Global Electric Commercial Vehicle Market, By Body Construction (Integrated, Semi-Integrated, Full-Size), Vehicle Type (Pickup Trucks, Trucks, Vans, Buses & Coaches), Propulsion (BEVS, FCEVS), Battery Type (NMC Batteries, LFP Batteries, Solid-State Batteries), Battery Capacity (Less Than 60 kWh, 60-120 kWh, 121-200 kWh, 201-300 kWh, 301-500 kWh, 501-1000 kWh), Power Output (<100 kW, 100-250 kW, >250 kW), Range (Less Than 150 Miles, 151-300 Miles, Above 300 Miles), End Use (Last-Mile Delivery, Distribution Services, Field Services, Long-Haul Transportation, Refuse Trucks), and Region — Industry Analysis and Forecast to 2030

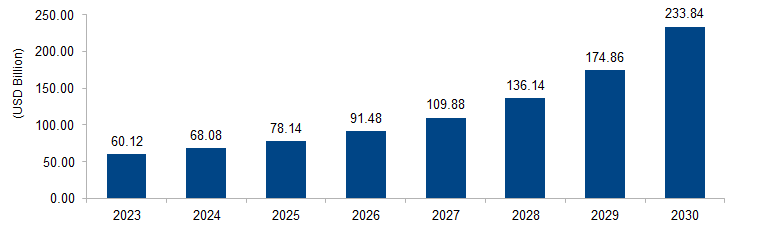

The global electric commercial vehicle market is expected to grow from USD 60.12 billion in 2023 to USD 233.84 billion by 2030 at a CAGR of 21.4%. The market is driven by the global shift towards sustainable transportation, with a focus on reducing emissions and dependence on traditional fuels. Stringent environmental regulations, lower operational costs, and advancements in battery technology propel the adoption of electric commercial vehicles. Companies are increasingly embracing eco-friendly fleets, contributing to the growth of this market.

Figure 1: Global Electric Commercial Vehicle Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

An electric commercial vehicle refers to a mode of transportation designed for commercial or industrial purposes that relies on electric propulsion. Unlike traditional vehicles powered by internal combustion engines, electric commercial vehicles use electric motors and rechargeable batteries for operation. This includes a diverse range of vehicles such as electric delivery vans, trucks, buses, and utility vehicles. The primary aim is to reduce environmental impact by minimizing emissions and dependence on fossil fuels. Electric commercial vehicles contribute to sustainable transportation solutions, offering businesses a means to lower operational costs, comply with stringent emission standards, and participate in the global transition towards cleaner and more energy-efficient mobility.

Electric Commercial Vehicle Market Drivers

Environmental Regulations and Emission Reduction Goals

A significant driver propelling the electric commercial vehicle market is the global focus on environmental sustainability and the implementation of stringent regulations aimed at reducing vehicle emissions. Governments worldwide are increasingly adopting measures to address air quality concerns and combat climate change. For instance, the European Union has set ambitious emission reduction targets, including a plan to cut CO2 emissions from trucks by 30% by 2030. Such regulatory initiatives create a compelling incentive for businesses to adopt electric commercial vehicles, which contribute to lower carbon footprints and help companies meet emission reduction goals. The pressure to comply with these standards encourages the transition to electric fleets, shaping the market landscape with a projected increase in the adoption of electric delivery vans and trucks.

Total Cost of Ownership (TCO) Benefits and Government Incentives

The Total Cost of Ownership (TCO) advantages associated with electric commercial vehicles serves as a key driver in their market growth. While the initial purchase cost of electric vehicles may be higher, the lower operating and maintenance costs over the vehicle’s lifecycle contribute to a favorable TCO. According to the U.S. Department of Energy, the fuel and maintenance savings for electric commercial vehicles can be substantial. Governments and authorities worldwide are recognizing the role of incentives in accelerating the transition to electric mobility. Incentives such as tax credits, rebates, and grants are being offered to businesses investing in electric commercial vehicles. For example, the Federal Transit Administration in the US provides grants to support the deployment of electric buses. These incentives not only make electric commercial vehicles more economically attractive but also stimulate market growth by encouraging businesses to embrace sustainable and cost-effective transportation solutions.

Electric Commercial Vehicle Market Restraints

Infrastructure Limitations and Charging Challenges

A prominent restraint in the electric commercial vehicle market is the existing limitations in charging infrastructure, which can impede widespread adoption. While governments and private entities are investing in expanding charging networks, challenges persist. According to the International Energy Agency (IEA), the growth of public charging infrastructure has not kept pace with the increasing number of electric vehicles. This is particularly critical for electric commercial vehicles that often require fast and reliable charging solutions to minimize downtime during operations. In the absence of a robust and accessible charging infrastructure, businesses may hesitate to invest in electric commercial vehicles, fearing disruptions in their logistics and transportation activities. Overcoming this restraint necessitates substantial investment in charging infrastructure development, addressing concerns related to charging station availability, compatibility, and charging speeds to facilitate the seamless integration of electric commercial vehicles into diverse fleets.

Initial Purchase Cost and Battery Technology Challenges

The high initial purchase cost of electric commercial vehicles stands as a significant restraint in their market penetration. According to the U.S. Department of Energy, the upfront cost of electric vehicles, including commercial ones, is often higher than their conventional counterparts. This cost disparity, even with potential long-term savings in operational expenses, can pose a financial barrier for businesses, especially smaller enterprises or those operating on thin profit margins. Additionally, battery technology challenges contribute to the overall cost constraints. The limited energy density and the cost of manufacturing high-capacity batteries impact the feasibility of electric commercial vehicles. Despite ongoing advancements, the costs associated with electric vehicle batteries remain substantial. Addressing this restraint involves continued research and development to improve battery technology, enhance energy storage capabilities, and ultimately bring down the overall cost of electric commercial vehicles to make them more economically competitive in the market.

Electric Commercial Vehicle Market Opportunities

Grid Integration and Vehicle-to-Grid (V2G) Technology

An opportunity for the electric commercial vehicle market lies in the advancement of grid integration and Vehicle-to-Grid (V2G) technology. V2G enables electric vehicles, including commercial ones, to not only consume energy from the grid but also feed excess energy back into it when needed. This bidirectional energy flow opens avenues for businesses to actively participate in energy markets and grid balancing. According to the European Commission, V2G technology has the potential to create a more stable and resilient energy grid while offering revenue-generating opportunities for vehicle owners. Electric commercial vehicles, when connected to the grid, can act as mobile energy storage units, contributing to grid stability during peak demand periods. This dual functionality transforms electric commercial vehicles into valuable assets in the broader energy ecosystem, providing businesses with the opportunity to optimize energy usage, reduce costs, and contribute to a more sustainable and resilient energy infrastructure.

Last-Mile Delivery Optimization and Urban Mobility Solutions

The rise of e-commerce and the increasing demand for last-mile delivery services present a notable opportunity in the electric commercial vehicle market. Last-mile delivery optimization is crucial for urban mobility solutions, and electric delivery vans and trucks offer a viable solution. According to the International Transport Forum (ITF), urban freight is expected to increase significantly, driven by e-commerce growth. Electric commercial vehicles, especially those designed for last-mile delivery, can capitalize on this trend by offering emission-free and noise-reduced transportation in urban areas. Municipalities and businesses can collaborate to create incentives for electric delivery fleets, such as congestion charge exemptions or preferential access to certain areas. This opportunity not only aligns with environmental goals but also addresses the increasing pressure to minimize congestion and pollution in urban centers, making electric commercial vehicles a strategic choice for companies involved in last-mile logistics and delivery operations.

Electric Commercial Vehicle Market Challenges

Limited Range and Battery Performance Variability

A substantial challenge in the electric commercial vehicle market is the limitation in range and the variability in battery performance, particularly for heavy-duty and long-haul applications. While advancements in battery technology have improved the energy density and range of electric vehicles, the operational range of electric commercial vehicles, such as trucks and buses, may still be a concern for certain applications. According to the U.S. Department of Energy, heavy-duty electric trucks often face challenges related to limited range compared to their diesel counterparts. Additionally, factors like temperature, terrain, and payload significantly impact the performance of electric vehicle batteries. Businesses relying on electric commercial vehicles for long-distance transportation may encounter challenges related to range anxiety and the need for frequent charging stops, potentially affecting operational efficiency. Addressing this challenge requires ongoing research and development to enhance battery technologies, increase energy density, and optimize the range for different types of electric commercial vehicles.

Recycling and End-of-Life Management of Batteries

Another significant challenge in the electric commercial vehicle market pertains to the recycling and end-of-life management of batteries. As electric vehicles become more widespread, the disposal and recycling of used batteries emerge as environmental concerns. According to the World Economic Forum, the growth in electric vehicles will result in a surge in battery waste, and by 2030, the world may face a considerable amount of retired batteries. Proper disposal and recycling of batteries are critical to avoid environmental pollution and utilize valuable materials efficiently. However, establishing comprehensive recycling infrastructure and sustainable practices for electric vehicle batteries is a complex challenge. The materials within batteries, such as lithium, cobalt, and nickel, are finite resources, and recycling them presents economic and technical challenges. Developing effective recycling methods and establishing a closed-loop system for battery materials are essential to mitigate the environmental impact of electric commercial vehicles and ensure the sustainability of the electric vehicle industry.

Regional Trends

North America

North America has seen a growing trend in the adoption of electric commercial vehicles, driven by environmental policies, government incentives, and a focus on sustainable transportation. The U.S. Department of Energy notes a surge in electric delivery vans and trucks, especially for last-mile logistics. Initiatives such as the “Buy Clean” policy and incentives like the federal electric vehicle tax credit contribute to the market’s growth. In addition, the transition to electric school buses is gaining traction, emphasizing the region’s commitment to cleaner and greener transportation solutions.

Europe

Europe has been at the forefront of electric commercial vehicle adoption, with a strong emphasis on sustainability and regulatory support. According to the European Alternative Fuels Observatory, European countries, particularly the Netherlands and Norway, have witnessed significant growth in electric van registrations. Urban delivery fleets are increasingly electrifying, supported by policies like the European Green Deal and financial incentives. The European Union’s strict emission standards and ambitious targets for reducing carbon emissions contribute to the accelerating trend of electric commercial vehicles on the continent.

Asia Pacific

The Asia Pacific region, including countries like China, Japan, and South Korea, has experienced a surge in electric commercial vehicle adoption. China, as a major market, has implemented policies to promote electric buses and delivery vehicles. The International Energy Agency (IEA) notes that China dominates the global electric bus market. In Japan, electric trucks are being developed for freight transport, aligning with the country’s focus on innovation in the automotive sector. The Asia-Pacific region’s commitment to reducing emissions and improving air quality contributes to the growth of electric commercial vehicles.

Middle East and Africa

In the Middle East and Africa, the adoption of electric commercial vehicles is influenced by the region’s economic development and a growing interest in sustainable practices. Countries like the United Arab Emirates have initiated projects to introduce electric buses, and there is an increasing awareness of the benefits of electric commercial vehicles in reducing air pollution. However, the pace of adoption may vary across countries due to economic factors and differing levels of infrastructure development.

Latin America

Latin America is witnessing a gradual shift toward electric commercial vehicles, driven by environmental concerns and governmental initiatives. Brazil, for example, has seen interest in electric buses for public transportation, and there is a growing awareness of the potential for electric delivery vehicles. The region’s market trends are influenced by a combination of regulatory support, awareness campaigns, and efforts to reduce dependence on traditional fuels.

Key Players

Key players operating in the global electric commercial vehicle market are Mercedes-Benz Group AG, BYD, AB Volvo, Paccar Inc, Tesla, Inc., Renault, Scania AB, Ford Motor Company, Yutong, Proterra, Dongfeng Motor Corporation, VDL Groep, Rivian, Tata Motors Limited, Nikola Corporation, Workhorse Group, Isuzu Motors Ltd., and Ashok Leyland.

PRICE

ASK FOR FREE SAMPLE REPORT