Global Fraud Detection and Prevention Market, By Component (Solutions, Services), Application (Payment Fraud, Money Laundering, Identity Theft), Deployment Mode (Cloud, On-premises), Organization Size, Industry Vertical, and Region – COVID-19 Pandemic Impact Analysis and Forecast to 2028

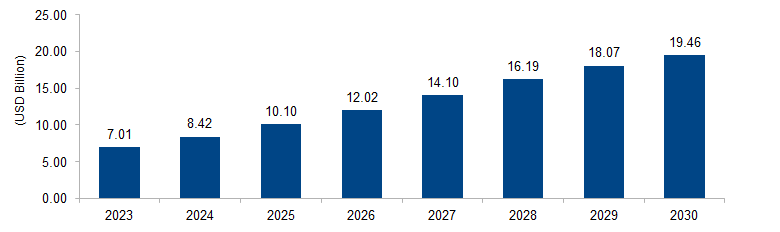

The global fraud detection and prevention market is expected to grow from USD 7.01 billion in 2023 to USD 19.46 billion by 2030 at a CAGR of 15.7%. The market is driven by factors such as the increasing incidents of fraud, regulatory compliance, technological advancements, the growth of e-commerce, rising awareness, and the integration of real-time monitoring capabilities. By understanding and addressing these driving factors, businesses can stay ahead in the evolving landscape of fraud detection and prevention.

Figure 1: Global Fraud Detection and Prevention Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Fraud detection and prevention refers to the process of identifying and mitigating fraudulent activities within various domains, such as financial transactions, online platforms, insurance claims, and more. Fraud can take many forms, including identity theft, credit card fraud, phishing scams, and insider threats, among others. The primary objective of fraud detection and prevention is to safeguard individuals, organizations, and systems from financial losses, reputational damage, and legal liabilities.

Detection involves the use of advanced technologies, data analysis techniques, and intelligent algorithms to identify patterns, anomalies, and suspicious behaviors that indicate fraudulent activities. This can include analyzing transactional data, monitoring user behavior, examining system logs, and employing machine learning models to detect and flag potential fraudulent incidents.

Prevention focuses on implementing robust security measures and controls to minimize the occurrence and impact of fraud. This includes implementing multi-factor authentication, encryption, secure communication protocols, and access controls to protect sensitive information and systems. Additionally, training and awareness programs are crucial for educating individuals about common fraud schemes and promoting a culture of vigilance.

Fraud Detection and Prevention Market Drivers

Increasing instances of fraud

As the world becomes more digitally connected, fraudsters are finding new and sophisticated ways to carry out fraudulent activities. This has resulted in a significant rise in fraudulent incidents across various industries and sectors.

With the expansion of online transactions, digital payment systems, and e-commerce platforms, fraudsters have more opportunities to exploit vulnerabilities and target individuals and organizations. They employ tactics such as identity theft, credit card fraud, account takeovers, and phishing scams to gain unauthorized access to sensitive information and financial assets.

To combat these threats, businesses and individuals are recognizing the importance of implementing robust fraud detection and prevention solutions. Such solutions leverage advanced technologies, data analytics, and machine learning algorithms to identify patterns, anomalies, and suspicious behaviors that indicate fraudulent activities. By analyzing vast amounts of data, these systems can detect fraudulent transactions, flag suspicious user behavior, and prevent unauthorized access to sensitive information.

The increasing incidents of fraud also drive the need for organizations to invest in fraud prevention measures to protect their customers and maintain their reputation. Customer trust is paramount in today’s digital landscape, and organizations must take proactive steps to ensure the security of their transactions and protect customer data.

Furthermore, the rise in fraudulent incidents has caught the attention of regulatory bodies and governments worldwide. They are imposing stringent regulations and compliance requirements to safeguard consumer interests and prevent financial crimes. This regulatory pressure further compels organizations to invest in robust fraud detection and prevention solutions to meet these requirements and avoid penalties, resulting into high growth of the fraud detection and prevention market.

Stringent Regulatory Compliance

Governments and regulatory bodies across the globe are imposing strict regulations and guidelines to combat fraud and protect consumer interests. These regulations require businesses to implement effective fraud detection and prevention measures to ensure compliance and avoid penalties.

Regulatory bodies, such as financial authorities and data protection agencies, are increasingly focusing on enhancing security measures and preventing financial crimes. They set forth guidelines and standards that organizations must follow to safeguard customer information, prevent identity theft, and ensure secure transactions.

Compliance with these regulations is not only essential for legal adherence but also for maintaining the trust and confidence of customers. Failure to comply can result in severe financial and reputational consequences for businesses.

To meet regulatory requirements, organizations need to invest in advanced fraud detection and prevention solutions. These solutions employ cutting-edge technologies, such as artificial intelligence, machine learning, and data analytics, to detect and prevent fraudulent activities. By leveraging these technologies, businesses can identify patterns, anomalies, and suspicious behaviors that may indicate fraudulent transactions or activities.

Additionally, compliance-driven fraud detection and prevention solutions provide features like audit trails, robust authentication mechanisms, encryption, and secure communication protocols. These features help organizations maintain comprehensive records of transactions, protect sensitive data, and ensure compliance with data protection regulations. These factors boost the growth of the fraud detection and prevention market.

Fraud Detection and Prevention Market Restraints

High cost of implementation

The high cost of implementation presents a significant restraint in the fraud detection and prevention market. While businesses acknowledge the importance of investing in robust solutions to combat fraud, the associated expenses can pose a considerable barrier.

Implementing effective fraud detection and prevention measures necessitates a robust technology infrastructure. This includes hardware, software, and cybersecurity measures. Acquiring and maintaining this infrastructure can be costly, especially for smaller organizations with limited resources.

Data collection and analysis are vital components of fraud prevention. Organizations need to gather and analyze vast amounts of data, such as transactional records and user behavior patterns, to identify potential fraudulent activities. This process requires advanced analytics tools and skilled data scientists, which adds to the overall cost.

Building a competent team of fraud detection and prevention experts also contributes to the high implementation costs. Skilled professionals who understand fraud patterns and emerging trends are in high demand and often require competitive salaries to attract and retain them.

Continuous updates and maintenance are essential to keep fraud detection and prevention systems effective. Regular updates and enhancements are necessary to stay ahead of evolving fraud tactics. Organizations must invest in ongoing system improvements, software updates, and training programs, all of which add to the overall cost.

Integration challenges further amplify the high cost of implementation. Integrating fraud detection and prevention solutions with existing IT infrastructure can be complex and time-consuming. Customization, integration with legacy systems, and extensive testing are often required, requiring additional resources and increasing costs. These factors restrain growth of the fraud detection and prevention market.

To address cost concerns, businesses can explore strategies such as leveraging cloud-based solutions for scalability and cost-effectiveness, outsourcing certain aspects of fraud prevention, and utilizing open-source tools and platforms.

Data privacy concerns

In an era marked by increasing data breaches and cyberattacks, individuals are becoming more aware of their privacy rights and the security of their personal information. There is a mounting demand for stricter data protection regulations and greater transparency from organizations concerning their data handling practices.

Data privacy concerns arise due to several factors. Firstly, fraud detection and prevention often require access to sensitive personal information, including financial data, transaction records, and user behavior patterns. Individuals are understandably concerned about the potential misuse or unauthorized access to their personal information, which could lead to identity theft or other privacy breaches.

Secondly, organizations must comply with data protection regulations imposed by governments worldwide. Regulations such as the European Union’s General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) mandate stringent requirements on data handling, consent, and security measures. Non-compliance with these regulations can result in severe penalties and reputational damage for organizations.

Thirdly, data sharing and cross-border transfers are common practices in fraud detection and prevention. Collaboration between entities often involves the exchange of data for effective fraud mitigation. However, this raises concerns about data security and the potential for unauthorized access or use of the shared information. Issues surrounding the lawful transfer of data across jurisdictions with varying data protection laws further exacerbate privacy concerns, acting as restraining factors for the fraud detection and prevention market.

Fraud Detection and Prevention Market Opportunities

Integration of Multichannel Fraud Prevention

The integration of multichannel fraud prevention represents a significant opportunity in the fraud detection and prevention market. As digital transactions and interactions continue to proliferate across various channels, fraudsters are finding new ways to exploit vulnerabilities. Organizations can leverage this opportunity by implementing a comprehensive and unified approach to fraud prevention across multiple channels, including online platforms, mobile applications, and point-of-sale systems.

By integrating multichannel fraud prevention, organizations can create a seamless and secure experience for customers while effectively detecting and preventing fraud attempts. This approach enables a holistic view of customer behavior, transactions, and interactions, allowing for more accurate fraud detection and risk assessment.

One key advantage of multichannel fraud prevention is the ability to identify patterns and anomalies across different channels. By correlating data from various sources, organizations can detect suspicious behaviors that may be indicative of fraudulent activities. For example, if a customer’s account shows unusual login patterns combined with suspicious transaction activity, an integrated multichannel fraud prevention system can raise an alert and trigger further investigation.

Furthermore, integrating fraud prevention across multiple channels enables organizations to leverage data and insights from one channel to strengthen the fraud prevention capabilities of others. For instance, if a fraudulent transaction is detected on a mobile app, that information can be used to strengthen the security measures on the website or in physical point-of-sale systems. This proactive sharing of information and detection strategies helps organizations stay ahead of evolving fraud tactics. These factors provide new growth opportunities to the fraud detection and prevention market.

Technological Advancements

Technological advancements present a significant opportunity in the fraud detection and prevention market. With rapid developments in technologies such as artificial intelligence (AI), machine learning (ML), and big data analytics, organizations can leverage these advancements to enhance their fraud detection capabilities and stay ahead of evolving fraud tactics.

AI and ML algorithms enable organizations to analyze large volumes of data in real-time, identifying patterns, anomalies, and suspicious behaviors that indicate potential fraudulent activities. These technologies can automate the process of fraud detection, significantly improving accuracy and efficiency compared to traditional manual methods. Machine learning models can learn from historical data, adapt to new fraud patterns, and continuously enhance detection capabilities.

Big data analytics plays a crucial role in fraud detection and prevention by allowing organizations to process and analyze vast amounts of structured and unstructured data. By integrating various data sources, including transactional data, user behavior data, and external data feeds, organizations can gain deeper insights and a comprehensive view of potential fraud risks. Advanced analytics techniques, such as network analysis and behavioral profiling, help identify hidden relationships and uncover complex fraud schemes.

Moreover, advancements in real-time monitoring technologies enable organizations to detect and respond to fraudulent activities in real-time or near real-time. Real-time monitoring allows for immediate identification of suspicious transactions, account takeovers, or other fraudulent behaviors, enabling timely intervention and prevention of financial losses. Thus, these technological advancements offer new opportunities to the fraud detection and prevention market.

Fraud Detection and Prevention Market Challenges

Evolving Fraud Tactics

One of the significant challenges in the fraud detection and prevention market is the ever-evolving nature of fraud tactics. Fraudsters are constantly adapting their strategies to exploit vulnerabilities, leveraging advancements in technology and finding new ways to circumvent detection systems. As organizations implement sophisticated fraud prevention measures, fraudsters respond by developing more sophisticated methods to bypass these systems, making it increasingly difficult to detect and prevent fraud effectively.

The dynamic landscape of fraud requires continuous vigilance, proactive monitoring, and constant updates to fraud detection systems. Organizations must invest in research and development to understand emerging fraud tactics, collaborate with industry peers and law enforcement agencies, and leverage technologies such as artificial intelligence (AI) and machine learning (ML) to identify and adapt to new fraud patterns.

To tackle the challenge of evolving fraud tactics, organizations need to stay agile and proactive. They should establish robust fraud intelligence capabilities to monitor the latest fraud trends, stay updated on emerging techniques, and quickly respond to new threats. Collaboration with other organizations in the industry can help share knowledge and best practices, enabling a collective defense against fraudsters.

Balancing Accuracy and False Positives

Balancing accuracy and minimizing false positives is a critical challenge in the fraud detection and prevention market. While it is crucial to identify and prevent fraudulent activities, an overly strict approach can lead to a high number of false positives. False positives occur when legitimate transactions or activities are wrongly flagged as fraudulent, causing customer frustration, delays, and potential reputational damage.

Data quality and feature selection are essential considerations in achieving accurate fraud detection. Organizations should ensure that the data used for training and testing their fraud detection models is comprehensive, up-to-date, and representative of real-world scenarios. Additionally, using advanced feature engineering techniques and incorporating contextual information can enhance the accuracy of fraud detection algorithms.

Moreover, implementing intelligent risk-scoring models can help organizations differentiate between legitimate transactions and fraudulent activities more effectively. These models assign risk scores to transactions based on various factors, including transaction patterns, historical behavior, and known fraud indicators. By setting appropriate risk thresholds, organizations can balance the need for accurate fraud detection while minimizing false positives.

Continuous optimization and improvement are key to maintaining an effective balance between accuracy and false positives. Organizations should analyze historical data, monitor performance metrics, and incorporate feedback loops into their fraud detection systems. Machine learning algorithms that can learn from past outcomes and adapt to changing fraud patterns play a crucial role in reducing false positives over time.

Regional Trends

North America: North America, particularly the US, has been at the forefront in the fraud detection and prevention market due to its highly developed financial and technological sectors. The region has witnessed significant investments in advanced fraud prevention technologies, including AI and ML, to combat sophisticated fraud schemes. Stringent regulations, such as the Payment Card Industry Data Security Standard (PCI DSS) and the Bank Secrecy Act (BSA), have driven the adoption of robust fraud prevention measures.

Europe: European countries have been proactive in implementing data protection regulations, with the General Data Protection Regulation (GDPR) being a prominent example. These regulations have prompted organizations to prioritize data privacy and security in their fraud prevention strategies. The European market has also seen collaborations between financial institutions, law enforcement agencies, and industry bodies to share information and combat cross-border fraud.

Asia Pacific: The Asia Pacific region is experiencing significant growth in digitalization, e-commerce, and mobile payment adoption, leading to an increased risk of fraud. This has driven the demand for advanced fraud detection and prevention solutions. Developing economies in the region, such as China and India, have witnessed a surge in fraud prevention investments and the adoption of technologies like biometrics for secure authentication.

Latin America: Latin American countries have seen a rise in e-commerce activities and digital payment adoption, accompanied by an increased focus on fraud prevention. Regulatory initiatives to combat money laundering and financial crimes have driven the implementation of robust fraud detection measures. Collaborative efforts among financial institutions and government agencies to share fraud intelligence have gained traction in the region.

Middle East and Africa: The Middle East and Africa region have witnessed rapid digital transformation, particularly in the financial services sector. As digital payment systems gain prominence, the focus on fraud detection and prevention has increased. Regulatory frameworks and compliance requirements have been established to address fraud risks, leading to investments in advanced fraud prevention solutions.

Key Players

Key players operating in the global fraud detection and prevention market are FICO, Fiserv, IBM, FIS Global, Securonix, Experian, Lexisnexis Risk Solutions, ACI Worldwide, Kount, Wirecard, DXC, BAE Systems, Dell EMC, SAS, MaxMind, SAP, Simility, First Data, Software AG, NICE, AppGate, Guardian Analytics, FRISS, and Iovation.

PRICE

ASK FOR FREE SAMPLE REPORT