Global ADAS Market, By System Type (Adaptive Cruise Control, Adaptive Front Light, Automatic Emergency Braking, Forward Collision Warning, Blind-Spot Detection, Cross-Traffic Alert, Driver Monitoring System, Night Vision System, Intelligent Park Assist, Lane Departure Warning, Road Sign Recognition, Pedestrian Detection System, Traffic Jam Assist, Tire Pressure Monitoring System), Level of Autonomy (L1, L2, L3, L4, L5), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Trucks, Buses), Electric Vehicle Type (Battery Electric Vehicles, Fuel Cell Electric Vehicles, Hybrid Electric Vehicles, Plug-In Hybrid Electric Vehicles), Component (Camera Unit, LiDAR, Radar Sensors, Ultrasonic Sensors, Infrared Sensors), Sales Channel (OEM, Aftermarket), Offering (Hardware, Software), and Region — Industry Analysis and Forecast to 2030

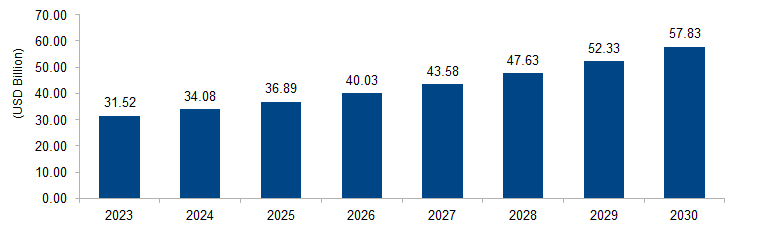

The global ADAS market is expected to grow from USD 31.52 billion in 2023 to USD 57.83 billion by 2030 at a CAGR of 9.1%. The Advanced Driver Assistance Systems (ADAS) market is propelled by escalating demand for enhanced safety features in vehicles, driven by a growing awareness of road safety. Regulatory mandates mandating the incorporation of safety technologies further fuel market growth. Technological advancements, such as autonomous driving capabilities and sensor innovations, also contribute significantly to the expanding ADAS market.

Figure 1: Global ADAS Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

ADAS, or Advanced Driver Assistance Systems, refers to a set of innovative technologies designed to enhance vehicle safety and improve driving experiences. These systems utilize sensors, cameras, radar, and other sophisticated technologies to assist drivers in various aspects of driving. ADAS features include adaptive cruise control, lane departure warning, automatic emergency braking, and parking assistance. The primary goal is to prevent accidents, mitigate collision impacts, and provide drivers with real-time information, thereby promoting safer and more efficient driving. As technology advances, ADAS plays a pivotal role in the evolution towards semi-autonomous and autonomous vehicles, revolutionizing the automotive industry’s safety standards.

ADAS Market Drivers

Growing Awareness of Road Safety

The surge in awareness regarding road safety is a significant driver propelling the Advanced Driver Assistance Systems (ADAS) market. Governments and regulatory bodies worldwide are increasingly focusing on implementing stringent safety norms to reduce road accidents and fatalities. For instance, the National Highway Traffic Safety Administration (NHTSA) in the United States emphasizes the importance of advanced safety technologies. As of 2021, NHTSA reports that vehicles equipped with forward-collision warning and automatic emergency braking witnessed a 56% reduction in rear-end crashes. This heightened awareness is reflected in the European New Car Assessment Programme (Euro NCAP), where safety ratings encourage the adoption of ADAS features. Such initiatives have led to a notable surge in the integration of ADAS technologies, as automakers strive to meet safety standards, fostering the market’s growth.

Regulatory Mandates Driving Adoption

The ADAS market experiences a robust push due to regulatory mandates that mandate the incorporation of safety technologies in vehicles. Governments globally are enacting and enforcing regulations that necessitate the inclusion of specific ADAS features to enhance road safety. For example, the European Union has introduced legislation making certain ADAS features mandatory, aiming to reduce accidents and improve overall traffic safety. These regulations include the requirement for advanced safety systems like lane-keeping assistance and advanced emergency braking systems. As of 2022, the European Commission estimates that these measures could save over 25,000 lives and prevent at least 140,000 serious injuries by 2038. The regulatory landscape’s evolving nature continues to drive automakers to integrate ADAS technologies, fostering a steady market expansion as they strive to comply with these mandates and enhance vehicle safety standards.

ADAS Market Restraints

High Initial Costs and Limited Consumer Affordability

A significant restraint for the Advanced Driver Assistance Systems (ADAS) market is the high initial costs associated with integrating these advanced technologies into vehicles. The expense of incorporating sensors, cameras, and radar systems, along with the required computing infrastructure, increases the overall production cost of automobiles. This cost burden is often transferred to consumers, making ADAS-equipped vehicles relatively more expensive. According to data from the U.S. Department of Transportation, as of 2021, the average cost of a new car in the United States was around $40,000, with additional safety features contributing to price hikes. This pricing dynamic limits the affordability of ADAS-equipped vehicles for a substantial portion of the consumer base, hindering mass adoption. Striking a balance between enhancing safety and maintaining affordability remains a challenge for the ADAS market, particularly as consumers weigh the value proposition against the additional cost.

Challenges in Standardization and Interoperability

Another restraint faced by the ADAS market revolves around the challenges related to standardization and interoperability. The absence of globally standardized protocols for ADAS technologies poses hurdles in achieving seamless integration and communication between different systems. Divergent regulatory frameworks and technical specifications across regions complicate efforts to establish uniform standards. For instance, while certain safety features may be mandatory in one region, they may not be obligatory elsewhere. This lack of harmonization inhibits the interoperability of ADAS systems, hindering the development of a cohesive, interconnected automotive safety network. The International Organization for Standardization (ISO) and other standard-setting bodies are working towards addressing these challenges. However, as of 2022, achieving a universally accepted standard remains an ongoing process. This lack of standardization not only complicates the manufacturing process for automakers but also limits the effectiveness of ADAS technologies in providing a seamless and consistent safety experience for drivers on a global scale.

ADAS Market Opportunities

Evolution towards Autonomous Driving

An immense opportunity for the Advanced Driver Assistance Systems (ADAS) market lies in the gradual shift towards autonomous driving. ADAS technologies serve as crucial building blocks for achieving higher levels of vehicle autonomy. As governments and industry stakeholders envision a future with self-driving vehicles, ADAS features such as adaptive cruise control, automatic lane-keeping, and advanced collision avoidance systems become integral components. The Society of Automotive Engineers (SAE) classifies autonomous driving into levels ranging from Level 1 (driver assistance) to Level 5 (full automation). As of 2022, the global automotive industry is progressing towards higher autonomy levels, creating a substantial market opportunity. For instance, the Chinese government’s Automotive Industry Development Policy aims for 50% of new vehicles sold to be equipped with ADAS by 2025, fostering a conducive environment for autonomous driving advancements.

Rising Integration of AI and Machine Learning

The increasing integration of Artificial Intelligence (AI) and Machine Learning (ML) within ADAS presents a notable opportunity for market expansion. These technologies enhance the capabilities of ADAS systems, enabling more sophisticated and context-aware decision-making. AI algorithms analyze vast amounts of data from sensors and cameras in real-time, improving the accuracy of object detection, traffic prediction, and hazard recognition. The global AI in automotive market is anticipated to grow at a CAGR of around 39% from 2021 to 2027. ADAS leveraging AI not only enhances safety but also opens avenues for predictive maintenance and personalized driving experiences. The integration of AI and ML in ADAS systems aligns with the industry’s trajectory towards intelligent and connected vehicles, offering a significant opportunity for technology advancements and market growth in the evolving automotive landscape.

ADAS Market Challenges

Cybersecurity Concerns

A critical challenge facing the Advanced Driver Assistance Systems (ADAS) market is the growing cybersecurity threat. As vehicles become more connected and reliant on digital technologies, they become susceptible to cyber-attacks. The interconnected nature of ADAS, with sensors and communication systems exchanging data, poses vulnerabilities that malicious actors may exploit. The U.S. Department of Homeland Security reported a significant increase in automotive cybersecurity incidents, with the number of vulnerabilities rising by 47% in 2021. Ensuring the security of ADAS systems is paramount to prevent unauthorized access, data breaches, and potential manipulation of critical functions. The automotive industry faces the challenge of developing robust cybersecurity frameworks and standards to safeguard ADAS technologies, maintaining trust in the safety and reliability of connected vehicles.

Infrastructure Readiness and Standardization

A substantial challenge for the ADAS market is the lack of standardized infrastructure and road-readiness for advanced technologies. While vehicles equipped with ADAS features rely on road infrastructure and communication networks for optimal functionality, the readiness of these elements varies globally. Inconsistencies in road markings, signage, and communication infrastructure can lead to challenges in the accurate interpretation of data by ADAS systems. The absence of standardized communication protocols between vehicles and infrastructure further hampers the seamless operation of ADAS technologies. According to the World Economic Forum, achieving global interoperability for connected and autonomous vehicles remains a significant challenge, with infrastructure readiness varying widely between regions. Addressing these challenges requires collaborative efforts between governments, industry stakeholders, and standard-setting bodies to establish uniform standards and ensure the widespread deployment and effectiveness of ADAS technologies on a global scale.

Regional Trends

North America: The North American ADAS market has seen a surge in the adoption of safety technologies driven by regulatory initiatives and a heightened focus on reducing road accidents. The United States, in particular, has been at the forefront of implementing safety standards, encouraging the integration of ADAS features. Trends include the increasing deployment of lane departure warning systems, automatic emergency braking, and adaptive cruise control.

Europe: Asia Pacific: The Asia Pacific region, particularly countries like China, Japan, and South Korea, has witnessed a rapid adoption of ADAS technologies. Government initiatives to improve road safety and the presence of prominent automotive manufacturers contribute to this growth. The trends include the integration of AI and machine learning in ADAS, as well as a focus on developing infrastructure to support connected and autonomous vehicles.

Middle East and Africa: Latin America: Latin America has been gradually embracing ADAS technologies, with a focus on features that enhance safety and overall driving experience. Economic factors play a role in the pace of adoption, and as affordability increases, the market is expected to witness a rise in the integration of basic ADAS features.

Key Players

Key players operating in the global ADAS market are Continental AG, Robert Bosch, Denso, Magna International, ZF Friedrichshafen, Aptiv, Valeo, NVIDIA, Hyundai Mobis, Intel, NXP Semiconductors, Autoliv, Hitachi Automotive, Aisin Corporation, Infineon Technologies AG, Renesas Electronics Corporation, Hella, and Ficosa International SA.

PRICE

ASK FOR FREE SAMPLE REPORT