Global Food Diagnostics Market, By Site (Inhouse, Outsourcing Facility), Type (Systems, Test Kits, Consumables), Food Tested (Meat, Poultry, and Seafood, Dairy Products, Processed Food, Cereals, Grains, and Pulses, Nuts, Seeds, and Spices), Testing Type (Quality, Safety), and Region — Industry Analysis and Forecast to 2030

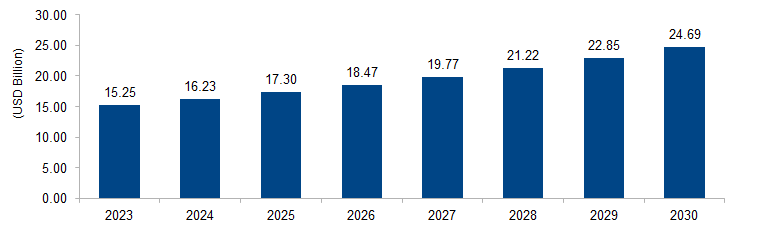

The global food diagnostics market is expected to grow from USD 15.25 billion in 2023 to USD 24.69 billion by 2030 at a CAGR of 7.1%. The market is propelled by increasing concerns about food safety and quality. Stringent regulations, heightened awareness among consumers, and frequent foodborne outbreaks drive the demand for advanced diagnostic technologies. Innovations in testing methods, including PCR and immunoassays, play a pivotal role in ensuring the rapid and accurate detection of contaminants, pathogens, and allergens in the global food supply chain.

Figure 1: Global Food Diagnostics Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Food diagnostics involves the application of various techniques and technologies to assess the safety, quality, and authenticity of food products. It encompasses a range of methods, including molecular biology, immunology, and other analytical techniques, to detect contaminants, pathogens, allergens, and other substances in food. This field ensures compliance with food safety regulations, verifies product labeling, and addresses concerns related to foodborne illnesses. Food diagnostics plays a crucial role in safeguarding public health, supporting regulatory compliance for manufacturers, and maintaining consumer confidence by providing accurate and reliable information about the safety and composition of food items throughout the production and supply chain.

Food Diagnostics Market Drivers

Stringent Food Safety Regulations

One key driver of the food diagnostics market is the implementation of stringent food safety regulations globally. Governments and regulatory bodies, such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), continually enforce rigorous standards to ensure the safety and quality of food products. These regulations mandate comprehensive testing for contaminants, pathogens, and allergens, driving the demand for advanced diagnostic technologies. For instance, the Food Safety Modernization Act (FSMA) in the United States emphasizes preventive measures and requires increased testing, creating a substantial market for diagnostic solutions. Globally, the Codex Alimentarius sets international food safety standards, contributing to a consistent need for reliable food diagnostics technologies to meet regulatory compliance.

Rising Incidence of Foodborne Diseases

The increasing incidence of foodborne diseases is a significant driver propelling the food diagnostics market. Outbreaks of illnesses caused by contaminated food have heightened consumer awareness and regulatory scrutiny. Governments and health organizations worldwide are emphasizing the importance of early detection and prevention through robust food testing procedures. According to the World Health Organization (WHO), millions of people fall ill and thousands die annually due to contaminated food. This has led to a surge in demand for diagnostic tools capable of rapidly identifying pathogens, toxins, and contaminants in the food supply chain. The market is driven by the urgent need for technologies that can ensure the safety of food products and prevent widespread outbreaks, contributing to the overall health and well-being of the global population.

Food Diagnostics Market Restraints

High Initial Investment Costs

A significant restraint in the food diagnostics market is the high initial investment required for implementing advanced diagnostic technologies. Acquiring and installing state-of-the-art equipment, such as polymerase chain reaction (PCR) machines, mass spectrometers, and immunoassay systems, can be capital-intensive for food manufacturers and testing laboratories. The cost of training personnel to operate these sophisticated systems further adds to the financial burden. According to the Food and Agriculture Organization (FAO), many small and medium-sized enterprises (SMEs) in the food industry, especially in developing regions, may find it challenging to afford such investments. This economic barrier limits the widespread adoption of advanced food diagnostic technologies, hindering smaller players from fully participating in ensuring comprehensive food safety and quality.

Complex Regulatory Landscape

The complex regulatory landscape poses another significant restraint on the food diagnostics market. The varying regulations and standards across different regions and countries create challenges for manufacturers and testing laboratories to navigate and comply with diverse requirements. For instance, the European Union and the United States may have distinct regulatory frameworks for food safety testing. This complexity not only increases the cost of compliance but also creates uncertainties and delays in the approval processes for diagnostic technologies. The Food and Drug Administration (FDA), European Food Safety Authority (EFSA), and other regulatory bodies regularly update and modify standards, requiring continuous adaptation from industry stakeholders. This dynamic regulatory environment can impede the swift introduction and adoption of new diagnostic technologies, constraining market growth and innovation in the food diagnostics sector.

Food Diagnostics Market Opportunities

Increasing Consumer Demand for Transparency

An opportunity for the food diagnostics market lies in the growing consumer demand for transparency in the food supply chain. Consumers are becoming more discerning and are seeking detailed information about the origin, production methods, and safety of the food they consume. This demand aligns with the concept of food traceability, where consumers want to trace the entire journey of a product from farm to table. The adoption of advanced diagnostic technologies, such as DNA-based testing and blockchain solutions, presents an opportunity to provide verifiable and transparent information. According to surveys conducted by organizations like the International Food Information Council Foundation (IFIC), consumers are willing to pay more for products with enhanced traceability and safety assurances. This trend offers a strategic opportunity for the food diagnostics market to integrate technologies that bolster transparency, build consumer trust, and meet the evolving expectations of a more informed and conscious consumer base.

Integration of IoT and Big Data Analytics

The integration of Internet of Things (IoT) and big data analytics presents a significant opportunity for the food diagnostics market. IoT-enabled sensors and devices can be incorporated into the food production and distribution process to collect real-time data on various parameters, including temperature, humidity, and contamination levels. This data, when analyzed through big data analytics, can offer valuable insights into the entire supply chain, helping identify potential risks and areas for improvement. The Food and Agriculture Organization (FAO) highlights the transformative potential of IoT in enhancing food safety. By leveraging IoT and analytics, the industry can proactively monitor and manage the quality and safety of food products, reducing the risk of contamination and ensuring compliance with stringent regulations. This technological integration not only enhances efficiency but also opens up new avenues for innovation and data-driven decision-making in the food diagnostics sector, fostering a more resilient and responsive food safety ecosystem.

Food Diagnostics Market Challenges

Global Supply Chain Complexity

A significant challenge faced by the food diagnostics market is the complexity of the global food supply chain. The interconnected nature of modern food systems involves the movement of ingredients and finished products across borders, making it challenging to trace and monitor every step of the supply chain. The Food and Agriculture Organization (FAO) notes that this complexity increases the risk of contamination incidents and poses difficulties in implementing effective diagnostic measures uniformly. Different regions have distinct production practices, and variations in regulatory frameworks further compound the challenges of maintaining a standardized approach. Addressing this challenge requires international collaboration, the adoption of harmonized standards, and the integration of technologies that can provide real-time visibility and traceability throughout the global food supply chain.

Emerging Pathogens and Contaminants

The emergence of new pathogens and contaminants poses a continuous and evolving challenge for the food diagnostics market. Microbial pathogens and contaminants can evolve, adapt, or emerge in response to changes in agricultural practices, climate, and international trade. The World Health Organization (WHO) highlights the unpredictable nature of emerging foodborne hazards, necessitating constant vigilance and adaptability in diagnostic capabilities. Traditional diagnostic methods may not always be equipped to detect novel contaminants, requiring ongoing investment in research and development to enhance detection capabilities. The dynamic nature of these challenges is evident in instances of outbreaks related to previously unknown pathogens. Food diagnostics must continuously evolve to stay ahead of emerging threats, emphasizing the need for agile and responsive diagnostic technologies. This challenge underscores the importance of research collaboration, investment in innovative technologies, and a proactive approach to identifying and mitigating emerging risks in the food supply chain.

Regional Trends

North America: In North America, the food diagnostics market has been characterized by a focus on advanced technologies to ensure food safety and compliance with stringent regulations. There is a growing emphasis on adopting rapid testing methods, including PCR and next-generation sequencing, to enhance the speed and accuracy of diagnostics. Additionally, the region has seen increased collaboration between regulatory bodies, such as the FDA, and industry stakeholders to address emerging challenges in food safety. The use of blockchain and IoT for traceability and transparency in the supply chain is also a notable trend.

Europe: Europe has witnessed a rise in demand for food diagnostics driven by the region’s commitment to ensuring high food safety standards. The adoption of technologies like biosensors, spectroscopy, and immunoassays has been notable. Europe is also increasingly focused on addressing issues related to food fraud, with the implementation of measures to enhance authenticity testing. The European Food Safety Authority (EFSA) plays a key role in providing scientific advice and risk assessments, influencing trends in food diagnostics.

Asia Pacific: In the Asia Pacific region, the food diagnostics market has seen a surge in growth due to the increasing awareness of food safety issues and the expansion of the food industry. There is a trend toward adopting cost-effective and efficient diagnostic technologies, particularly in emerging economies. Governments in the region are working to strengthen regulatory frameworks, and collaborations between public and private sectors are fostering advancements in food safety practices. Rapid urbanization and a rising middle class contribute to the demand for reliable food diagnostics.

Middle East and Africa: In the Middle East and Africa, the food diagnostics market is influenced by efforts to improve food safety practices. The region has seen investments in infrastructure and technology to enhance diagnostic capabilities. Governments are working on regulatory frameworks to ensure compliance with international standards. Additionally, there is a growing awareness of the importance of food diagnostics in preventing foodborne illnesses, leading to increased adoption of testing methods.

Latin America: Latin America has been experiencing a shift toward more sophisticated food safety measures. The region has witnessed increased investment in research and development to address specific challenges related to local agricultural practices. Governments and industry players are working collaboratively to implement advanced diagnostics for both export-oriented agriculture and domestic consumption. The emphasis on addressing contamination issues and ensuring compliance with international standards is driving trends in the Latin American Food Diagnostics market.

Key Players

Key players operating in the global food diagnostics market are Thermo Fisher Scientific Inc., Merck KGaA, Bio-Rad Laboratories, Inc., Neogen Corporation, Shimadzu Corporation, Agilent Technologies, Inc., Qiagen, bioMérieux, Bruker, Danaher, FOSS, Hygiena LLC, Perkinelmer Inc., R-Biopharm AG, Romer Labs Division Holding, Envirologix, Promega Corporation, and Randox Food Diagnostics.

PRICE

ASK FOR FREE SAMPLE REPORT