Global Automotive Camera Market, By Technology (Digital, Infrared, Thermal), ICE Application (Adaptive Cruise Control (ACC), Forward Collision Warning (FCW), Traffic Sign Recognition (TSR), Blind Spot Detection (BSD), Intelligent Park Assist (IPA), Adaptive Lighting Systems (ALS), Driver Monitoring Systems (DMS), Night Vision Systems (NVS)), View Type (Front View, Rear View, Surround View), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), Level of Autonomy (L1, L2 & L3, L4 & L5), and Region — Industry Analysis and Forecast to 2030

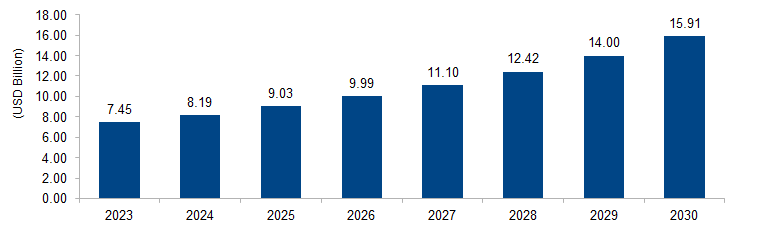

The global automotive camera market is expected to grow from USD 7.45 billion in 2023 to USD 15.91 billion by 2030 at a CAGR of 11.5%. The market is propelled by the growing emphasis on safety and advanced driver-assistance systems (ADAS). Increasing regulatory mandates for vehicle safety features, coupled with a rising awareness of the benefits of cameras in collision prevention and parking assistance, drive the demand for automotive cameras. Manufacturers respond by integrating innovative camera technologies into vehicles to enhance overall safety and improve the driving experience.

Figure 1: Global Automotive Camera Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

An automotive camera refers to a specialized imaging device installed in vehicles to capture visual information for various purposes. These cameras play a pivotal role in modern automotive systems, particularly in advanced driver-assistance systems (ADAS). They are strategically placed around the vehicle to provide real-time visual data for functions such as lane departure warning, collision avoidance, parking assistance, and pedestrian detection. Automotive cameras enhance overall safety by assisting drivers in making informed decisions and by facilitating the integration of autonomous driving technologies. The continual advancement of camera technologies contributes to the evolution of smarter and more efficient vehicles on the road.

Automotive Camera Market Drivers

Regulatory Mandates for Vehicle Safety

A key driver for the automotive camera market is the increasing stringency of regulatory mandates globally, compelling automakers to integrate advanced safety features into vehicles. Governments and safety organizations are emphasizing the importance of enhancing road safety through technologies like advanced driver-assistance systems (ADAS), wherein automotive cameras play a crucial role. For instance, the National Highway Traffic Safety Administration (NHTSA) in the US has been progressively introducing regulations to encourage the adoption of safety technologies. The European New Car Assessment Programme (Euro NCAP) also includes assessment criteria for ADAS features, influencing manufacturers to incorporate camera-based systems. As these regulations evolve and expand, the automotive camera market experiences growth, driven by the necessity for compliance and the prioritization of safety in the automotive industry.

Increasing Consumer Demand for Advanced Driver-Assistance Systems

Consumer demand for enhanced safety features and a more comfortable driving experience acts as a significant driver for the automotive camera market. As awareness of advanced driver-assistance systems grows, consumers actively seek vehicles equipped with technologies like lane-keeping assistance, automatic emergency braking, and adaptive cruise control—all of which rely on camera inputs. The desire for improved vehicle safety, reduced accidents, and overall driving convenience fuels the integration of sophisticated camera systems. Industry reports indicate a rising trend in consumer preference for vehicles equipped with ADAS features. As per a survey by the Insurance Institute for Highway Safety (IIHS), a considerable number of drivers express interest in purchasing vehicles with ADAS, indicating a strong market pull towards camera-based safety technologies. This consumer-driven demand propels innovation and investment in the automotive camera market.

Automotive Camera Market Restraints

Cost and Affordability Challenges

A significant restraint for the automotive camera market is the cost associated with implementing advanced camera systems in vehicles. While demand for safety features and ADAS is high, the added expense of integrating high-quality cameras can increase the overall cost of manufacturing vehicles. This cost burden is particularly pronounced for smaller or budget-conscious consumers. The European Automobile Manufacturers’ Association (ACEA) notes that cost considerations are critical in the widespread adoption of safety technologies, with economic factors influencing the pace of implementation. As a result, manufacturers face the challenge of striking a balance between incorporating advanced camera technologies and keeping vehicles affordable for a broader consumer base. The cost factor acts as a limiting factor, affecting the market penetration of automotive cameras, especially in entry-level and mid-range vehicle segments.

Data Security and Privacy Concerns

The increasing reliance on automotive cameras for data collection and processing raises significant concerns related to data security and privacy. As cameras become more sophisticated and integrated with connected car systems, the amount of sensitive data they capture, including driver behavior and surrounding environments, grows substantially. The General Data Protection Regulation (GDPR) in Europe and similar regulations worldwide highlight the need to address data privacy concerns in the automotive sector. The potential misuse of this data, whether through unauthorized access or hacking, poses a substantial risk. Addressing these concerns requires robust cybersecurity measures and adherence to privacy regulations, adding complexity and cost to the development and implementation of automotive camera systems. Striking a balance between leveraging the benefits of data for improved safety and addressing privacy concerns remains a critical challenge for the automotive camera market.

Automotive Camera Market Opportunities

Autonomous Vehicles and Advanced Driver Assistance Systems (ADAS) Evolution

An opportunity for the automotive camera market lies in the ongoing evolution of autonomous vehicles and the continued advancement of ADAS technologies. As the automotive industry moves towards higher levels of automation, the demand for sophisticated camera systems to enable perception and decision-making in real-time grows substantially. Cameras are integral to functions such as object detection, lane-keeping, and pedestrian recognition—essential components for autonomous driving. According to the International Organization of Motor Vehicle Manufacturers (OICA), the production of electric and electronic vehicles, including those equipped with advanced camera systems, has been steadily increasing globally. The rising investment in research and development for autonomous technologies presents a promising avenue for the automotive camera market to further integrate advanced vision systems, contributing to the realization of safer and more autonomous driving experiences.

Integration with Augmented Reality (AR) and Artificial Intelligence (AI)

The integration of automotive cameras with augmented reality (AR) and artificial intelligence (AI) technologies presents a compelling opportunity. Advanced camera systems, when combined with AR overlays and AI algorithms, can enhance the driver’s situational awareness, providing real-time information and assistance. For example, AR displays can offer navigation prompts directly on the windshield, reducing the need for the driver to look away from the road. The market potential is reflected in the increasing interest in AR-enhanced automotive displays. According to the Consumer Technology Association (CTA), the market for automotive technology, including AR displays, is expected to witness significant growth. Leveraging this opportunity requires collaborations between camera manufacturers, AI developers, and automotive companies to create seamless and intuitive interfaces that improve the overall driving experience. The convergence of automotive cameras with AR and AI technologies opens up avenues for innovation, making vehicles more intelligent and user-friendly.

Automotive Camera Market Challenges

Environmental Conditions and Reliability Challenges

One of the challenges facing the automotive camera market is ensuring reliability and performance under various environmental conditions. Automotive cameras are subjected to a wide range of environmental factors, including extreme temperatures, humidity, dust, and vibrations, which can affect their functionality and longevity. According to the Society of Automotive Engineers (SAE), automotive cameras must meet stringent standards for durability and reliability to ensure consistent performance in harsh conditions. Ensuring the reliability of automotive cameras in adverse environments requires robust design and testing processes by manufacturers. Additionally, the need for regular maintenance and cleaning to prevent dust and debris buildup poses logistical challenges for vehicle owners. Addressing these challenges involves continuous research and development to enhance the durability and resilience of automotive camera systems, ensuring they meet the demands of diverse operating environments while maintaining optimal performance.

Compatibility and Standardization Issues

Another challenge for the automotive camera market is the lack of universal compatibility and standardization across different vehicle models and manufacturers. With the increasing adoption of advanced driver assistance systems (ADAS) and camera-based safety features, there is a growing need for interoperability and seamless integration of automotive cameras with other vehicle components and systems. However, the absence of standardized interfaces and protocols complicates the integration process, leading to compatibility issues between camera systems and vehicle platforms. The International Organization for Standardization (ISO) and other standard-setting bodies are working to establish common standards for automotive camera systems. However, achieving widespread adoption and compatibility across the automotive industry remains a significant challenge. Manufacturers and suppliers must collaborate to develop standardized interfaces and protocols, ensuring compatibility between automotive camera systems and vehicles from different manufacturers. Overcoming these compatibility and standardization challenges is essential to facilitate the seamless integration and interoperability of automotive camera systems, ultimately enhancing vehicle safety and performance.

Regional Trends

North America

In North America, particularly in the US, the automotive camera market has been witnessing significant growth, driven by the increasing adoption of advanced driver-assistance systems (ADAS) and safety regulations. The U.S. National Highway Traffic Safety Administration (NHTSA) has been actively encouraging the integration of safety technologies, influencing the automotive industry to incorporate cameras in vehicles. The trend includes the rise of rear-view cameras becoming standard features in new vehicles, as mandated by regulations. Additionally, the North American market has shown a growing interest in high-resolution cameras for enhanced image quality and improved object detection capabilities, contributing to the overall advancement of automotive camera technologies.

Europe

In Europe, automotive safety regulations and consumer demand for advanced safety features have been driving the adoption of automotive cameras. The European New Car Assessment Programme (Euro NCAP) includes criteria for assessing ADAS, influencing manufacturers to integrate cameras for functionalities like lane-keeping assistance and automatic emergency braking. The European market has been experiencing a trend towards increased use of surround-view cameras and the integration of cameras in side mirrors for improved visibility. Additionally, there is a growing emphasis on the development of electric vehicles (EVs) and autonomous driving technologies in Europe, which further contributes to the demand for advanced camera systems in vehicles.

Asia Pacific

The Asia Pacific region has been a key player in the automotive camera market, with countries like Japan, China, and South Korea contributing significantly. The market has been influenced by the rapid expansion of the automotive industry in these countries, coupled with increasing consumer awareness of vehicle safety. China, as the largest automotive market, has been witnessing a surge in the adoption of ADAS and camera-based safety features. The Asia Pacific region is also at the forefront of electric vehicle (EV) adoption, and the integration of cameras in EVs for purposes like autonomous driving and parking assistance is a notable trend.

Middle East and Africa

The Middle East and Africa region have been experiencing a gradual adoption of automotive camera technologies, driven by a combination of safety regulations and consumer preferences. While safety features are becoming more common, the market in this region is also influenced by factors like off-road vehicle usage in certain areas. There is a potential for growth in advanced camera applications for off-road and utility vehicles.

Latin America

Latin America has been witnessing an increasing focus on safety technologies, contributing to the adoption of automotive cameras in the market. Economic factors influence the pace of adoption, but there is a growing awareness of the benefits of ADAS, particularly in urban environments. The market in Latin America is characterized by a mix of safety-driven trends and economic considerations impacting the penetration of advanced camera systems in vehicles.

Key Players

Key players operating in the global automotive camera market are Continental AG, Robert Bosch, ZF Friedrichshafen AG, Valeo, Denso, Aptiv, Veoneer, Magna International, Inc., Ficosa, Mobileye, Faurecia, Samvardhana Motherson, Automated Engineering Inc (AEI), Omnivision, Hitachi Astemo, Ltd., Ambarella, Gentex Corporation, and Kyocera Corporation.

PRICE

ASK FOR FREE SAMPLE REPORT