Global Animal Parasiticides Market, By Type (Ectoparasiticides, Endoparasiticides, Endectocides), Animal Type (Companion Animals, Livestock), End User (Veterinary Hospitals and Clinics, Animal Farms, Home Care Settings), and Region — Industry Analysis and Forecast to 2030

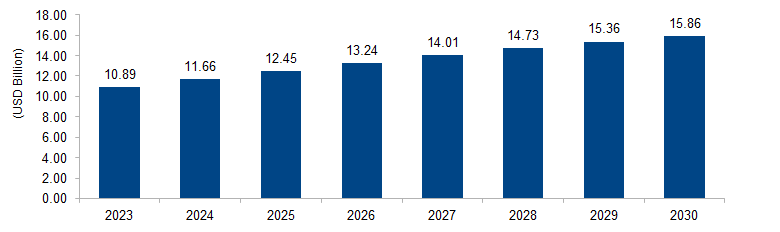

The global animal parasiticides market is expected to grow from USD 10.89 billion in 2023 to USD 15.86 billion by 2030 at a CAGR of 5.5%. The market is primarily driven by the rising awareness of zoonotic diseases and the need for preventive measures in livestock. Increasing pet ownership and a growing emphasis on animal health contribute to the market’s growth. Technological advancements in parasiticide formulations and a surge in global meat consumption further propel market expansion.

Figure 1: Global Animal Parasiticides Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Animal parasiticides are substances or medications used to control and eliminate parasitic infections in animals. These parasites, including fleas, ticks, worms, and mites, can pose significant health threats to livestock, pets, and even humans through zoonotic diseases. Animal parasiticides come in various forms such as topical solutions, oral medications, and injections, offering a range of options for treatment and prevention. As an essential component of veterinary care, these products help maintain animal health, improve livestock productivity, and safeguard human health by reducing the risk of parasitic infections transmitted from animals to humans.

Animal Parasiticides Market Drivers

Growing Awareness of Zoonotic Diseases

One significant driver of the animal parasiticides market is the escalating awareness of zoonotic diseases and the critical role these parasiticides play in preventing their transmission. Zoonotic diseases are infections that can be transmitted from animals to humans, making the control of parasites in animals crucial for public health. According to the World Health Organization (WHO), around 60% of known infectious diseases in humans are zoonotic, emphasizing the need for effective parasiticides. The increasing global awareness of zoonotic diseases has prompted governments and animal health organizations to advocate for regular and strategic use of animal parasiticides.

Governments and international health bodies are allocating resources and implementing regulations to combat zoonotic diseases. For instance, the Food and Agriculture Organization (FAO) and the World Organisation for Animal Health (OIE) collaborate to control zoonoses globally. As a result, the demand for animal parasiticides has witnessed a substantial rise. This growing recognition of the interdependence of human and animal health is a driving force behind the market’s expansion.

Rising Pet Ownership and Human-Animal Bond

Another key driver of the animal parasiticides market is the surge in pet ownership and the deepening bond between humans and their companion animals. The global pet population has been steadily increasing, with dogs, cats, and other pets becoming integral parts of families worldwide. According to the American Pet Products Association (APPA), around 67% of U.S. households own a pet, translating to approximately 84.9 million homes. As pets are considered family members, there is a heightened focus on their health and well-being.

This shift in perception has led to an increased demand for high-quality veterinary care, including preventive measures against parasites. Pet owners are more willing to invest in advanced parasiticides to ensure the optimal health of their animals. The bond between humans and pets is further driving innovations in parasiticide formulations, such as spot-on treatments and oral medications, contributing to the market’s growth. The emotional connection between pet owners and their animals is a compelling factor propelling the animal parasiticides market forward.

Animal Parasiticides Market Restraints

Environmental Concerns and Resistance Development

One significant restraint affecting the animal parasiticides market is the growing concern about environmental impact and the development of resistance in parasites. Some conventional parasiticides contain chemical compounds that, when improperly disposed of, may pose risks to ecosystems and aquatic life. The United Nations Environment Programme (UNEP) highlights the environmental consequences of certain parasiticide residues, emphasizing the need for sustainable and eco-friendly alternatives. Additionally, the persistent use of the same class of parasiticides has led to resistance development in various parasites, diminishing the efficacy of treatments. According to the World Organisation for Animal Health (OIE), resistance has been reported in parasites affecting livestock, raising concerns about the long-term effectiveness of existing parasiticides. This resistance not only hampers the ability to control parasitic infections but also necessitates the development of new, more potent formulations, adding to research and development costs for manufacturers. Consequently, environmental considerations and resistance challenges pose substantial restraints on the animal parasiticides market.

Regulatory Hurdles and Stringent Approval Processes

Another significant restraint for the animal parasiticides market is the presence of regulatory hurdles and stringent approval processes for new products. Government agencies such as the U.S. Environmental Protection Agency (EPA) and the European Medicines Agency (EMA) impose rigorous standards to ensure the safety, efficacy, and environmental impact of animal parasiticides. The approval process involves extensive testing, which can be time-consuming and costly for manufacturers. Delays in obtaining regulatory approvals can hinder the timely market entry of new parasiticides, impacting the revenue streams for companies. Furthermore, changing regulatory landscapes and evolving compliance requirements necessitate ongoing adjustments, further complicating market dynamics. The need for compliance with multiple regulatory frameworks across different regions adds an additional layer of complexity, particularly for companies operating in global markets. As a result, navigating these regulatory hurdles becomes a substantial restraint, influencing the pace of innovation and market growth in the Animal Parasiticides sector.

Animal Parasiticides Market Opportunities

Increasing Demand for Organic and Natural Parasiticides

An opportunity within the animal parasiticides market lies in the rising demand for organic and natural parasiticides. With growing awareness of environmental sustainability and concerns about chemical residues in animal products, there is a shift toward eco-friendly and naturally derived parasiticides. Organizations such as the Organic Materials Review Institute (OMRI) play a crucial role in certifying products as compliant with organic standards. The global market for organic pet food, including products with organic parasiticides, is experiencing substantial growth. According to the Research Institute of Organic Agriculture (FiBL), the global market for organic pet food witnessed a 14% increase in sales in 2020.

Manufacturers have the opportunity to capitalize on this trend by developing and marketing parasiticides derived from natural sources, emphasizing their efficacy while minimizing environmental impact. As consumer preferences align with sustainable and natural alternatives, the animal parasiticides market has the potential to expand by meeting this demand for organic and eco-friendly solutions.

Advancements in Precision Livestock Farming

Another opportunity for the animal parasiticides market is linked to advancements in precision livestock farming. Integrating technologies such as IoT (Internet of Things), RFID (Radio-Frequency Identification), and data analytics enables real-time monitoring of animal health and behavior. This technology allows for the early detection of parasitic infections, enabling timely intervention with targeted parasiticides. Precision livestock farming enhances the efficiency of parasiticide use, reducing unnecessary treatments and minimizing the risk of resistance development.

According to the Food and Agriculture Organization (FAO), the adoption of precision livestock farming is increasing globally, with benefits including improved productivity and resource efficiency. Manufacturers in the animal parasiticides market can seize this opportunity by developing products that align with precision farming practices, providing farmers with effective tools for targeted parasite management. As precision farming gains traction, the integration of advanced technologies into parasiticide solutions can enhance their effectiveness, contributing to market growth in the context of evolving agricultural practices.

Animal Parasiticides Market Challenges

Global Economic Uncertainty and Cost Sensitivity

A significant challenge facing the animal parasiticides market is the impact of global economic uncertainty and the resulting cost sensitivity among consumers and livestock producers. Economic downturns and financial instability can lead to reduced disposable income for pet owners and diminished profit margins for farmers. In times of economic hardship, consumers may cut back on discretionary spending, including veterinary care and preventive measures such as parasiticides. The Food and Agriculture Organization (FAO) reports that economic challenges can affect the affordability of animal health products, potentially leading to suboptimal parasite control practices in livestock.

Manufacturers in the animal parasiticides market must navigate these economic fluctuations and develop pricing strategies that balance affordability with the need for effective parasiticides. Additionally, economic challenges may impact research and development budgets, affecting the introduction of new and innovative parasiticide formulations. Adapting to the economic landscape while maintaining product efficacy is a complex challenge that requires strategic planning and market responsiveness.

Trade Barriers and Regulatory Divergence

Another significant challenge for the animal parasiticides market is the presence of trade barriers and regulatory divergence across different regions. The variability in regulatory frameworks and approval processes can hinder the seamless global distribution of parasiticides. The World Trade Organization (WTO) emphasizes the importance of international standards and harmonization to facilitate trade in animal health products. However, differing regulatory requirements and approval timelines can create obstacles for manufacturers seeking to enter multiple markets.

Trade barriers and regulatory divergence not only complicate market access but also contribute to delays in product launches and increased compliance costs. Companies operating in the animal parasiticides market must invest in understanding and navigating diverse regulatory landscapes, which may involve adapting formulations, conducting additional testing, and engaging with regulatory authorities in each region. The challenge lies in developing strategies that ensure compliance with various regulations while maintaining efficiency in product development and market entry.

Regional Trends

North America: In North America, the animal parasiticides market has seen a growing emphasis on preventive healthcare for pets and livestock. Pet owners increasingly prioritize regular veterinary care, including the use of parasiticides. Additionally, the livestock sector focuses on sustainable and organic practices, driving demand for eco-friendly parasiticides. Government agencies like the U.S. Environmental Protection Agency (EPA) play a role in regulating and approving animal health products.

Europe: Europe exhibits a trend towards stricter regulations concerning the safety and environmental impact of animal parasiticides. There is an increasing demand for natural and organic parasiticides, aligning with the region’s strong emphasis on environmental sustainability. The European Medicines Agency (EMA) plays a significant role in regulating veterinary medicines, including parasiticides, ensuring their safety for animals and the environment.

Asia Pacific: The Asia Pacific region experiences a surge in demand for animal parasiticides due to the growth in pet ownership and intensification of livestock farming. The focus on food safety and quality in countries like China drives the adoption of parasiticides in the livestock sector. Additionally, increasing awareness of zoonotic diseases contributes to the use of parasiticides for disease prevention. Government bodies, such as China’s Ministry of Agriculture and Rural Affairs, play a role in regulating animal health products.

Middle East and Africa: In the Middle East and Africa, the animal parasiticides market is influenced by factors such as the predominance of pastoral farming and the prevalence of vector-borne diseases. The need to enhance livestock productivity and prevent the spread of diseases drives the adoption of parasiticides. Government initiatives and organizations like the Food and Agriculture Organization (FAO) of the United Nations may contribute to awareness and regulation in the region.

Latin America: Latin America experiences trends similar to other regions, with a growing pet population and an increasing awareness of zoonotic diseases. The livestock sector, particularly in countries with significant agricultural activities, drives demand for parasiticides. Government bodies, such as Brazil’s Ministry of Agriculture, Livestock and Food Supply (MAPA), may regulate the use of animal health products, including parasiticides. The region’s diverse climates and ecosystems also influence the prevalence of different parasites, impacting the types of parasiticides in demand.

Key Players

Key players operating in the global animal parasiticides market are Boehringer Ingelheim GmbH, Elanco Animal Health Incorporated, Zoetis Inc., Merck & Co., Inc, Vetoquinol S.A., Petiq, LLC, Virbac, Sequent Scientific Limited, Krka Group, ECO Animal Health Group PLC, Ceva SantÉ Animale, Bimeda Animal Health, Norbrook, Chanelle Pharma, Kyoritsu Seiyaku Corporation, Ucbvet, Smartvet Holdings, Inc., and Calier.

PRICE

ASK FOR FREE SAMPLE REPORT