Global Autonomous Forklift Market, By Navigation Technology (Laser Guidance, Magnetic Guidance, Optical Tape Guidance, Inductive Guidance, Simultaneous Localization and Mapping (SLAM), Vision Guidance), Application (Manufacturing, Warehousing, Material Handling, Logistics and Freight), Tonnage Capacity (Below 5 Tons, 5-10 Tons, Above 10 Tons), End-Use Industry (Third-Party Logistics (3PL), Automotive, Food and Beverages, Paper and Pulp, Metals and Heavy Machinery, Ecommerce, Semiconductors and Electronics, Aviation, Chemicals, Healthcare), Fuel Source (Electric, Internal Combustion Engine (ICE), Alternate Fuels), Type (Indoor, Outdoor), Forklift Type (Pallet Jacks, Pallet Stackers), and Region — Industry Analysis and Forecast to 2030

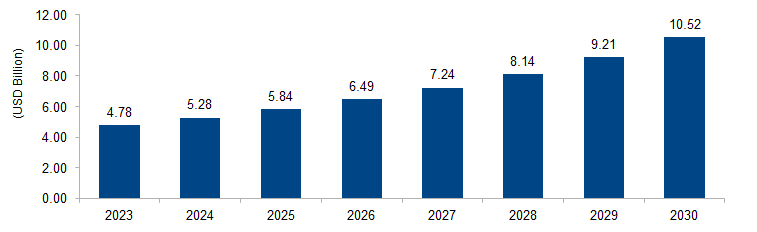

The global autonomous forklift market is expected to grow from USD 4.78 billion in 2023 to USD 10.52 billion by 2030 at a CAGR of 11.9%. The market is driven by the increasing need for warehouse optimization and efficiency. Industries seek to enhance logistics and material handling processes, spurring demand for autonomous forklifts. These vehicles offer benefits such as increased productivity, reduced operational costs, and improved safety, fostering the adoption of automation in warehouse and distribution center operations.

Figure 1: Global Autonomous Forklift Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

An autonomous forklift refers to a self-driving and self-operating material handling vehicle designed for lifting, transporting, and stacking pallets or goods within a warehouse or industrial setting. These forklifts utilize advanced technologies such as sensors, cameras, lidar, and artificial intelligence to navigate and interact with their environment autonomously. They can execute tasks like loading and unloading, inventory management, and maneuvering through predefined routes without direct human intervention. Autonomous forklifts contribute to improved efficiency, safety, and productivity in logistics and manufacturing operations by reducing the need for manual labor and optimizing the material handling processes within a facility.

Autonomous Forklift Market Drivers

Growing Emphasis on Warehouse Automation

A key driver for the autonomous forklift market is the increasing emphasis on warehouse automation within the logistics and manufacturing sectors. The need for enhanced efficiency, accuracy, and speed in material handling processes has led to a surge in the adoption of autonomous solutions. According to the International Federation of Robotics (IFR), the global sales of industrial robots, including those used in material handling applications, witnessed significant growth. Autonomous forklifts play a pivotal role in warehouse optimization, offering capabilities such as automated pallet handling, inventory management, and seamless navigation. As e-commerce and supply chain demands continue to rise, companies are investing in autonomous forklifts to streamline operations, reduce labor costs, and minimize errors in inventory management, contributing to the overall growth of the autonomous forklift market.

Increasing Focus on Workplace Safety and Efficiency

The emphasis on workplace safety and the pursuit of operational efficiency are driving factors for the adoption of autonomous forklifts. According to the Occupational Safety and Health Administration (OSHA), the material handling industry experiences a significant number of workplace injuries, with forklift-related accidents being a notable concern. Autonomous forklifts address this challenge by reducing the need for human operators, minimizing the risk of accidents caused by factors like operator fatigue or errors. Additionally, autonomous forklifts are designed to operate seamlessly in environments with a high density of goods, optimizing storage space and minimizing congestion. The focus on creating safer work environments, coupled with the desire to improve overall operational efficiency, is propelling the integration of autonomous forklifts into various industries, fostering a positive market outlook for these automated material handling solutions.

Autonomous Forklift Market Restraints

High Initial Implementation Costs

A significant restraint in the autonomous forklift market is the high initial implementation costs associated with adopting autonomous material handling solutions. The installation of the required technology infrastructure, including sensors, cameras, and navigation systems, demands substantial upfront investment. According to the Material Handling Equipment Distributors Association (MHEDA), the initial cost of autonomous forklift systems can be a barrier for small and medium-sized enterprises (SMEs). The need for retrofitting existing forklift fleets or investing in new autonomous forklifts can pose financial challenges. While the long-term benefits in terms of increased efficiency and reduced labor costs are recognized, the initial capital outlay remains a significant consideration for businesses contemplating the adoption of autonomous forklifts, impacting the pace of market penetration.

Complex Integration with Existing Systems

The complex integration of autonomous forklifts with existing warehouse management and enterprise systems represents another restraint. Achieving seamless coordination between autonomous forklifts and other automated or manual material handling equipment can be intricate. According to the International Journal of Advanced Robotic Systems, interoperability challenges may arise when integrating autonomous forklifts with warehouse management software or enterprise resource planning systems. Ensuring a smooth transition without disruptions to ongoing operations requires careful planning and investment in compatible technologies. For businesses with legacy systems or diverse equipment, the integration process may entail additional customization and complexity. The challenge of harmonizing autonomous forklifts with existing infrastructures can pose a hindrance to widespread adoption, especially for enterprises with established warehouse setups seeking to incorporate automation into their material handling processes.

Autonomous Forklift Market Opportunities

Integration of AI and Machine Learning for Enhanced Decision-Making

An opportunity in the autonomous forklift market lies in the integration of artificial intelligence (AI) and machine learning (ML) technologies to enhance decision-making capabilities. The use of AI algorithms enables autonomous forklifts to adapt to dynamic warehouse environments, optimizing route planning, load prioritization, and navigation. According to the International Federation of Robotics (IFR), advancements in AI and ML contribute to the sophistication of robotic systems in material handling applications. Autonomous forklifts equipped with learning algorithms can continuously improve their performance based on data analysis, leading to increased efficiency and reduced operational errors. This opportunity positions the market to explore and implement intelligent, self-optimizing forklifts that can seamlessly adapt to evolving warehouse conditions, thereby catering to the demand for flexible and responsive automated material handling solutions.

Expansion of Autonomous Forklifts in E-Commerce Fulfillment Centers

A significant opportunity for the autonomous forklift market is the expanding role of these automated solutions in e-commerce fulfillment centers. The burgeoning growth of the e-commerce sector, accelerated by changing consumer preferences and online shopping trends, presents a substantial market avenue. The United Nations Conference on Trade and Development (UNCTAD) reports a substantial increase in global e-commerce sales. Autonomous forklifts offer a valuable solution for the efficient handling of inventory and order fulfillment in large-scale e-commerce warehouses. As fulfillment centers strive to meet the demands for faster order processing and delivery, autonomous forklifts become pivotal in streamlining logistics operations. This opportunity positions the market to cater to the specific needs of e-commerce players, providing advanced material handling solutions that contribute to the speed and accuracy of order fulfillment processes in the dynamic and rapidly growing e-commerce landscape.

Autonomous Forklift Market Challenges

Limited Adaptation to Unstructured Environments

A prominent challenge in the autonomous forklift market is the limited adaptation of these vehicles to unstructured or dynamic environments. While autonomous forklifts excel in controlled and structured warehouse settings, they face challenges in environments where the layout is subject to frequent changes, or where unexpected obstacles and variations occur. According to research by the International Journal of Advanced Manufacturing Technology, unstructured environments may include outdoor settings, construction sites, or warehouses with irregular layouts. Autonomous forklifts may struggle to navigate efficiently in such scenarios, leading to potential disruptions and decreased productivity. Addressing this challenge requires advancements in sensor technologies and navigation algorithms that can handle real-time adjustments to diverse and unpredictable working environments, expanding the application of autonomous forklifts beyond traditional warehouses.

Regulatory and Safety Compliance

Regulatory and safety compliance pose significant challenges to the widespread adoption of autonomous forklifts. Government agencies and industry standards organizations, such as the Occupational Safety and Health Administration (OSHA), impose stringent regulations on the operation of industrial vehicles. Ensuring that autonomous forklifts comply with safety standards, both in terms of design and operational aspects, is critical. According to the Industrial Truck Association (ITA), ensuring the safety of autonomous forklifts involves addressing issues related to collision avoidance, emergency braking, and human-machine interaction. Meeting these safety standards becomes more complex as autonomous forklifts share spaces with human-operated equipment. The challenge is not only to design autonomous forklifts that can navigate safely but also to develop and adhere to regulatory frameworks that govern their deployment, addressing concerns related to liability, accident prevention, and overall workplace safety. Overcoming these regulatory and safety challenges is crucial for gaining broader acceptance and trust in the use of autonomous forklifts across various industries.

Regional Trends

North America

In North America, the autonomous forklift market has seen a trend toward increased adoption, particularly in response to the growing demand for warehouse automation and e-commerce fulfillment. The region has witnessed advancements in robotics and automation technologies. The Occupational Safety and Health Administration (OSHA) and industry standards organizations have influenced the adoption of autonomous forklifts by emphasizing safety regulations. The market has also been characterized by collaborations between manufacturers, technology providers, and e-commerce companies to implement automated solutions. As e-commerce continues to grow, North America is likely to experience further trends in the integration of autonomous forklifts to enhance logistics and material handling efficiency.

Europe

In Europe, the adoption of autonomous forklifts aligns with the region’s focus on sustainability, efficiency, and Industry 4.0 initiatives. European countries, such as Germany and the Netherlands, have been at the forefront of implementing smart manufacturing and logistics solutions. The European Union’s emphasis on environmental sustainability and innovation has influenced the integration of autonomous technologies. Warehouse optimization and green logistics have been driving forces, and the market has witnessed trends in the use of electric and hybrid autonomous forklifts. Collaborations between logistics companies, manufacturers, and technology providers have contributed to the deployment of these technologies in Europe.

Asia Pacific

The Asia Pacific region, particularly countries like China, Japan, and South Korea, has seen a surge in the adoption of autonomous forklifts. The growth of manufacturing and e-commerce industries, coupled with government initiatives supporting automation, has fueled the demand for these technologies. In China, for example, the “Made in China 2025” initiative has encouraged the implementation of smart manufacturing solutions, including autonomous forklifts. The region has also experienced trends in the development of artificial intelligence (AI) and machine learning technologies to enhance the capabilities of autonomous forklifts, making them more adaptable to dynamic environments.

Middle East and Africa

In the Middle East and Africa, the adoption of autonomous forklifts has been influenced by the region’s investment in infrastructure development and logistics. Countries such as the United Arab Emirates have been incorporating automation into their supply chains. The demand for efficient material handling solutions in industries such as oil and gas, construction, and retail has contributed to trends in deploying autonomous forklifts. However, the pace of adoption may vary across different countries in the region based on economic factors and industry-specific requirements.

Latin America

In Latin America, trends in the adoption of autonomous forklifts have been shaped by the region’s focus on improving logistics and supply chain efficiency. The growth of the e-commerce sector in countries like Brazil and Mexico has driven the demand for automated material handling solutions. Government initiatives aimed at enhancing manufacturing capabilities and logistics infrastructure have also played a role. The market has witnessed trends in the integration of connectivity and IoT technologies to optimize the performance of autonomous forklifts in the region.

Key Players

Key players operating in the global autonomous forklift market are Toyota Industries Corporation, Mitsubishi Logisnext Co., Ltd., Kion Group AG, Jungheinrich AG, Hyster-Yale Materials Handling, Inc., Agilox Services GmbH, Swisslog AG, Hyundai Construction Equipment Co., Ltd., Oceaneering International, Inc., Balyo SA, Anhui Heli Co., Ltd., AGVE AB, Movigo Robotics Bv, Otto Motors, Seegrid Corporation, Vecna Robotics, Multiway Robotics (Shenzhen) Co., Ltd., and È GROUP S.P.A.

PRICE

ASK FOR FREE SAMPLE REPORT