Asia Pacific: In the Asia Pacific, there is a rising trend in the adoption of orthopedic software solutions, driven by the increasing burden of orthopedic conditions and a growing awareness of the benefits of digital healthcare. Countries like China and India are investing in healthcare infrastructure, and there is a notable interest in solutions that cater to the unique needs of orthopedic practices. The region experiences a trend toward mobile health applications and telemedicine platforms, contributing to the overall growth of orthopedic software solutions.

Middle East and Africa: The Middle East and Africa region show a trend toward incorporating technology in healthcare delivery. Initiatives in countries like the United Arab Emirates focus on digital transformation in healthcare. The region experiences a growing interest in orthopedic software solutions that enhance diagnostic capabilities, improve patient engagement, and contribute to the overall efficiency of orthopedic practices.

Latin America: Latin America sees a growing trend in the adoption of orthopedic software solutions, driven by an evolving healthcare landscape and increasing awareness of the benefits of digital health. Countries like Brazil and Mexico are investing in digital health infrastructure, and there is a notable interest in solutions that streamline orthopedic workflows, enhance diagnostic accuracy, and improve overall patient care.

Key Players

Key players operating in the global orthopedic software market are Brainlab AG, GE Healthcare, Merge Healthcare, Materialise N.V., Philips Healthcare, Medstrat, Inc., CureMD Healthcare, Greenway Health, LLC, Nextgen Healthcare Information Systems, LLC, Allscripts Healthcare Solutions, Inc., Eclinicalworks, McKesson Corporation, Athenahealth, Inc., DrChrono, Exscribe Orthopaedic Healthcare Solutions, Neusoft Medical Systems Co., Ltd, CareCloud Corporation, and Advanced Data Systems Corporation.

PRICE

ASK FOR FREE SAMPLE REPORT