Global Automotive Cybersecurity Market, By Application Type (Telematics, Communication Systems, ADAS & Safety, Infotainment, Body Control & Comfort, Powertrain Systems), Form Type (In-Vehicle, External Cloud Services), Offering (Hardware, Software), Security Type (Application Security, Wireless Network Security, Endpoint Security), Vehicle Autonomy (Non-Autonomous Vehicles, Semi-Autonomous Vehicles, Autonomous Vehicles), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles), Propulsion Type (ICE Vehicles, Electric Vehicles), and Region — Industry Analysis and Forecast to 2030

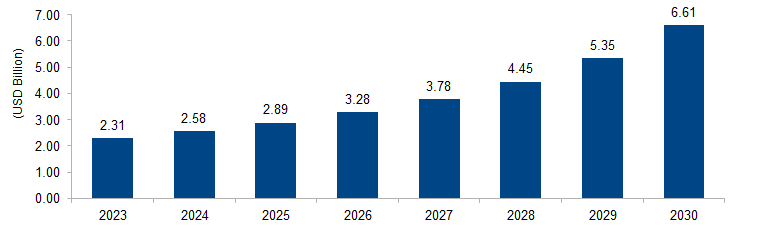

The global automotive cybersecurity market is expected to grow from USD 2.31 billion in 2023 to USD 6.61 billion by 2030 at a CAGR of 16.2%. The market is driven by the increasing connectivity and complexity of modern vehicles, making them vulnerable to cyber threats. The growing adoption of connected car technologies and autonomous vehicles amplifies the need for robust cybersecurity solutions to safeguard against potential cyberattacks, ensuring the safety and security of automotive systems and data.

Figure 1: Global Automotive Cybersecurity Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Automotive cybersecurity refers to the protection of connected vehicles and their electronic systems from cyber threats and unauthorized access. With the increasing integration of advanced technologies like internet connectivity, autonomous driving, and in-car communication systems, vehicles are exposed to potential cyberattacks. Automotive cybersecurity involves implementing robust measures, such as firewalls, encryption, and intrusion detection systems, to safeguard vehicle software, control systems, and data from malicious activities. Ensuring the security of automotive systems is crucial to prevent unauthorized manipulation, hacking, or disruption that could compromise vehicle safety, privacy, and overall functionality in the rapidly evolving landscape of connected and autonomous vehicles.

Automotive Cybersecurity Market Drivers

Increasing Connectivity and Digitization in Vehicles

A significant driver for the automotive cybersecurity market is the escalating integration of connectivity and digital technologies in modern vehicles. The advent of connected cars, telematics systems, and in-vehicle infotainment has substantially increased the attack surface for potential cyber threats. According to the International Telecommunication Union (ITU), the number of connected cars is expected to rise significantly in the coming years. This surge in connectivity enhances the driving experience but also exposes vehicles to cybersecurity risks. As more vehicles become part of the Internet of Things (IoT), the need for robust cybersecurity solutions intensifies. The automotive industry is witnessing a paradigm shift towards smart, connected vehicles, prompting automakers and cybersecurity providers to collaborate and implement advanced security measures to protect against potential cyberattacks, ensuring the integrity and safety of vehicle systems.

Rise of Autonomous Vehicles and Advanced Driver Assistance Systems (ADAS)

The proliferation of autonomous vehicles and the widespread adoption of Advanced Driver Assistance Systems (ADAS) serve as key drivers for the automotive cybersecurity market. The interconnectedness and reliance on sophisticated software in autonomous and ADAS-equipped vehicles create new cybersecurity challenges. As per the Society of Automotive Engineers (SAE), levels of vehicle automation are expected to increase, necessitating comprehensive cybersecurity strategies. Autonomous vehicles, with their complex sensor systems and communication networks, are vulnerable to cyber threats that could compromise safety and navigation. Governments and industry organizations are recognizing the importance of addressing these challenges. Collaborative initiatives are underway to establish cybersecurity standards for autonomous vehicles, ensuring that cybersecurity is an integral part of the development and deployment of these advanced automotive technologies. The rise of autonomous driving underscores the critical role of cybersecurity in shaping the future of safe and secure transportation systems.

Automotive Cybersecurity Market Restraints

Lack of Standardization and Regulations

A significant restraint in the automotive cybersecurity market is the absence of standardized regulations and frameworks across the industry. The lack of uniformity in cybersecurity standards makes it challenging for automakers and cybersecurity solution providers to implement consistent and interoperable security measures. According to the National Highway Traffic Safety Administration (NHTSA) in the US, the regulatory landscape for automotive cybersecurity is evolving, but there is a notable lack of specific, standardized requirements. This absence hinders a cohesive approach to cybersecurity, leading to varied practices among manufacturers. The industry requires standardized guidelines to ensure a comprehensive and unified response to cybersecurity threats. The absence of clear regulations also complicates international cooperation, hindering global efforts to address cybersecurity challenges uniformly across different regions.

Complexity of Automotive Systems and Interconnected Ecosystems

The intricate and interconnected nature of modern automotive systems presents a restraint to effective cybersecurity implementation. As vehicles become more sophisticated with advanced features like autonomous driving, connected services, and over-the-air updates, the attack surface for potential cyber threats expands significantly. According to the International Organization of Motor Vehicle Manufacturers (OICA), the complexity of in-vehicle software and the growing number of electronic control units (ECUs) make vehicles more susceptible to cyber vulnerabilities. Ensuring the cybersecurity of interconnected ecosystems, including vehicle-to-everything (V2X) communication, introduces challenges related to identifying and mitigating potential entry points for cyberattacks. The intricate web of components and communication networks requires robust cybersecurity solutions, but the complexity of modern automotive systems poses a hurdle in implementing standardized and foolproof security measures across the entire automotive ecosystem. Addressing this challenge necessitates collaborative efforts to establish comprehensive cybersecurity standards that encompass the diverse components and communication interfaces within vehicles.

Automotive Cybersecurity Market Opportunities

Emerging Markets for Connected and Electric Vehicles

One significant opportunity in the automotive cybersecurity market stems from the rapid growth of emerging markets, particularly in the adoption of connected and electric vehicles (EVs). Governments worldwide are incentivizing the transition to cleaner and technologically advanced vehicles. For instance, the European Union has set ambitious targets for reducing vehicle emissions, driving the adoption of electric and connected vehicles. As these markets expand, there is a parallel need for robust cybersecurity solutions tailored to the specific challenges of connected and electric vehicles. Cybersecurity becomes integral to the successful deployment of EV charging infrastructure, vehicle-to-grid (V2G) communication, and other connected services. The opportunity lies in providing comprehensive cybersecurity frameworks that address the unique vulnerabilities associated with the electrification and connectivity of vehicles in emerging markets, contributing to the sustainable and secure growth of the automotive industry.

Collaboration and Partnerships in the Automotive Ecosystem

The automotive cybersecurity market presents a notable opportunity through increased collaboration and partnerships within the automotive ecosystem. As vehicles become more interconnected and reliant on external networks and services, collaboration between automakers, technology providers, and cybersecurity firms becomes crucial. Government agencies and industry associations are actively promoting such collaborations. For instance, the U.S. Department of Transportation emphasizes industry cooperation to enhance automotive cybersecurity. Opportunities arise for cybersecurity solution providers to form partnerships with original equipment manufacturers (OEMs) and technology suppliers to integrate cybersecurity measures seamlessly into the automotive development process. Joint initiatives can focus on information sharing, developing standardized practices, and establishing common frameworks to address cybersecurity challenges effectively. By fostering collaborative efforts, the automotive cybersecurity market can leverage shared expertise, resources, and insights to stay ahead of evolving cyber threats and create a more resilient and secure automotive ecosystem.

Automotive Cybersecurity Market Challenges

Supply Chain Vulnerabilities

A significant challenge in the automotive cybersecurity market is the increasing complexity and global nature of automotive supply chains, which introduces vulnerabilities. According to the International Organization of Motor Vehicle Manufacturers (OICA), the automotive industry relies on a vast network of suppliers, making it challenging to ensure the cybersecurity of every component in the supply chain. Cyber threats may exploit weaknesses in the production and distribution process, potentially compromising the integrity of critical components. Each supplier introduces its own set of cybersecurity risks, and the lack of standardized security practices across the supply chain can lead to vulnerabilities. Addressing this challenge requires collaborative efforts to establish cybersecurity standards and guidelines for suppliers. Additionally, manufacturers need to implement robust cybersecurity measures and conduct thorough assessments throughout the supply chain to minimize the risk of cyber threats affecting the security and functionality of automotive systems.

Evolving Threat Landscape and Advanced Persistent Threats (APTs)

The automotive cybersecurity market faces a continuous challenge posed by the evolving nature of cyber threats and the emergence of advanced persistent threats (APTs). APTs are sophisticated and stealthy cyberattacks that specifically target automotive systems for extended periods, aiming to compromise sensitive data or disrupt critical functions. The dynamic threat landscape requires constant adaptation and innovation in cybersecurity measures. As vehicles become more connected and autonomous, the potential impact of cyber threats increases significantly. According to the National Institute of Standards and Technology (NIST), the automotive industry needs to stay vigilant against evolving cyber threats and be prepared for new attack vectors. The challenge lies in developing proactive cybersecurity strategies that go beyond conventional measures, incorporating advanced threat detection and response capabilities. Automotive cybersecurity solutions must continually evolve to counter increasingly sophisticated cyber threats, requiring ongoing research, development, and collaboration across the industry to stay ahead of the rapidly changing threat landscape.

Regional Trends

North America

In North America, particularly in the US, there is an increasing focus on automotive cybersecurity driven by the growing number of connected vehicles and the emphasis on autonomous driving technologies. Government agencies, including the National Highway Traffic Safety Administration (NHTSA), are likely to continue pushing for cybersecurity regulations and standards. The U.S. automotive industry is also witnessing collaborations between automakers and cybersecurity firms to enhance the security of connected vehicles. As electric vehicles (EVs) gain popularity, the integration of robust cybersecurity measures in EVs is expected to be a prominent trend.

Europe

Europe is at the forefront of automotive cybersecurity initiatives, with a strong emphasis on regulatory frameworks. The European Union has been actively working on establishing cybersecurity standards for connected and autonomous vehicles. Euro NCAP, the European New Car Assessment Programme, incorporates cybersecurity considerations into its safety assessments. The European automotive industry is likely to witness a trend toward increased collaboration between automotive manufacturers, cybersecurity solution providers, and government agencies to address cybersecurity challenges systematically.

Asia Pacific

In the Asia Pacific region, especially in countries like Japan and South Korea, the automotive industry is witnessing a surge in the adoption of connected and electric vehicles. The increased connectivity in vehicles poses cybersecurity challenges, and there is an opportunity for the development and implementation of advanced cybersecurity solutions. As Asia Pacific is a significant player in the global automotive market, regional governments and industry players are expected to focus on cybersecurity initiatives to ensure the safety and security of vehicles on the road.

Middle East and Africa

While the Middle East and Africa may not be as advanced in terms of automotive cybersecurity compared to other regions, the increasing adoption of connected technologies and electric vehicles in some countries could drive awareness and initiatives in this space. The focus on smart city projects in certain Middle Eastern countries may contribute to the integration of cybersecurity measures in automotive systems.

Latin America

In Latin America, the automotive industry is evolving, with an increasing number of vehicles incorporating connected features. As the region embraces technological advancements, there may be a growing awareness of the need for automotive cybersecurity. Governments and industry stakeholders could collaborate to establish guidelines and standards to address cybersecurity challenges and ensure the secure deployment of connected and autonomous vehicles.

Key Players

Key players operating in the global automotive cybersecurity market are Robert Bosch GmbH, Continental AG, Harman International, Denso Corporation, Aptiv PLC, Garrett Motion Inc., Renesas Electronics Corporation, NXP Semiconductors, Lear Corporation, Vector Informatik GmbH, Karamba Security, Sheelds, SafeRide Technologies, GuardKnox Cyber Technologies Ltd., Upstream Security Ltd., Broadcom Inc., Airbiquity Inc., and Green Hills Software.

PRICE

ASK FOR FREE SAMPLE REPORT