Global Electric Powertrain Market, By Vehicle Type (PHEVS, BEVS, 48V MHEVS, FCEVS), Type (BEV Powertrain, MHEV Powertrain, Series Hybrid Powertrain, Parallel Hybrid Powertrain, Series-Parallel Hybrid Powertrain), and Region — Industry Analysis and Forecast to 2030

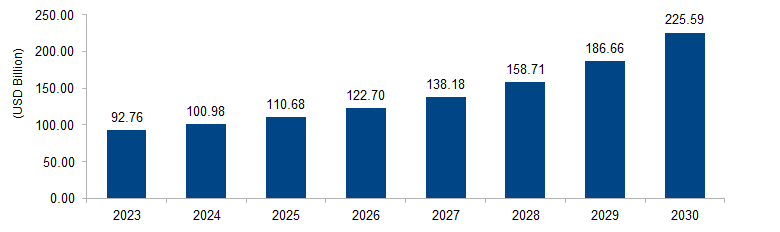

The global electric powertrain market is expected to grow from USD 92.76 billion in 2023 to USD 225.59 billion by 2030 at a CAGR of 13.5%. The market is driven by the global transition towards sustainable mobility. Stringent emission regulations, coupled with a growing environmental consciousness, propel the demand for electric vehicles (EVs) and, consequently, electric powertrains. Advancements in battery technology, government incentives, and consumer preferences for eco-friendly transportation contribute to the expanding market for electric powertrains, fostering innovation and market growth.

Figure 1: Global Electric Powertrain Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

An electric powertrain refers to the integral components in an electric vehicle (EV) that facilitate the conversion of electrical energy into mechanical power for propulsion. Comprising an electric motor, power electronics, and a battery, the powertrain eliminates traditional internal combustion engines. The electric motor serves as the primary source of propulsion, drawing power from the battery, which stores electrical energy. Power electronics control the flow of electricity between the battery and the motor. This technology is at the core of electric vehicles, providing an eco-friendly alternative to traditional fossil fuel-powered vehicles, promoting energy efficiency, reduced emissions, and advancements in sustainable transportation.

Electric Powertrain Market Drivers

Stringent Emission Regulations

A primary driver of the electric powertrain market is the global enforcement of stringent emission regulations by governments. To combat climate change and reduce air pollution, regulatory bodies such as the European Union and the Environmental Protection Agency (EPA) in the United States have imposed strict emission standards on the automotive industry. For instance, the EU has set ambitious targets to lower the average CO2 emissions from new cars. The automotive sector’s response to these regulations is a significant shift towards electric powertrains to meet emission reduction goals. The adoption of electric vehicles (EVs) with zero tailpipe emissions becomes imperative for automakers to comply with these regulations. This trend is pushing the electric powertrain market forward, encouraging innovations in battery technology and electric drivetrains to create environmentally friendly vehicles that align with regulatory standards.

Increasing Consumer Demand for Electric Vehicles

Another key driver is the increasing consumer demand for electric vehicles, propelling the growth of the electric powertrain market. Consumers are becoming more environmentally conscious, seeking sustainable transportation options. According to the International Energy Agency (IEA), the global electric car stock surpassed 10 million vehicles in 2020. The rising awareness of climate change, coupled with government incentives and subsidies for EV purchases, is driving consumers towards electric vehicles equipped with advanced powertrains. As consumers prioritize eco-friendly and cost-effective mobility solutions, automakers are compelled to invest in electric powertrain technologies to meet this growing demand. The Electric Powertrain Market benefits from this consumer shift, with manufacturers focusing on developing efficient, high-performance electric powertrains to cater to the expanding market for electric vehicles globally.

Electric Powertrain Market Restraints

Infrastructure Challenges and Range Anxiety

A significant restraint in the electric powertrain market is the existing challenges related to charging infrastructure and the prevalence of range anxiety among consumers. While electric vehicle (EV) adoption is growing, the availability and accessibility of charging stations remain a concern. According to the International Energy Agency (IEA), a lack of charging infrastructure is a barrier to EV uptake. Range anxiety, the fear of running out of battery power before reaching a charging station, further hinders widespread adoption. Addressing this restraint requires substantial investments in charging infrastructure expansion. Governments globally need to collaborate with industry stakeholders to accelerate the deployment of charging stations. Additionally, innovative solutions such as fast-charging technologies are essential to alleviate range anxiety, offering consumers a convenient and efficient charging experience. Until these infrastructure challenges are effectively addressed, the electric powertrain market may face limitations in achieving widespread consumer acceptance and market growth.

High Initial Costs and Affordability Concerns

Another restraint in the electric powertrain market is the high initial costs associated with electric vehicles (EVs) and their powertrains, leading to affordability concerns for consumers. Despite decreasing battery costs, EVs still tend to have higher upfront prices compared to traditional internal combustion engine vehicles. Government incentives and subsidies play a crucial role in mitigating this restraint. For example, the U.S. federal government offers tax credits for EV purchases to promote affordability. However, such incentives vary globally, impacting consumer decisions. The International Council on Clean Transportation (ICCT) notes that the affordability gap between electric and conventional vehicles remains a challenge. To overcome this restraint, ongoing efforts are needed to further reduce battery costs, increase economies of scale in production, and implement consistent and substantial incentives to make electric powertrains and EVs more accessible to a broader consumer base.

Electric Powertrain Market Opportunities

Grid Integration and Vehicle-to-Grid (V2G) Technology

An opportunity in the electric powertrain market lies in the advancement of grid integration and Vehicle-to-Grid (V2G) technology. As the electric vehicle (EV) fleet grows, there is potential for these vehicles to serve as mobile energy storage units. V2G technology enables bidirectional energy flow between EVs and the electrical grid. According to the U.S. Department of Energy (DOE), V2G technology can enhance grid stability and reliability. EVs can be used to store excess renewable energy and supply it back to the grid during peak demand, contributing to grid balancing. This presents an opportunity for the electric powertrain market to play a crucial role in the broader energy ecosystem. Manufacturers can explore innovations in V2G technology, creating intelligent powertrains that not only power vehicles but also contribute to a more resilient and sustainable energy infrastructure.

Development of Lightweight and High-Efficiency Components

Another significant opportunity lies in the development of lightweight and high-efficiency components for electric powertrains. The weight of components directly impacts the overall efficiency and range of electric vehicles (EVs). According to the National Renewable Energy Laboratory (NREL), advancements in lightweight materials and efficient design can enhance EV performance. Manufacturers can explore opportunities to innovate in materials science and engineering, focusing on components such as electric motors, power electronics, and battery systems. By developing lightweight and energy-efficient components, the electric powertrain market can contribute to extending the range of EVs, improving overall efficiency, and addressing consumer concerns related to range anxiety. This opportunity aligns with the broader goals of creating more sustainable and practical electric vehicles, enhancing the competitiveness and attractiveness of electric powertrains in the automotive market.

Electric Powertrain Market Challenges

Material Supply Chain Constraints

A significant challenge in the electric powertrain market is the potential for constraints in the supply chain of critical materials used in electric vehicle (EV) components. The increased demand for EVs, particularly for their powertrains, places pressure on the availability of essential materials such as rare earth elements, lithium, and cobalt. According to the World Bank, the demand for lithium, a key component in EV batteries, is expected to increase significantly. Supply chain disruptions or shortages of these materials can impact manufacturing timelines and lead to increased costs. This challenge necessitates strategic planning by industry stakeholders to diversify material sources, invest in recycling technologies, and explore alternative materials for sustainable and resilient supply chains. Overcoming material supply chain constraints is crucial for the electric powertrain market to maintain growth and sustainability amid rising demand for electric vehicles.

Standardization and Interoperability Issues

Another challenge in the electric powertrain market is the need for standardization and interoperability in charging infrastructure. As electric vehicles (EVs) become more prevalent, different regions and stakeholders are implementing diverse charging standards and protocols. The absence of global standardization can lead to interoperability issues, making it challenging for EV users to access charging networks seamlessly. The International Electrotechnical Commission (IEC) and other organizations are working on standardization efforts, but a lack of uniformity remains. This challenge requires collaborative efforts among governments, industry players, and standardization bodies to establish common charging standards globally. Ensuring interoperability is essential for promoting widespread EV adoption by providing a user-friendly charging experience, reducing barriers for consumers, and fostering the continued growth of the electric powertrain market.

Regional Trends

North America: Trends in North America may include a continued push towards electric vehicle adoption with an emphasis on incentives and policies promoting cleaner transportation. The United States, for instance, has federal tax credits for EV purchases, and various states offer additional incentives. The development of charging infrastructure and the integration of EVs into smart grids could be notable trends.

Europe: Europe is likely to see a surge in electric vehicle sales driven by ambitious emission reduction goals. The European Union has set strict CO2 emission standards for new cars, stimulating the adoption of electric powertrains. Trends may also include advancements in battery technologies and the expansion of charging infrastructure to support the growing EV market.

Asia Pacific: In the Asia Pacific region, trends may revolve around the dominance of electric vehicle markets, particularly in China. Government support and regulations promoting electric mobility, along with advancements in EV technology, could drive the electric powertrain market. The region might also witness increased investments in research and development for battery technologies.

Middle East and Africa: Trends in the Middle East and Africa may include the adoption of electric powertrains in response to increasing concerns about air quality and a desire to diversify energy sources. Countries in the region could invest in electric infrastructure, and the market might witness a gradual but growing interest in electric mobility.

Latin America: Latin America might experience trends related to urbanization and the need for sustainable transportation solutions. Governments could implement policies to incentivize electric vehicle adoption, and market trends may include the development of electric powertrain technologies suitable for the region’s unique geographic and economic conditions.

Key Players

Key players operating in the global electric powertrain market are Robert Bosch GmbH, Mitsubishi Electric Corporation, Continental AG, Magna International Inc., Hitachi Astemo, Ltd., ZF Friedrichshafen AG, Borgwarner Inc., Denso Corporation, Dana Incorporated, Valeo S.A., Brusa Elektronik AG, NIDEC CORPORATION, Magneti Marelli Ck Holdings, Kelly Controls, Toyota Industries Corporation, Panasonic, Filtran LLC, and Curtis Instruments.

PRICE

ASK FOR FREE SAMPLE REPORT