Global Dry Type Transformer Market, By Technology (Cast Resin, Vacuum Pressure Impregnated (VPI)), Voltage (Low Voltage, Medium Voltage, High Voltage), Phase (Single Phase, Three Phase), Application (Industrial, Commercial, Utilities), and Region — Industry Analysis and Forecast to 2030

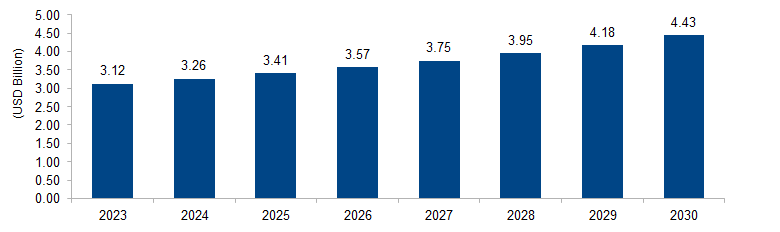

The global dry type transformer market is expected to grow from USD 6.24 billion in 2023 to USD 9.68 billion by 2030 at a CAGR of 6.5%. The dry type transformer market is propelled by the increasing focus on safety and environmental sustainability in electrical infrastructure. As a safer and eco-friendly alternative to oil-filled transformers, dry type transformers are witnessing higher adoption. Growing concerns about fire risks, reduced maintenance requirements, and regulatory emphasis on energy efficiency contribute to the market’s expansion.

Figure 1: Global Dry Type Transformer Market Size, 2023-2030 (USD Billion)

Source: Secondary Research, Expert Interviews, and MAARECO Analysis

A dry type transformer is an electrical transformer that uses air as a cooling medium instead of liquid dielectric substances such as oil. Unlike oil-filled transformers, it features encapsulated windings in epoxy resin or other solid insulation materials. This design eliminates the need for a liquid coolant, making it a safer and environmentally friendly option with reduced fire risks and maintenance requirements. Dry type transformers find applications in various industries, buildings, and power distribution systems, particularly in areas where safety, reliability, and compliance with stringent environmental standards are paramount.

Dry Type Transformer Market Drivers

Growing Emphasis on Safety and Environmental Sustainability

One significant driver of the dry type transformer market is the increasing emphasis on safety and environmental sustainability in the electrical power sector. Governments and industries globally are prioritizing technologies that minimize environmental impact and enhance workplace safety. Dry type transformers, using air as a cooling medium instead of oil, offer a safer and eco-friendly solution, mitigating the risks associated with oil-filled transformers. According to the International Energy Agency (IEA), the rising awareness of environmental concerns and stringent regulations regarding oil-filled transformers’ potential hazards contribute to the growing adoption of dry type transformers. The market benefits from the broader shift toward sustainable energy practices and a commitment to reducing the carbon footprint in power distribution systems.

Rising Demand for Energy Efficiency and Reduced Maintenance

The demand for energy-efficient solutions and reduced maintenance requirements serves as another key driver for the dry type transformer market. Dry type transformers offer advantages in terms of lower energy losses and enhanced efficiency compared to their oil-filled counterparts. The U.S. Department of Energy (DOE) emphasizes the importance of energy-efficient transformers in reducing electricity consumption and minimizing greenhouse gas emissions. Additionally, dry type transformers often require less maintenance, resulting in cost savings and improved reliability for end-users. As energy efficiency becomes a crucial consideration in power infrastructure development, the market for dry type transformers is poised for growth, driven by the desire to optimize energy usage and minimize operational costs in diverse industrial and commercial applications.

Dry Type Transformer Market Restraints

Initial Cost and Capital Investment Challenges

A significant restraint for the dry type transformer market is the comparatively higher initial cost and capital investment associated with these transformers. Dry type transformers utilize advanced insulation materials such as epoxy resin, which can increase manufacturing costs. According to the Institute of Electrical and Electronics Engineers (IEEE), the initial capital expenditure for dry type transformers is often higher than that for oil-filled transformers. This poses a challenge, especially for budget-conscious end-users or projects with strict cost considerations. While the long-term operational benefits and lower maintenance costs of dry type transformers contribute to a favorable lifecycle cost analysis, the higher upfront investment remains a deterrent for some potential buyers, hindering widespread adoption.

Limited Power Ratings for Large-Scale Applications

Another notable restraint in the dry type transformer market is the limitation on power ratings for large-scale applications. Dry type transformers are typically available in lower power ratings compared to oil-filled transformers, which are more commonly used in high-voltage and high-power applications. The U.S. Environmental Protection Agency (EPA) acknowledges the challenge of adapting dry type transformers to handle extremely high voltages and power levels. This limitation restricts the use of dry type transformers in certain utility and heavy industrial settings where large power capacities are essential. Overcoming this restraint requires continuous research and development efforts to expand the power ratings of dry type transformers, making them more versatile and suitable for a broader range of applications without compromising performance or safety standards.

Dry Type Transformer Market Opportunities

Integration with Smart Grid Technologies

An emerging opportunity for the dry type transformer market is the integration with smart grid technologies. Smart grids incorporate advanced communication and control systems to optimize the generation, distribution, and consumption of electricity. Dry type transformers, being a key component in power distribution networks, can play a pivotal role in modernizing grid infrastructure. According to the International Electrotechnical Commission (IEC), the increasing deployment of smart grids worldwide presents an opportunity for dry type transformers to contribute to grid resilience and efficiency. By incorporating digital monitoring and communication capabilities, dry type transformers can facilitate real-time data exchange, predictive maintenance, and enhanced grid intelligence. This integration aligns with the global trend towards smart cities and sustainable energy systems, presenting a growth avenue for the dry type transformer market as utilities and industries seek to modernize their power infrastructure.

Renewable Energy Integration and Distributed Generation

An opportunity for the dry type transformer market lies in the increasing integration of renewable energy sources and distributed generation. As the world transitions towards a more sustainable energy mix, the demand for dry type transformers is expected to rise in applications related to renewable energy projects. The International Energy Agency (IEA) highlights the growing contribution of renewable sources to global electricity generation. Dry type transformers, known for their environmental compatibility, can be deployed in solar and wind power installations, ensuring efficient and reliable energy distribution. Additionally, the rise of distributed generation, where power is generated close to the point of consumption, offers opportunities for smaller dry type transformers. These transformers play a vital role in stepping down voltage levels for localized renewable energy systems, supporting the transition towards decentralized and cleaner energy solutions globally.

Dry Type Transformer Market Challenges

Space Limitations and Installation Challenges

One notable challenge for the dry type transformer market is the constraint posed by space limitations and installation challenges. Dry type transformers typically have larger dimensions compared to oil-filled transformers of similar power ratings. This larger footprint can be a significant drawback in urban or industrial areas where space is limited and expensive. According to the American National Standards Institute (ANSI), the bulkier design of dry type transformers can hinder their adoption in locations with restricted installation space. Overcoming this challenge requires innovative designs and compact solutions to enhance the versatility of dry type transformers, making them more adaptable to diverse environments. Additionally, addressing installation complexities, such as the need for reinforced foundations and specialized mounting arrangements due to their size, is crucial for expanding the market reach of dry type transformers.

Limited Fire Endurance and Overloading Capacity

A significant challenge in the dry type transformer market is the limited fire endurance and overloading capacity of dry type transformers compared to oil-filled counterparts. Dry type transformers are more susceptible to thermal stress and overloading conditions, which can compromise their insulation and overall performance. According to standards set by organizations like the Institute of Electrical and Electronics Engineers (IEEE), dry type transformers generally have lower overload capacities and reduced ability to withstand short-term overloads compared to oil-filled transformers. This limitation can pose challenges in applications where occasional overloading is a possibility, affecting the reliability and longevity of dry type transformers. Overcoming these challenges requires advancements in insulation materials and cooling technologies to enhance the thermal performance and overload capabilities of dry type transformers, ensuring their suitability for a broader range of applications and operating conditions.

Regional Trends

North America: In North America, there has been a growing trend towards modernizing and upgrading power infrastructure, driven by factors such as the need for grid resilience and the integration of renewable energy. The U.S. Department of Energy (DOE) emphasizes the importance of enhancing grid reliability, and this trend aligns with the adoption of advanced dry type transformers in the region.

Europe: Europe has been at the forefront of promoting environmental sustainability and energy efficiency. The European Union (EU) has set ambitious targets for reducing greenhouse gas emissions and increasing the share of renewable energy. This has led to a trend of adopting dry type transformers, known for their eco-friendly attributes, in various applications across the European power infrastructure.

Asia Pacific: The Asia Pacific region has seen rapid industrialization and urbanization, driving the demand for reliable and efficient electrical systems. Additionally, the increasing deployment of renewable energy projects in countries like China and India has contributed to the adoption of dry type transformers. The growth of smart cities and infrastructure projects also influences the demand for modern and environmentally friendly electrical solutions.

Middle East and Africa: In the Middle East and Africa, the energy transition towards more sustainable and resilient power systems is influencing the adoption of advanced transformers. The focus on renewable energy projects and the need for reliable electrical infrastructure in expanding urban areas contribute to the demand for dry type transformers in the region.

Latin America: Latin America has experienced growth in its industrial and commercial sectors, leading to increased demand for electrical equipment. The region’s emphasis on improving energy efficiency aligns with the adoption of dry type transformers. Additionally, efforts to address environmental concerns and comply with international standards contribute to the market trends in Latin America.

Key Players

Key players operating in the global dry type transformer market are Eaton, Schneider Electric, Siemens Energy, Toshiba Corporation, Hitachi, Ltd., General Electric, Fuji Electric Co., Ltd., CG Power & Industrial Solutions Ltd., Kirloskar Electric Company, Hyosung Heavy Industries, Hammond Power Solutions, Voltamp, WEG, TMC Transformers S.P.A., Hanley Energy, Alfanar Group, Tbea Co., Ltd., and Efacec.

PRICE

ASK FOR FREE SAMPLE REPORT