Global Hybrid Cloud Market, By Component (Solution, Services), Service Type (Hybrid Hosting, Disaster Recovery, Cloud Management and Orchestration), Service Model (IaaS, PaaS, SaaS), Organization Size, Industry Vertical, and Region – Industry Analysis and Forecast to 2030

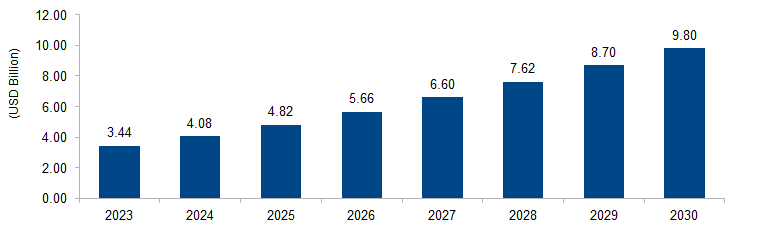

The global hybrid cloud market is expected to grow from USD 3.44 billion in 2023 to USD 9.80 billion by 2030 at a CAGR of 16.1%. The Hybrid Cloud market is driven by the need for a flexible IT infrastructure that combines on-premises and cloud environments. Organizations seek to balance performance, security, and cost-effectiveness by integrating private and public cloud solutions. This approach enables seamless scalability, optimal resource utilization, and accommodates diverse workloads, fostering innovation and agility in a dynamic business landscape.

Figure 1: Global Hybrid Cloud Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Hybrid Cloud refers to a computing environment that combines on-premises infrastructure with public and private cloud services. This approach allows businesses to leverage the benefits of both worlds, integrating the scalability and cost-efficiency of public clouds with the control and security of private clouds and on-premises data centers. Hybrid Cloud solutions enable seamless data and application portability, facilitating dynamic workload distribution. Organizations can optimize performance, enhance flexibility, and address specific compliance or security requirements. This hybrid model supports a more adaptive IT strategy, accommodating varying workloads and providing a balance between the advantages of cloud computing and the control of on-premises infrastructure.

Hybrid Cloud Market Drivers

Scalability and Flexibility for Dynamic Workloads

A prominent driver fueling the growth of the hybrid cloud market is the need for scalability and flexibility to manage dynamic workloads efficiently. Organizations experience fluctuations in computational demands due to seasonal variations, project-specific requirements, or unexpected spikes in user activity. The hybrid cloud model allows businesses to scale their IT resources seamlessly by utilizing the on-demand capacity of public clouds during peak times while maintaining a private infrastructure for baseline workloads. According to a study by the National Institute of Standards and Technology (NIST), 72% of surveyed enterprises reported that scalability was a key factor driving their adoption of Hybrid Cloud. This dynamic scalability not only optimizes resource utilization but also supports business agility, enabling companies to respond promptly to changing demands without overprovisioning hardware resources.

Data Security and Compliance

The imperative for robust data security and compliance is a significant driver propelling the hybrid cloud market. Certain industries, such as finance, healthcare, and government, have stringent regulations governing data storage, transmission, and access. The hybrid cloud model allows organizations to store sensitive or regulated data in private, on-premises environments, addressing concerns about data sovereignty and compliance. According to a report from the European Union Agency for Cybersecurity (ENISA), 68% of businesses cite compliance with data protection regulations as a primary motivator for adopting Hybrid Cloud solutions. By maintaining control over critical data in private clouds while still benefiting from the scalability and cost-effectiveness of public clouds for less sensitive workloads, businesses can navigate complex regulatory landscapes while ensuring the security and integrity of their data.

Hybrid Cloud Market Restraints

Integration Challenges and Interoperability Issues

A significant restraint for the hybrid cloud market is the complexity associated with integrating diverse cloud environments and potential interoperability issues. Organizations often encounter challenges when trying to seamlessly connect on-premises infrastructure with various public and private cloud platforms. According to a study by the Institute of Electrical and Electronics Engineers (IEEE), 56% of businesses identify integration difficulties as a primary obstacle to successful Hybrid Cloud implementation. This complexity can arise from differences in APIs, data formats, and management tools across different cloud providers. Interoperability concerns may result in increased operational complexity, slower deployment times, and compromised efficiency, limiting the benefits organizations seek from adopting a hybrid cloud approach. Addressing these challenges requires standardized practices, open APIs, and collaborative efforts within the industry to ensure a more seamless integration experience for businesses.

Security and Compliance Risks

Security and compliance risks pose a significant challenge to the widespread adoption of hybrid cloud solutions. While hybrid clouds offer the advantage of keeping sensitive data on-premises for enhanced control, the integration with public clouds introduces additional security considerations. According to a report by the National Cyber Security Centre (NCSC), 45% of organizations express concerns about data security when adopting Hybrid Cloud. The complexity of managing security policies across hybrid environments and potential vulnerabilities in data transmission between on-premises and cloud components can lead to increased exposure to cyber threats. Moreover, adherence to industry-specific regulations and compliance standards becomes more intricate in a hybrid environment. Mitigating these risks necessitates robust encryption protocols, comprehensive security frameworks, and ongoing efforts to align hybrid cloud practices with evolving compliance requirements, ensuring a secure and compliant computing environment for organizations.

Hybrid Cloud Market Opportunities

Edge Computing Integration for Low-Latency Applications

An exciting opportunity within the hybrid cloud market lies in the integration of edge computing to cater to low-latency applications. Edge computing involves processing data closer to the source of its generation, reducing latency and enhancing real-time responsiveness. The hybrid cloud model facilitates the seamless integration of edge computing with centralized cloud resources. Spending on edge computing is expected to reach $250 billion by 2024. By combining the scalability and storage capabilities of the cloud with the speed and efficiency of edge computing, organizations can unlock opportunities in areas such as Internet of Things (IoT), autonomous vehicles, and augmented reality, where low-latency processing is crucial. This integration presents a strategic opportunity for hybrid cloud providers to offer comprehensive solutions that meet the diverse computing needs of modern applications.

Industry-Specific Hybrid Cloud Solutions

An emerging opportunity in the hybrid cloud market involves the development of industry-specific solutions tailored to the unique requirements of different sectors. Various industries, such as healthcare, finance, and manufacturing, have distinct compliance, security, and operational needs. According to the Healthcare Information and Management Systems Society (HIMSS), the healthcare sector, in particular, is increasingly adopting Hybrid Cloud solutions to balance data accessibility and security. Hybrid cloud providers can capitalize on this trend by developing specialized offerings that address industry-specific challenges and compliance standards. For instance, customized solutions can cater to the data-intensive nature of genomic research in healthcare or the stringent regulatory requirements in finance. This approach not only enhances the relevance of hybrid cloud solutions across diverse sectors but also allows providers to establish themselves as trusted partners, understanding and addressing the unique demands of each industry.

Hybrid Cloud Market Challenges

Data Transfer Costs and Bandwidth Limitations

A significant challenge facing the hybrid cloud market is the issue of data transfer costs and bandwidth limitations associated with moving large volumes of data between on-premises environments and public clouds. As organizations increasingly adopt hybrid cloud models, they often encounter unexpected costs related to data egress fees. According to a report from the Federal Communications Commission (FCC), businesses can experience substantial expenses when transferring significant amounts of data over networks. Bandwidth limitations further compound this challenge, especially for organizations with extensive datasets or high-frequency data transfers. These constraints can hinder the seamless movement of workloads between environments, impacting operational efficiency and potentially outweighing the cost advantages offered by hybrid cloud solutions. Addressing this challenge requires strategic planning, optimization of data transfer protocols, and consideration of data locality to minimize associated costs and optimize performance.

Skill Gaps and Training Needs

A critical challenge in the hybrid cloud market is the shortage of skilled professionals capable of effectively managing hybrid environments. The complexity of integrating on-premises infrastructure with various public and private cloud platforms demands specialized expertise. According to a report by the European Commission, 43% of businesses identify a lack of skilled personnel as a barrier to adopting advanced digital technologies, including hybrid cloud. The shortage of skilled professionals can lead to suboptimal configurations, increased security risks, and hindered innovation. Addressing this challenge requires comprehensive training programs, certifications, and educational initiatives to equip IT teams with the knowledge and skills necessary for successful hybrid cloud implementation. Collaboration between educational institutions, industry associations, and hybrid cloud providers is essential to bridge the skill gaps and empower organizations to harness the full potential of hybrid computing environments.

Regional Trends

North America: North America has been a prominent market for hybrid cloud adoption, driven by the presence of major cloud providers, advanced IT infrastructure, and a robust digital economy. The United States, in particular, has been at the forefront of hybrid cloud adoption due to its mature cloud ecosystem and a large number of enterprises adopting hybrid cloud strategies.

Europe: Europe has shown significant growth in hybrid cloud adoption, with countries like the United Kingdom, Germany, and France leading the way. Regulatory frameworks such as the General Data Protection Regulation (GDPR) have influenced organizations to adopt hybrid cloud models to ensure compliance while leveraging the benefits of cloud technologies.

Asia-Pacific: The Asia-Pacific region has witnessed a surge in hybrid cloud adoption as organizations look to capitalize on the growing digital economies and leverage cloud technologies for business expansion. Countries like China, India, and Australia have seen increased hybrid cloud deployments, driven by a combination of economic growth, digital transformation initiatives, and investments in cloud infrastructure.

Latin America: Latin America is experiencing a growing demand for hybrid cloud solutions. Brazil, Mexico, and Argentina are among the leading countries adopting hybrid cloud architectures. Organizations in the region are leveraging hybrid cloud to modernize their IT infrastructure, enhance scalability, and enable digital innovation.

Middle East and Africa: The Middle East and Africa region have shown a growing interest in hybrid cloud solutions, driven by the need for digital transformation and the rapid growth of cloud services. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are leading the hybrid cloud adoption in the region.

Key Players

Key players operating in the global hybrid cloud market are CenturyLink, Accenture, AWS, Atos, IBM, Alibaba, Google, Dell EMC, HPE, Microsoft, Oracle, NetApp, NTT Communications, Fujitsu, DXC, VMware, Micro Focus, Rackspace, Pure Storage, Quest Software, Flexera, Unitas, Global, and Citrix.

PRICE

ASK FOR FREE SAMPLE REPORT