Global Dairy Alternatives Market, Source (Soy, Almond, Coconut, Rice, Oats, Hemp), Formulation (Flavored, Plain), Application (Milk, Ice Cream, Yogurt, Cheese, Creamers, Butter), Distribution Channel (Retail, Food Services, Online Stores), and Region — Industry Analysis and Forecast to 2030

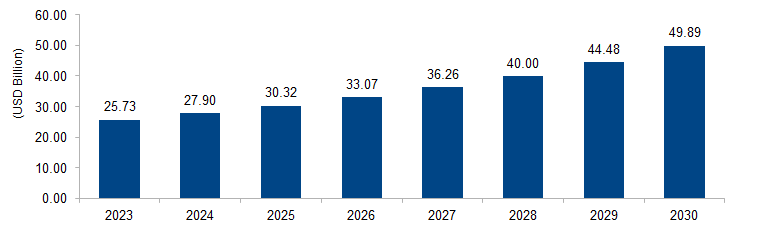

The global dairy alternatives market is expected to grow from USD 25.73 billion in 2023 to USD 49.89 billion by 2030 at a CAGR of 9.9%. The market is driven by a surge in consumer demand for plant-based, lactose-free alternatives due to health and sustainability concerns. Increasing lactose intolerance awareness, coupled with environmental considerations, propels the adoption of plant-derived options like almond, soy, and oat milk. Growing consumer preferences for dairy-free choices underscore the market’s expansion.

Figure 1: Global Dairy Alternatives Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

Dairy alternatives refer to plant-based products designed to replicate or replace traditional dairy items, catering to individuals seeking lactose-free or vegan options. These alternatives include plant-derived milk, such as soy, almond, and oat milk, as well as substitutes for yogurt, cheese, and ice cream. Driven by health consciousness, environmental sustainability, and dietary preferences, consumers choose dairy alternatives for various reasons, including lactose intolerance, ethical concerns, and a desire for a more diverse and plant-centric diet. Dairy alternatives offer a wide range of flavors and textures, contributing to the growing popularity of plant-based options in the evolving landscape of modern food choices.

Dairy Alternatives Market Drivers

Lactose Intolerance Awareness and Health Consciousness

A prominent driver of the dairy alternatives market is the increasing awareness of lactose intolerance and the broader shift toward health-conscious dietary choices. According to the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), approximately 65% of the global population has a reduced ability to digest lactose after infancy. As awareness of lactose intolerance grows, individuals seek dairy alternatives to avoid digestive discomfort. Moreover, the perception that dairy alternatives, such as almond or soy milk, may offer health benefits like lower cholesterol and saturated fat content contributes to their popularity. The demand for plant-based alternatives aligns with broader health and wellness trends, with consumers making conscious choices to adopt diets perceived as healthier, contributing to the expanding Dairy Alternatives market.

Environmental Sustainability and Ethical Considerations

Environmental sustainability emerges as a significant driver propelling the dairy alternatives market. The livestock industry, particularly dairy farming, is associated with environmental challenges such as greenhouse gas emissions, land use, and water consumption. Consumers, informed about the environmental impact of traditional dairy production, are opting for plant-based alternatives as a more sustainable choice. The Food and Agriculture Organization (FAO) recognizes the role of plant-based diets in mitigating environmental impact. Ethical considerations, including animal welfare concerns and a desire to reduce one’s ecological footprint, drive the shift toward dairy alternatives. As individuals increasingly align their purchasing decisions with environmental and ethical values, the dairy alternatives market experiences growth driven by a conscious choice to opt for sustainable and cruelty-free alternatives to traditional dairy products.

Dairy Alternatives Market Restraints

Nutritional Disparities and Fortification Challenges

A significant restraint in the dairy alternatives market is the nutritional disparities between traditional dairy products and their plant-based alternatives. While dairy products are naturally rich in nutrients such as calcium, vitamin D, and protein, plant-based alternatives may lack these essential components or possess them in varying quantities. The American Journal of Clinical Nutrition highlights that, in certain cases, plant-based milk substitutes may have lower protein content, potentially impacting nutritional adequacy. Despite efforts to fortify plant-based alternatives, achieving nutrient parity remains challenging. The availability and bioavailability of fortified nutrients in dairy alternatives may not match those in dairy, leading to nutritional concerns. Overcoming these challenges requires innovation in fortification techniques and addressing nutritional disparities to ensure that consumers can make informed choices without compromising essential dietary elements.

Ingredient Sourcing and Supply Chain Constraints

A notable restraint for the dairy alternatives market lies in ingredient sourcing and supply chain constraints. The production of plant-based alternatives often relies on ingredients like almonds, soy, and oats, whose availability and sourcing can be affected by external factors. Climate change, for instance, impacts the yield and stability of these crops. The Food and Agriculture Organization (FAO) recognizes climate-related challenges in agriculture, which may affect the raw materials for dairy alternatives. Supply chain disruptions, such as those experienced during the COVID-19 pandemic, underscore the vulnerability of relying on specific ingredients for plant-based products. Additionally, the global demand for certain plant-based ingredients may lead to price fluctuations and availability issues. Addressing these challenges requires diversifying ingredient sources, investing in sustainable agriculture practices, and developing resilient supply chains to ensure the consistent production and availability of dairy alternatives.

Dairy Alternatives Market Opportunities

Functional Dairy Alternatives for Health and Wellness

An emerging opportunity in the dairy alternatives market lies in the development of functional plant-based products designed to promote health and wellness. The shift toward incorporating health-beneficial ingredients, such as probiotics, vitamins, and minerals, into dairy alternatives is gaining traction. According to the American Journal of Clinical Nutrition, there is growing interest in fortifying plant-based milks with nutrients traditionally associated with dairy, aiming to offer enhanced nutritional value. This presents an opportunity for manufacturers to create innovative and functional dairy alternatives that not only mimic traditional dairy in taste and texture but also provide additional health benefits. The market can capitalize on the rising consumer demand for products that support digestive health, immune function, and overall well-being, driving the development of a new generation of functional dairy alternatives.

Customization and Personalization of Dairy Alternatives

An exciting opportunity in the dairy alternatives market is the potential for customization and personalization to meet individual taste preferences and nutritional needs. The American Journal of Clinical Nutrition notes that consumers are increasingly seeking personalized nutrition experiences. Manufacturers can explore this trend by offering customizable dairy alternatives, allowing consumers to adjust sweetness levels, choose fortification options, or even customize flavor profiles. The customization trend extends to addressing specific dietary requirements, such as low-sugar or high-protein preferences. This not only caters to diverse consumer preferences but also enhances brand loyalty and consumer engagement. As consumers become more discerning and seek products tailored to their unique preferences and dietary goals, the dairy alternatives market can capitalize on this opportunity by offering a range of customizable and personalized options to meet the evolving demands of a diverse consumer base.

Dairy Alternatives Market Challenges

Texture and Mouthfeel Challenges

A significant challenge facing the dairy alternatives market is replicating the desired texture and mouthfeel of traditional dairy products. Achieving a texture akin to dairy, especially in products like cheese and yogurt, remains a complex task. The Journal of Food Science highlights the challenges associated with mimicking the creamy and smooth texture of dairy in plant-based alternatives. While advancements have been made in developing plant-based textures, achieving the exact mouthfeel and consistency remains elusive. Consumers often compare dairy alternatives based on their textural resemblance to traditional dairy, and any deviation may impact acceptance. Overcoming texture challenges requires ongoing research into ingredient functionality, processing techniques, and formulation methods to achieve textures that closely match or surpass the sensory experience of conventional dairy products. The market must address these challenges to enhance consumer acceptance and satisfaction with dairy alternatives.

Price Competitiveness and Affordability

A notable challenge in the dairy alternatives market is the price competitiveness and affordability compared to traditional dairy products. While demand for plant-based alternatives is growing, these products can sometimes be priced higher than their dairy counterparts. The International Journal of Environmental Research and Public Health emphasizes that affordability remains a barrier for certain consumer segments, limiting widespread adoption. Factors such as the cost of raw materials, production processes, and limited economies of scale contribute to the pricing challenges. As demand increases, there is an opportunity for the dairy alternatives market to explore cost-effective sourcing, efficient production methods, and economies of scale to make these products more accessible to a broader consumer base. Overcoming the affordability challenge is crucial for ensuring that plant-based alternatives become a viable and competitive choice for a diverse range of consumers, irrespective of their economic considerations.

Regional Trends

North America: In North America, the dairy alternatives market has experienced a surge in demand driven by a growing preference for plant-based options. Consumers are increasingly adopting dairy alternatives such as almond milk, soy milk, and oat milk as part of their diet. The trend is fueled by factors such as lactose intolerance awareness, health consciousness, and environmental concerns. Major retailers and foodservice outlets in the region have expanded their offerings of plant-based dairy alternatives, responding to the demand for diverse and sustainable choices.

Europe: Europe has witnessed a similar trend of increased adoption of dairy alternatives, with a particular focus on environmental sustainability and ethical considerations. Plant-based milk alternatives, vegan cheeses, and yogurts have gained popularity. The European market has seen a rise in innovative products, including those made from lesser-known plant sources. Government initiatives supporting sustainable agriculture and healthier food choices contribute to the growth of the dairy alternatives market in Europe.

Asia Pacific: In the Asia Pacific region, the dairy alternatives market has seen substantial growth, driven by factors such as a large vegetarian population, increasing awareness of plant-based diets, and the introduction of diverse dairy alternatives in the market. Traditional plant-based products like soy milk have been widely consumed, and there is a growing market for newer alternatives such as almond milk, coconut milk, and plant-based yogurt. The Asia Pacific market has also witnessed the entry of international and local brands offering a variety of dairy-free options.

Middle East and Africa: In the Middle East and Africa, there is a developing interest in dairy alternatives, influenced by health and wellness trends. Plant-based options, particularly nut-based milks and dairy-free yogurts, have gained traction in urban areas. Health-conscious consumers are exploring alternatives to traditional dairy products, creating opportunities for the growth of the dairy alternatives market in the region.

Latin America: Latin America has seen a rise in the popularity of dairy alternatives, driven by factors such as an increasing vegan and vegetarian population, rising health consciousness, and the availability of a variety of plant-based options. Traditional plant-based products like horchata (a rice-based beverage) and coconut milk have been consumed for years, and the market is expanding with the introduction of almond milk, soy milk, and other alternatives. The region is witnessing increased awareness of environmental sustainability, contributing to the adoption of dairy alternatives.

Key Players

Key players operating in the global dairy alternatives market are The Hain Celestial Group, Inc., Danone North America Public Benefit Corporation, Valsoia S.P.A., Sunopta, Freedom Foods Group Limited, Blue Diamond Growers, Oatly Group Ab, Sanitarium, Nutriops, S.L., Earth’s Own, Eden Foods, Inc., Green Spot Co., Ltd., Hiland Dairy, Triballat Noyal, Elmhurst Milked Direct LLC, Ripple Foods, Kite Hill, and Rude Health.

PRICE

ASK FOR FREE SAMPLE REPORT