Global Hydrogen Energy Storage Market, By Storage Form (Gas, Liquid, Solid), Technology (Compression, Liquefaction, Material-Based), Application (Stationary Power, Transportation), End User (Electric Utilities, Industrial, Commercial), and Region — Industry Analysis and Forecast to 2030

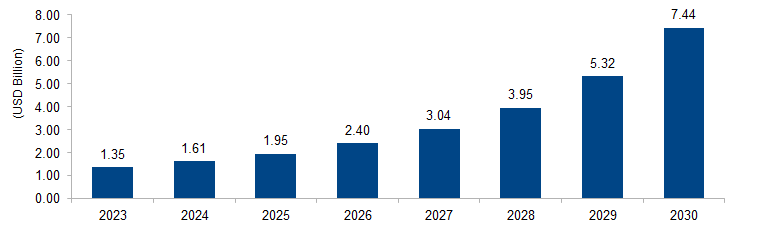

The global hydrogen energy storage market is expected to grow from USD 10.78 billion in 2023 to USD 401.74 billion by 2030 at a CAGR of 67.7%. The hydrogen energy storage market is driven by the global transition to sustainable energy sources and the need for effective energy storage solutions. Hydrogen, as a versatile and clean energy carrier, is gaining prominence for its potential to store renewable energy, address intermittency issues, and contribute to decarbonizing various sectors, including transportation and industry.

Figure 1: Global Hydrogen Energy Storage Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Hydrogen energy storage refers to the process of storing energy in the form of hydrogen gas to be later converted back into electricity or heat when needed. It plays a crucial role in the transition to renewable energy by addressing the intermittency of sources like wind and solar. During periods of excess energy production, surplus electricity is used to electrolyze water, splitting it into hydrogen and oxygen. The hydrogen is then stored, and when energy demand is high, it can be utilized in fuel cells or combustion engines, producing electricity or heat, offering a clean and efficient means of storing and utilizing renewable energy.

Hydrogen Energy Storage Market Drivers

Renewable Energy Integration and Grid Balancing

A significant driver for the hydrogen energy storage market is the increasing need for renewable energy integration and grid balancing. As the world shifts towards sustainable energy sources like wind and solar, the intermittent nature of these resources poses challenges in matching supply with varying demand. Hydrogen energy storage serves as an effective solution by storing excess renewable energy during periods of high production. According to the International Energy Agency (IEA), hydrogen produced from renewable sources could reach a level of 8.3 million tonnes by 2030. The stored hydrogen can then be used during low renewable energy generation to produce electricity or heat, contributing to grid stability and balancing. Governments and energy operators globally are recognizing the potential of hydrogen storage in enhancing the reliability and resilience of renewable energy systems, thereby driving investments and initiatives to accelerate the deployment of hydrogen energy storage technologies.

Decarbonization of Industry and Transportation

Another key driver is the growing emphasis on the decarbonization of industry and transportation. Hydrogen, as a clean energy carrier, is gaining traction as a versatile solution to reduce carbon emissions across various sectors. The European Commission outlines the importance of hydrogen in achieving climate neutrality, with a strategic hydrogen plan aiming for up to 1 million tonnes of renewable hydrogen production by 2024. Hydrogen energy storage facilitates the use of green hydrogen produced from renewable sources in industries like steel and transportation. The ability to store and transport hydrogen provides an avenue for integrating clean energy into sectors that are traditionally challenging to decarbonize. This driver aligns with global commitments to mitigate climate change, and as countries set ambitious targets for reducing greenhouse gas emissions, the hydrogen energy storage market is positioned to play a crucial role in supporting the broader decarbonization agenda.

Hydrogen Energy Storage Market Restraints

Cost Challenges and Infrastructure Investment

A significant restraint for the hydrogen energy storage market is the current high cost associated with hydrogen production, storage, and infrastructure development. The International Renewable Energy Agency (IRENA) highlights that hydrogen from renewable energy is currently more expensive compared to hydrogen produced from fossil fuels. The cost of electrolyzers used in the production of green hydrogen remains a key contributor to the overall expense. Additionally, establishing a dedicated infrastructure for hydrogen storage, transportation, and distribution requires substantial investment. According to the Hydrogen Council, the cost of building hydrogen infrastructure, such as pipelines and storage facilities, is a considerable barrier to the widespread adoption of hydrogen technologies. Overcoming these cost challenges is crucial for making hydrogen energy storage economically competitive, and concerted efforts in research, development, and policy support are needed to drive down costs and encourage broader market adoption.

Limited Scaling and Technical Challenges

Another restraint is the limited scaling of hydrogen energy storage technologies and associated technical challenges. While hydrogen has the potential to play a vital role in large-scale energy storage, current technologies face scalability limitations. The deployment of hydrogen storage on a grid scale is hampered by factors such as the efficiency of electrolyzers, the need for large-scale storage solutions, and the challenges in hydrogen compression and transportation. Technical issues related to the performance and durability of storage materials, such as the impact of hydrogen embrittlement on infrastructure, pose additional challenges. The U.S. Department of Energy (DOE) acknowledges these technical hurdles and emphasizes the importance of research and innovation to address scalability and enhance the overall efficiency of hydrogen energy storage systems. Overcoming these technical challenges is essential for realizing the full potential of hydrogen as a storage solution and ensuring its practical integration into large-scale energy storage applications.

Hydrogen Energy Storage Market Opportunities

Hydrogen as a Chemical Feedstock

One significant opportunity for the hydrogen energy storage market lies in the utilization of hydrogen as a chemical feedstock. Hydrogen’s versatility extends beyond its role as an energy carrier; it can be a crucial raw material in various industrial processes. The European Commission emphasizes the potential of hydrogen in supporting the chemical industry’s transition towards sustainability. Hydrogen can be integrated into the production of ammonia, methanol, and other chemicals, providing an alternative to conventional fossil fuel-based feedstocks. This not only diversifies the applications of hydrogen but also aligns with the global push for greener and more sustainable industrial practices. As industries seek to reduce their carbon footprint and embrace circular economy principles, the hydrogen energy storage market stands to benefit from the expanding role of hydrogen as a feedstock in the chemical sector.

Hydrogen in Power-to-X Applications

Another promising opportunity is the development of Power-to-X applications, where hydrogen is used as a precursor for synthetic fuels and other valuable products. The concept involves converting excess renewable energy into hydrogen through electrolysis and then using the hydrogen as a feedstock for producing synthetic fuels like hydrogen-based aviation fuels or chemicals like synthetic natural gas. The International Energy Agency (IEA) emphasizes the potential of Power-to-X technologies in the transition to a low-carbon energy system. These applications not only offer a means of storing renewable energy but also provide solutions for decarbonizing hard-to-abate sectors like aviation and heavy industry. The Hydrogen Energy Storage Market can tap into this opportunity by playing a crucial role in the production and storage of hydrogen for diverse Power-to-X applications, contributing to the broader efforts towards sustainable and decarbonized energy systems.

Hydrogen Energy Storage Market Challenges

Intermittency and Fluctuations in Renewable Energy Production

A significant challenge for the hydrogen energy storage market is the intermittency and fluctuations in renewable energy production, which directly impact the availability and efficiency of hydrogen production through electrolysis. Renewable energy sources such as wind and solar are inherently variable, with energy production being contingent on weather conditions and time of day. During periods of low renewable energy generation, the availability of excess electricity for electrolysis decreases, affecting the consistent production of hydrogen. The International Renewable Energy Agency (IRENA) notes that addressing the intermittency challenge requires effective coordination between renewable energy generation and hydrogen production, necessitating advanced energy management systems and grid integration strategies. Overcoming this challenge is crucial for ensuring a stable and reliable supply of hydrogen for energy storage, particularly as the share of renewables in the energy mix continues to grow globally.

Infrastructure Development and Standardization

Another substantial challenge is the need for extensive infrastructure development and standardization in the hydrogen value chain. The Hydrogen Council emphasizes the importance of a comprehensive hydrogen infrastructure, including production facilities, transportation, and distribution networks. Developing the necessary infrastructure requires significant investments in building hydrogen pipelines, storage facilities, and refueling stations. Additionally, there is a lack of standardized protocols and regulations for hydrogen production, storage, and transportation. The absence of a standardized framework hinders interoperability and can lead to inefficiencies in the supply chain. Overcoming the challenge of infrastructure development and standardization requires collaborative efforts among governments, industry players, and regulatory bodies to establish a coherent and universally accepted set of standards and guidelines. This will not only facilitate the growth of the hydrogen energy storage market but also promote a seamless and efficient hydrogen ecosystem on a global scale.

Regional Trends

North America: In North America, there has been a growing focus on hydrogen as a key element in the energy transition. The United States, in particular, has seen increased investments in hydrogen-related projects and infrastructure development. The U.S. Department of Energy (DOE) has been actively supporting research and development in hydrogen technologies. A trend in North America involves collaborative efforts between the public and private sectors to promote hydrogen as a clean energy solution. The region has witnessed projects related to Power-to-X applications and the use of hydrogen in sectors such as transportation.

Europe: Europe has been at the forefront of hydrogen adoption, with a strong emphasis on green hydrogen produced using renewable energy sources. The European Union’s Hydrogen Strategy aims to establish Europe as a global leader in hydrogen technologies. Trends in Europe include significant investments in hydrogen infrastructure, such as hydrogen refueling stations and electrolyzer capacity. Germany, in particular, has been a key player in advancing hydrogen technologies, with ambitious targets for green hydrogen production.

Asia Pacific: The Asia Pacific region has shown a keen interest in developing hydrogen economies. Countries like Japan and South Korea have unveiled hydrogen roadmaps and set targets for expanding hydrogen infrastructure. Japan, for example, has been investing in hydrogen production and storage technologies. Australia, with its abundant renewable resources, is exploring opportunities to become a major exporter of green hydrogen. The region is witnessing collaborations between governments and industries to accelerate the adoption of hydrogen energy storage solutions.

Middle East and Africa: In the Middle East, countries with significant oil and gas resources are exploring the potential of hydrogen to diversify their energy portfolios. The Gulf Cooperation Council (GCC) countries have shown interest in both blue and green hydrogen production. The Middle East, known for its large-scale energy projects, may play a crucial role in global hydrogen supply chains. Africa, with its renewable energy potential, is also considering hydrogen as part of its sustainable energy future.

Latin America: Latin America has seen emerging trends in hydrogen adoption, with countries like Chile and Brazil exploring the development of hydrogen projects. Chile, in particular, aims to become a major exporter of green hydrogen due to its favorable renewable energy conditions. Brazil has been exploring hydrogen applications in its energy matrix, particularly in the transportation sector.

Key Players

Key players operating in the global hydrogen energy storage market are Linde PLC, Plug Power Inc., Engie, Iwatani Corporation, Fuelcell Energy, Inc., Storelectric Ltd, Energy Vault, Inc., Power to Hydrogen, Mahytec, Beijing Sinohy Energy Co., Ltd., Hydrogen in Motion, Home Power Solutions (HPS), Lavo System, HDF Energy, GKN Hydrogen, Ergenics Corp., Powertech Labs Inc., and HGO Power.

PRICE

ASK FOR FREE SAMPLE REPORT