Global Co-Packaged Optics Market, By Type (Co-Packaged Optics (CPO), Near-Packaged Optics (NPO)), Data Rate (Less Than 1.6 T, 3.2 T, 6.4 T), Application (Data Center and High-Performance Computing, Telecommunications and Networking), and Region — Industry Analysis and Forecast to 2030

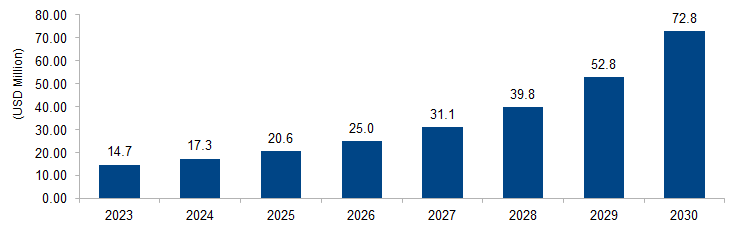

The global co-packaged optics market is expected to grow from USD 14.7 million in 2023 to USD 72.8 million by 2030 at a CAGR of 25.6%. The market is primarily driven by the growing demand for higher bandwidth and data rates in data centers. The need for improved power efficiency, reduced latency, and enhanced overall performance in optical communication systems has fueled the adoption of co-packaged opticssolutions, driving market expansion.

Figure 1: Global Co-Packaged Optics Market Size, 2023-2030 (USD Million)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Co-packaged optics refers to an advanced integration approach in optical communication technology where optical components like lasers, modulators, and photodetectors are closely integrated with semiconductor chips within a single package. This innovation minimizes signal losses, enhances data transfer efficiency, and reduces power consumption compared to traditional optical interconnect solutions. By co-locating optics and electronics, co-packaged optics addresses the increasing demand for higher bandwidth and performance in data centers. This technology facilitates faster and more reliable communication between electronic components, paving the way for improved scalability and energy efficiency in high-speed data transmission applications.

Co-Packaged Optics Market Drivers

Growing Data Center Traffic and Bandwidth Requirements

One key driver propelling the co-packaged optics market is the escalating demand for higher bandwidth and increased data traffic within data centers. With the proliferation of cloud computing, artificial intelligence, and other data-intensive applications, traditional optical interconnect solutions face limitations in addressing the surge in data transmission requirements. Co-packaged optics offers a solution by integrating optical components directly with semiconductor chips, reducing signal losses and improving data transfer efficiency. According to a report by the International Data Corporation (IDC), global data center IP traffic is expected to reach 20.6 zettabytes by 2023, emphasizing the urgency for advanced optical communication technologies like Co-Packaged Optics to support this exponential growth.

Need for Enhanced Power Efficiency and Reduced Latency

Another significant driver for the co-packaged optics market is the industry’s increasing focus on power efficiency and latency reduction in optical communication systems. Traditional disaggregated optical architectures suffer from energy inefficiencies and latency issues due to the separation of optical and electronic components. Co-packaged optics addresses this concern by co-locating these elements, resulting in improved power efficiency and reduced signal travel times. The Optical Internetworking Forum (OIF) emphasizes the importance of low-latency optical solutions, indicating that Co-Packaged Optics can play a pivotal role in meeting these objectives. This focus on energy-efficient and low-latency solutions is pivotal in catering to the evolving needs of modern applications and data center environments.

Co-Packaged Optics Market Restraints

Complex Design Challenges and Integration Issues

One significant restraint facing the co-packaged optics market revolves around the complex design challenges and integration issues associated with this advanced technology. Integrating optical components within the same package as semiconductor chips demands meticulous design precision and poses engineering challenges. Achieving optimal thermal management, ensuring signal integrity, and addressing potential interference are critical considerations. These complexities may result in increased development costs and elongated product development cycles. According to the Institute of Electrical and Electronics Engineers (IEEE), advancements in Co-Packaged Optics require breakthroughs in design methodologies to address these challenges effectively. The intricate nature of the integration process remains a substantial hurdle, hindering the widespread adoption of co-packaged opticsin the market.

High Initial Investment and Development Costs

Another notable restraint for the co-packaged optics market is the high initial investment and development costs associated with implementing this innovative technology. Research, development, and the establishment of production facilities for co-packaged optics entail substantial financial commitments. The Optical Internetworking Forum (OIF) highlights the need for significant capital investment in infrastructure, manufacturing processes, and research initiatives to bring Co-Packaged Optics solutions to market. This financial barrier can limit the adoption of Co-Packaged Optics, particularly for smaller companies or those with budget constraints. Until economies of scale are achieved, the high upfront costs may impede widespread industry adoption, slowing down the integration of co-packaged opticsinto mainstream optical communication systems despite its potential benefits.

Co-Packaged Optics Market Opportunities

Advancements in High-Performance Computing (HPC) and Artificial Intelligence (AI)

An exciting opportunity for the co-packaged optics market lies in the increasing demand for high-performance computing (HPC) and artificial intelligence (AI) applications. As these domains continue to evolve and demand faster processing speeds, the role of co-packaged opticsbecomes crucial. According to the Top500 project, the global HPC market is expanding, with more powerful supercomputers being deployed worldwide. Co-packaged optics, with its ability to provide high bandwidth and low latency, can significantly enhance the performance of HPC systems and accelerate AI algorithms. This aligns with the growing need for efficient data processing in scientific research, simulations, and AI-driven applications, creating a substantial market opportunity for co-packaged optics to cater to the evolving requirements of these technologies.

Emergence of 5G Networks

The deployment of 5G networks presents a significant opportunity for the co-packaged optics market. As 5G technology gains momentum globally, the demand for high-speed, low-latency communication systems increases. Co-packaged optics, with its ability to offer improved data transfer efficiency and reduced latency, aligns with the requirements of 5G infrastructure. According to the International Telecommunication Union (ITU), the number of 5G subscriptions is expected to reach 3.5 billion by 2026. Co-packaged optics can play a crucial role in supporting the data-intensive nature of 5G networks by providing advanced optical communication solutions. This opportunity positions Co-Packaged Optics as a key technology for the continued development and optimization of 5G networks, making it an integral component in the evolution of telecommunications infrastructure globally.

Co-Packaged Optics Market Challenges

Standardization and Interoperability Issues

One substantial challenge confronting the co-packaged optics market is the lack of standardized protocols and potential interoperability issues. The industry is still in the early stages of defining common standards for co-packaged optics, and the absence of universally accepted protocols may hinder seamless integration across different systems and vendors. Standardization is crucial to ensure that Co-Packaged Optics solutions from various manufacturers can work cohesively within a diverse ecosystem. The Optical Internetworking Forum (OIF) and other standardization bodies are actively working on addressing this challenge, but achieving consensus on protocols and interfaces remains an ongoing process. The absence of standardized guidelines may lead to compatibility issues, slowing down the widespread adoption of co-packaged opticsas a unified and interoperable solution in optical communication systems.

Supply Chain and Manufacturing Complexities

Another notable challenge in the co-packaged optics market involves supply chain and manufacturing complexities. The intricate integration of optical and electronic components within a single package requires specialized manufacturing processes and expertise. Scaling up production to meet the increasing demand for co-packaged optics can pose challenges related to the supply chain, quality control, and production yield. Ensuring the reliability and consistency of co-packaged opticsproducts at a larger scale demands sophisticated manufacturing capabilities. The Institute of Electrical and Electronics Engineers (IEEE) emphasizes the need for advancements in manufacturing technologies to overcome these challenges. The complexity of the manufacturing process, coupled with potential yield issues, may impact the cost-effectiveness and availability of co-packaged opticssolutions, posing a hurdle to broader market adoption until these challenges are effectively addressed.

Regional Trends

North America: North America, particularly the United States, has been a significant contributor to the co-packaged optics market due to the presence of key players in the semiconductor and networking industries. The region is witnessing increased investments in data centers and high-performance computing, which are driving the adoption of co-packaged optics solutions. Regulatory initiatives aimed at improving data infrastructure and network capabilities further support market growth.

Europe: Europe is also experiencing growth in the co-packaged optics market, propelled by the expansion of 5G networks and the increasing demand for data-intensive applications. Countries like Germany, the UK, and France are investing in upgrading their telecommunications infrastructure, creating opportunities for co-packaged optics vendors. Government initiatives focusing on digital transformation and connectivity enhancement are likely to drive market growth in the region.

Asia Pacific: Asia Pacific is expected to witness substantial growth in the co-packaged optics market due to the rapid expansion of telecommunications networks and the adoption of advanced technologies. Countries like China, Japan, and South Korea are investing heavily in 5G infrastructure, data centers, and cloud computing, driving demand for co-packaged optics solutions. Rising internet penetration rates and increasing demand for high-speed connectivity in emerging economies contribute to market expansion in the region.

Middle East and Africa: MEA region is also experiencing growth in the co-packaged optics market, driven by the deployment of 5G networks and the expansion of data center facilities. Countries in the Middle East, such as the UAE and Saudi Arabia, are investing in smart city initiatives and digital transformation projects, which require robust networking infrastructure. Africa, with its growing population and increasing internet penetration, presents opportunities for co-packaged optics vendors to cater to the rising demand for connectivity and data services.

Latin America: Latin America is witnessing growth in the co-packaged optics market, driven by investments in telecommunications infrastructure and the adoption of cloud services. Countries like Brazil, Mexico, and Argentina are upgrading their networks to support higher data speeds and accommodate the growing demand for digital services. Initiatives aimed at bridging the digital divide and improving connectivity in rural areas contribute to the expansion of the co-packaged optics market in the region.

Key Players

Key players operating in the global co-packaged optics market are Broadcom, Marvell, Ranovus, Quanta Computer Inc., Molex, Ragile Networks Inc., Senko, Furukawa Electric Co., Ltd., SABIC, TE Connectivity, Rain Tree Photonics Pteltd., Ruijie Networks Co., Ltd., and Synopsys, Inc.

PRICE

ASK FOR FREE SAMPLE REPORT