Global Hemostats Market, By Type (Oxidized Regenerated Cellulose-Based Hemostats, Thrombin-Based Hemostats, Gelatin-Based Hemostats, Combination Hemostats, Collagen-Based Hemostats), Formulation (Matrix & Gel Hemostats, Sheet & Pad Hemostats, Sponge Hemostats, Powder Hemostats), Application (Orthopedic Surgery, General Surgery, Neurological Surgery, Cardiovascular Surgery, Reconstructive Surgery, Gynecological Surgery), and Region — Industry Analysis and Forecast to 2030

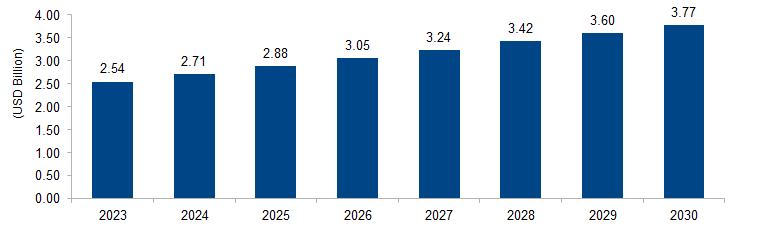

The global hemostats market is expected to grow from USD 2.54 billion in 2023 to USD 3.77 billion by 2030 at a CAGR of 5.8%. The market is primarily driven by the increasing prevalence of surgical procedures globally, fueling the demand for effective and reliable hemostatic agents. Technological advancements in hemostatic products, rising aging population, and a growing emphasis on minimally invasive surgeries further contribute to market growth. Additionally, expanding healthcare infrastructure and awareness about the benefits of hemostats drive market expansion.

Figure 1: Global Hemostats and Sealants Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Hemostats are medical devices or substances used to control bleeding during surgical procedures or to promote coagulation in cases of injury. They work by facilitating blood clotting, preventing excessive bleeding, and ensuring the maintenance of hemostasis. These products can take various forms, including mechanical devices, absorbable agents, or topical applications. Hemostats are crucial in surgeries to minimize blood loss, improve visibility for surgeons, and enhance overall patient outcomes. As advancements in medical technology continue, the development of more efficient and targeted hemostatic solutions plays a pivotal role in improving surgical procedures and patient care across various medical disciplines.

Hemostats and Sealants Market Drivers

Increasing Prevalence of Surgical Procedures

One significant driver propelling the hemostats market is the escalating prevalence of surgical procedures worldwide. As the global population continues to grow and age, there is a parallel rise in the incidence of chronic diseases that often require surgical interventions. According to data from the World Health Organization (WHO), the number of surgeries performed globally has been steadily increasing, with an estimated 313 million surgeries conducted in 2012. Surgical procedures for conditions such as cardiovascular diseases, cancer, and orthopedic issues contribute significantly to this surge.

The demand for hemostatic agents rises in tandem with the expanding scope of surgical interventions. Effective hemostasis is crucial in preventing excessive bleeding during surgeries, minimizing complications, and improving patient outcomes. With an increasing emphasis on enhancing healthcare infrastructure and accessibility, especially in emerging economies, the demand for hemostatic solutions is expected to continue its upward trajectory.

Technological Advancements in Hemostatic Products

Technological advancements in hemostatic products represent another pivotal driver shaping the market landscape. Innovations in materials, formulations, and delivery mechanisms have led to the development of more efficient and targeted hemostatic solutions. For instance, the introduction of advanced hemostatic agents, such as flowable hemostats and sealants, has significantly improved their applicability in diverse surgical scenarios.

The U.S. Food and Drug Administration (FDA) has been instrumental in facilitating the approval of cutting-edge hemostatic products, ensuring their safety and efficacy. This regulatory support encourages manufacturers to invest in research and development, fostering a continuous cycle of innovation. The adoption of hemostats with improved hemostatic performance, reduced side effects, and enhanced biocompatibility contributes to their growing acceptance among healthcare professionals.

As the hemostats market continues to evolve, technological advancements will remain a key driver, providing healthcare providers with increasingly sophisticated tools to address bleeding control challenges in various medical settings.

Hemostats and Sealants Market Restraints

Regulatory Challenges and Approval Processes

One significant restraint in the hemostats market is the stringent regulatory environment and the lengthy approval processes associated with bringing new hemostatic products to market. Regulatory agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have rigorous standards to ensure the safety and efficacy of medical devices. The complex and time-consuming approval procedures can considerably delay the introduction of innovative hemostatic solutions. According to the FDA, the average time for a 510(k) clearance, a common regulatory pathway for medical devices, is around 177 days, subjecting manufacturers to prolonged waiting periods before commercialization. These challenges not only impede the swift entry of novel hemostatic products but also increase development costs, affecting market growth. Moreover, the evolving regulatory landscape adds an additional layer of complexity, requiring companies to stay abreast of changing requirements, further contributing to delays and resource-intensive compliance efforts.

Limited Adoption in Emerging Markets

Another restraint faced by the hemostats market is the limited adoption of advanced hemostatic technologies in emerging economies. While developed regions witness a more extensive integration of innovative hemostats, emerging markets often face challenges related to affordability, awareness, and infrastructure. In many developing countries, there is a preference for traditional hemostatic methods or basic medical supplies due to budget constraints and limited access to advanced healthcare facilities. According to the World Health Organization (WHO), healthcare infrastructure and access to essential medical supplies are often insufficient in low-income countries. This hinders the widespread adoption of sophisticated hemostatic solutions, limiting market expansion in these regions. Moreover, the lack of awareness and education among healthcare professionals and patients about the benefits of advanced hemostats contributes to slower market penetration in emerging economies. Addressing these challenges requires targeted efforts to enhance affordability, education, and healthcare infrastructure in these regions to unlock the full potential of the hemostats market.

Hemostats and Sealants Market Opportunities

Increasing Demand for Hemostats in Ambulatory Surgical Centers

A notable opportunity in the hemostats market lies in the rising demand for these products in ambulatory surgical centers (ASCs). ASCs have gained prominence due to their cost-effectiveness, efficiency, and ability to provide outpatient surgical services. According to the Ambulatory Surgery Center Association (ASCA), there were over 5,800 ASCs in the United States alone in 2020, performing approximately 23 million surgeries annually. As ASCs continue to grow globally, there is a corresponding surge in the need for hemostatic solutions tailored to these settings. Hemostats play a crucial role in ensuring efficient and rapid hemostasis in shorter surgical procedures typically conducted in ASCs. Manufacturers can capitalize on this opportunity by developing hemostatic products that align with the specific requirements and workflows of ASCs, catering to the increasing trend of outpatient surgeries and contributing to overall market expansion.

Technological Advancements and Innovation in Hemostatic Products

The ongoing advancements in medical technology and the continuous innovation in hemostatic products present a significant opportunity for market growth. Novel technologies, such as the development of hemostatic agents with enhanced biocompatibility and reduced side effects, are gaining traction. For instance, the incorporation of nanotechnology in hemostats is showing promise in improving their efficacy. According to a report by the National Center for Biotechnology Information (NCBI), nanotechnology-based hemostatic agents have demonstrated superior hemostatic performance compared to traditional counterparts. Manufacturers can seize this opportunity by investing in research and development to create cutting-edge hemostatic solutions that address unmet clinical needs. Additionally, the integration of smart technologies, such as sensors for real-time monitoring of hemostasis, presents avenues for innovation. Capitalizing on these technological opportunities can not only drive market expansion but also contribute to improved patient outcomes and satisfaction.

Hemostats and Sealants Market Challenges

Price Sensitivity and Cost Barriers

A significant challenge facing the hemostats market is the price sensitivity of consumers and healthcare providers, coupled with the presence of cost barriers that limit the adoption of advanced hemostatic products. According to the World Bank, many countries, especially in developing regions, struggle with economic constraints, making healthcare affordability a critical concern. Advanced hemostatic solutions often involve higher production costs, research and development expenses, and regulatory compliance costs, contributing to elevated market prices. This can pose a challenge for widespread adoption, particularly in regions with limited healthcare budgets. The need for cost-effective solutions becomes crucial to address this challenge, requiring manufacturers to develop strategies that balance innovation with affordability to ensure broader market access without compromising product quality and efficacy.

Variability in Hemostatic Product Efficacy

An inherent challenge in the hemostats market is the variability in the efficacy of different hemostatic products, leading to concerns about their consistent performance across diverse clinical scenarios. The efficacy of hemostatic agents can be influenced by factors such as patient characteristics, surgical procedures, and underlying health conditions. Variability in clotting time and potential adverse reactions pose challenges in predicting and ensuring uniform hemostatic outcomes. Standardizing efficacy across a range of clinical situations is a complex task. This challenge is particularly pronounced with hemostats derived from biological sources, where factors like donor variability and production processes can impact performance. Addressing this challenge requires ongoing research and development efforts to enhance the predictability and reliability of hemostatic products, ensuring consistent effectiveness in diverse clinical settings. Standardization initiatives and collaboration between manufacturers and healthcare institutions are essential to overcome this challenge and build trust in the reliability of hemostatic solutions.

Regional Trends

North America: The North American hemostats market has been witnessing a trend towards increased adoption of advanced hemostatic technologies and products. Factors such as a well-established healthcare infrastructure, high healthcare expenditure, and a growing geriatric population contribute to this trend. Additionally, there is a focus on developing hemostatic solutions tailored to specific medical procedures, contributing to improved patient outcomes.

Europe: In Europe, the hemostats market is influenced by a similar shift towards advanced and innovative products. The region emphasizes regulatory compliance and safety standards, driving research and development efforts for hemostatic solutions. Collaboration between industry players and healthcare institutions is observed to address challenges and promote the adoption of cutting-edge hemostatic technologies.

Asia Pacific: The Asia Pacific region experiences a growing demand for hemostatic products, fueled by an expanding population, increasing awareness about advanced medical technologies, and improving healthcare infrastructure. Governments in countries like China and India are investing in healthcare development, contributing to the growth of the hemostats market. The trend also includes efforts to make advanced hemostatic solutions more accessible and affordable.

Middle East and Africa: The Middle East and Africa are witnessing a gradual increase in the adoption of hemostatic products. Factors such as a rising prevalence of chronic diseases, an improving healthcare landscape, and government initiatives to enhance healthcare services contribute to this trend. There is also a focus on addressing specific healthcare challenges in the region, such as trauma-related injuries, which can benefit from advanced hemostatic solutions.

Latin America: Latin America is experiencing a trend towards the adoption of hemostatic technologies, driven by improving economic conditions and healthcare infrastructure in certain countries. Governments are working on enhancing healthcare accessibility, contributing to the demand for medical products, including hemostats. The market in Latin America reflects a growing awareness of the importance of effective hemostatic solutions in various medical procedures.

It’s crucial to note that the trends mentioned are based on general observations and the situation might have evolved. For the most up-to-date and accurate information, consulting recent reports from market research firms or relevant government agencies is recommended.

Key Players

Key players operating in the global hemostats market are Johnson & Johnson, Baxter International, B. Braun SE, Pfizer Inc., BD, Teleflex Incorporated, Hemostasis, LLC, Medtronic PLC, Stryker Corporation, Advanced Medical Solutions Group PLC, Medtronic PLC, Samyang Holdings Corporation, Gelita Medical GmbH, Dilon Technologies, Inc., Marine Polymer Technologies, Inc., Betatech Medical, BioCer Entwicklungs-GmbH, and Meril Life Sciences Pvt. Ltd.

PRICE

ASK FOR FREE SAMPLE REPORT